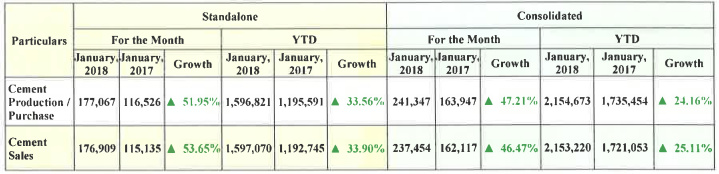

December Despatches - Strong results continue

3 Likes

NOTES FROM EDELWEISS CONFERENCE - 01-FEB-18

The beneficiary of demand recovery in Andhra Pradesh: According to Sagar Cements (SCL), cement demand in Andhra Pradesh/ Telangana (a key market with 55% sales exposure) has been growing at over 15% YTD in FY18 and is expected to continue growing at similar pace at least for the next two years.

Irrigation and housing are driving demand growth. 9mFY18 volumes for SCL grew a robust ~23% YoY (aided by demand recovery in AP and benefits of acquisitions) and the company remains confident of similar growth for FY18. At all-India level, SCL expects demand to clock 6.5-7.5% CAGR over the next five years.

Capacity expansion provides further volumes growth visibility

SCL is expanding its cement capacity at V izag from 0.3mtpa to 1.5mtpa (by September 2018) aiding visibility of a strong volume growth over FY19 and FY20 as well. The company estimates huge demand potential in Vizag where it plans to produce only slag cement. The unit will also aid savings in logistic cost with reduction in lead distance. While Vizag expansion will take its capacity to 5.5mtpa, SCL also has planned to add another 0.5mtpa at its plant in Gudipadu, which will take its capacity to 6mtpa by FY20.

Captive power capacities to yield significant savings

SCL has recently commissioned 6MW of waste heat-based power plant in Matampally, which the company plans to increase to ~8.5MW by Q1FY19. It is also installing an 18MW thermal CPP by March 2019. Collectively, both the power plants will help save the company INR400mn p.a. (~40% of FY17 reported EBITDA).

Debt level to remain same despite capex

Despite incurring total capex of INR3.5bn towards various projects, SCL expects debt to stay flat at current level of ~INR5bn.

Prices may remain firm, but difficult to comment

SCL expects cement prices to remain firm in the near term due to the busy season. However, given capacity additions by some players in an already low utilisation market of South, the company does not want to comment over the outlook from a medium to long term perspective.

4 Likes

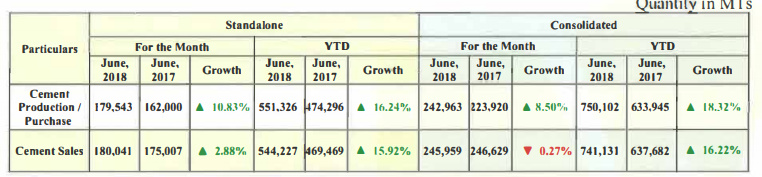

February Despatches

3 Likes

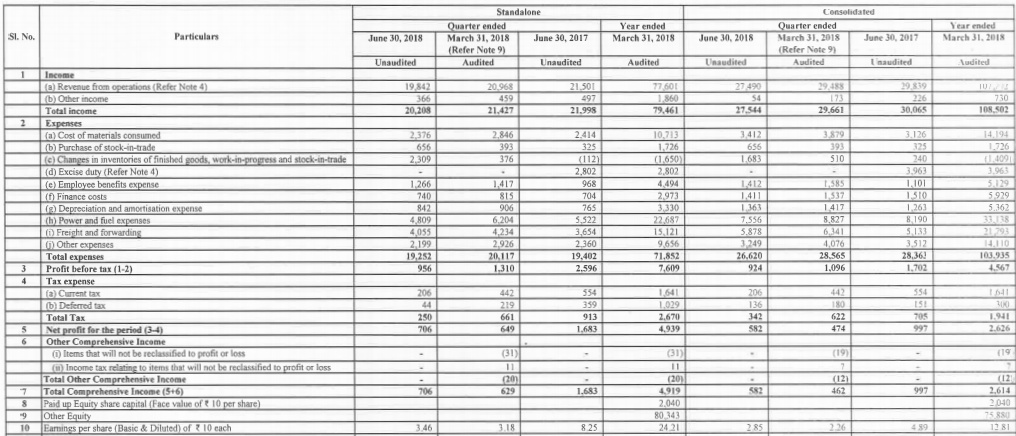

Q1 results: Significantly poor results.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/710df7ad-cd0a-40e4-b1b1-11e315579dc4.pdf

Investor presentation - https://www.bseindia.com/xml-data/corpfiling/AttachLive/275165b1-315a-4933-960a-3d4a59f82bff.pdf

Q1 FY 19 Concall details:

Demand in South especially in Andhra Pradesh and Telangana remain strong. Realizations as well improved marginally on a sequential basis on a back of steady demand. Moving onto the West, pickup in infrastructure projects and lower base have been improving the demand in the region. Prices as well moved in sync with the demand improving on a sequential basis.

Commissioned the expanded capacity of our grinding unit located at Bayyavaram, Vizag, ahead of schedule

Work on the captive power plant is progressing smoothly and we expect to commission it by March 2019

Operating margins for the quarter stood at 13.5%, margin compression was largely owing to higher input prices, slightly lower realization, and at the same time shutdown of the wastage recovery plant for upgrading purposes.

Average fuel cost remained inched up a bit higher as it stood at Rs. 878 per ton for the quarter as against Rs. 923 per ton of clinker during Q1 FY ’18 and stabilization of Gudipadu plant resulted in lower fuel cost on a consolidated basis. Freight cost for the quarter on a consolidated basis stood at Rs. 793 per ton as against Rs. 805 per ton during Q1 FY ‘18.

Mattampally plant operated at 65% while SCLR operated at 80% during the quarter.

The gross debt as on June 30, 2018, on a standalone basis stood at Rs. 312 crore out of which Rs. 174 crore is the long-term and the remaining constituted the working capital. While on a consolidated basis, debt stood at Rs. 550 crore of which Rs. 370 crore is a long-term debt.

There is strong demand in AP. Demand from Tamil nadu and Kerala also picked up. Pricing was weak as supply was moreas demand expectation was high. Price will not improve before mid-Q3.

Transport cost is likely to reduce due to the new axle load regulation

2 Likes

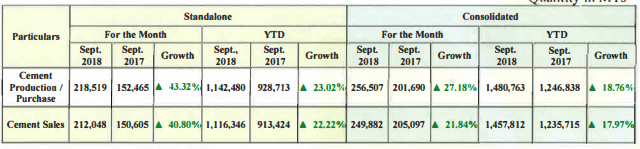

Sep 2018 Despatches:

Dec 2018 despatches

1 Like

NCL industries balance sheet looks good with reduction in debt, I got some cement building blocks from them for construction of my hotel, the quality was good & price was cheaper than aercon blocks from HIL. What is your view?

Is there any red flag on promoters? Why Credit agency saying “CARE had, vide its press release dated February 07, 2018, placed the rating(s) of Sagar Cements Limited. (SCL) under the ‘issuer non-cooperating’ category as SCL had failed to provide information for monitoring of the rating. SCL continues to be non-cooperative despite repeated requests for submission of information through e-mails, phone calls and emails dated from August 3, 2018 to December 5, 2018”.

I think in commodity business promoters must be “High Quality” otherwise in up profit cycle they will siphon profit out and in down cycle they will take more debt !!"

http://www.careratings.com/upload/CompanyFiles/PR/Sagar%20Cements%20Limited-12-19-2018.pdf

They have moved from CARE to India Ratings. https://www.indiaratings.co.in/Issuers?issuerID=5918&issuerName=Sagar-Cements-Limited

O ce a company moves away from a rating agency, they suspend the rating. Standard practice.

@basumallick even they moved from Care to India Rating, why Company does not give clear reply / information about discontinue to their service ! I see this is not honest practice by promoters/company management

Who has not given a clear reply??

company to Care. If company clearly reply to CARE that they don’t want their services and switched to other rating agency, CARE will never care of that company!!

why ROE and ROCE is very low ?

That is not how it works. Once a company switches to another rating provider they not only inform the previous agency, but the company also needs to report if there is any change if rating between the old and the new agency.

The previous rating agency will always say that they were refused access till the duration of the rated instrument in such a case as per SEBI mandate.

Some details are here:

1 Like

Excerpts from CLSA view on cement sector (8-Jan-19):

Government focus drove demand in FY19; we expect momentum to continue

- Over the past several years, a weak macro weighed on cement demand which reported growth of sub-5% over FY11-18 (FY18 growth of 8.5% is off a very low base).

- FY19 saw a trend reversal as demand is expected to be 9%-10%, the fastest growth in almost a decade.

- Industry feedback indicates FY19 growth has primarily come from government-led infrastructure & a boost from pre-election spending (states as well as centre).

- Across regions, the south and east have witnessed strong growth while the west faces challenges.

Utilisation rates to move up

- Supply additions continued and rose c.5% YoY but trailed incremental demand in FY19 which drove up industry utilisation by around c.3ppt YoY to 69% in FY19.

- Despite relatively lower utilisation than average, several players continue to add capacity; we forecast a 4.5% Cagr for capacity over FY18-21CL.

- However, with demand growth ahead of supply, industry utilisation rates should see an up-trend, which we forecast to average 73% by FY21.

- There would however be regional disparity with the south witnessing the lowest absolute utilisation while the north & central should see the strongest absolute level.

Energy cost advantage but cement pricing holds the key

- Energy prices exerted severe pressure during most of 2018 but have started to ease. For example, petcoke prices are down 25%+ & diesel prices are down 20%+ from peak.

- The benefit of these along with higher axle load should be visible during 2019.

- The concern, however, is on cement pricing which remained weak for most of 2018. For FY19 we estimate a 1% rise on a blended basis, well below cost inflation.

- This is because of a market share fight among the large & the mid-sized players, which resulted in a c.12% YoY decline in the FY19 unit Ebitda despite a better utilisation rate.

- With UltraTech likely to ramp-up its acquired capacity, Shree’s foray into the south and west, Ramco’s expansion in the east and Dalmia’s foray into the west, concern remains.

2 Likes

sagar has been showing quite consistent sales cagr…, higher than peers would say…, have they been adding capacity lately? margins and cash cost still some room to improve…, at 13xev/ebitda, 30%+cagr, looks an interesting story…