Volumes for quarter remains steady. Demand in Maharashtra remained strong. Volumes in south remain soft .

Expect good demand to be seen in future due to affordable housing and various govt policies.

Yearly expectation of regional growth :

Ap and Telangana - 15% due to small base and most demand drivers active from govt standpoint. Lots of spend is on concrete roads at the Panchayat levels.

Karnataka - 5 %

Maharashtra and Orissa - 10 %

Tamil Nadu and Kerala - (-5%) - don’t cover full Tamil Nadu, cover which is in north and till now not seeing any improvement.

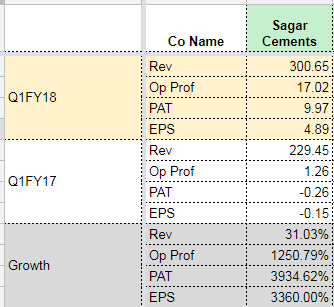

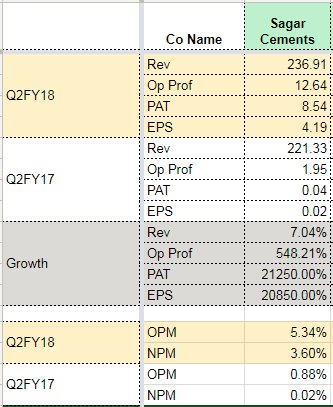

Sales grew by 31% due to improved volumes and realization.

EBITDA grew by 65%

Op margins 14% against 11% increase due to cost control measures.

Gross debt at consolidated level at 773 crores .

Freight cost reduced due to increase in FOR (free on rail - freight cost borne by customer) sales (about 90% this time ). But this sales is on choice of customer and not sustainable

BMM - Doing brownfield expansion there, so cost is high (due to frequent shut down of plant ) but from Q4 it will reduce and plant will be aligned.

If coal prices remain same , we expect reduction in cost of production .

Generally q2 and q3 are not good quarters as per price realisation, so there is some reduction in price in first month.

Co has seen 7.5 to 10 Rs decline in realizations across our markets in this July month which is seasonal. For consumer it can be somewhat more due to post GST and monsoon season .

Capex plan:

Capex is 275 crores total for this year and next year (incl growth capex and maintenance capex).

WHR has become operational last month and it is ramping up and will result 2-3 crores saving in this quarter, and 4-5 crores in Q3 or 100-125 per tonne cost saving .

Grinding station will take a year to be operational

Will commission recently 1MW solar plant .

Cost reduction strategies

For Matapally plant , co is using 95% pet coke

Also heating capacity will help to reduce cost

In BMM, co will start using pet coke from Q3 due to change in burner which is to be done. BMM will have savings of around 60-65 per tonne

Debt repayment will not be much in current financial year , 40 crores would be repayment on consol basis

Supply addition in next 24 months - Around 6-7 MTPA

NCL to commission in Q3 (1 mtpa ), KCP will come and Shree cement will also start in q3 or q4. This will spread over wider canvas and will cover wider geography and will have 2.5 MTPA around in South alone .

Increase in price of imported pet coke & coal has resulted in increase in the average fuel cost per tonne of clinker produced. Average Fuel Cost Per Tonne = 926 rs/Tonne (up from 866 yoy)

Freight cost per ton increased due to increase in fuel prices. Freight Cost per Tonne = 840 rs/tonne (up from 753 yoy)

It was my interaction with certain contractors to outsource construction of colleague’s home at Hyderabad. We realized that most of them proposed sagar cement for construction.

The overall demand across key markets remained relatively mixed, as the impact of sand mining and political instability in TN were partially offset by strong demand in AP / Telangana.

Marginal softening of prices across our primary markets and higher input costs resulted in lower operational profitability.

The Company has commissioned 6 MW Waste Heat Recovery Power Plant at Mattampally, Nalgonda district, Telangana, and 1 MW Solar Power. This will ensure greater control over power and fuel costs. The company expects to reduce its operating costs further once its new grinding unit and captive power plant is commissioned.

Project Highlights (1) The Company has ordered core equipments for grinding facility project at Bayyavaram., Anakapally, Visakhapatnam, Andhra Pradesh which is expected to commission by September 2018. (2) The Company has ordered core equipments for 18 MW Captive Power Plant at Mattampally, Suryapet, Telangana, which is expected to commission by December 2018.

The company expects to reduce its operating costs further once its new grinding unit and captive power plant is commissioned.

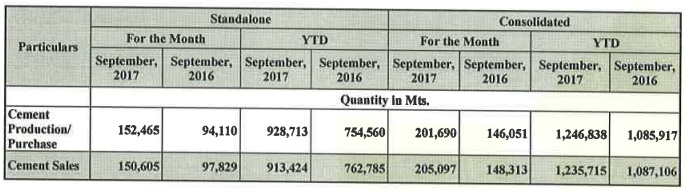

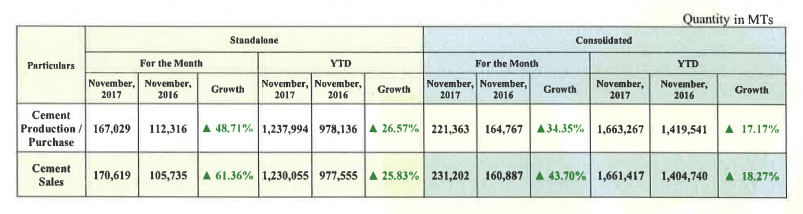

During Q2FY18, the plant operated at reasonable utilization levels producing 5,81,027 tonnes of clinker and 5,86,243 tonnes of cement. The Mattampally cement Plant and BMM - Gudipadu Plant utilization level stood at 52% and 63%, respectively in Q2FY18.

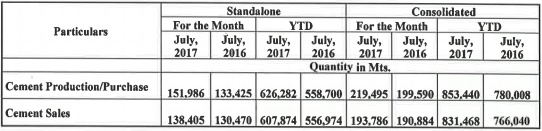

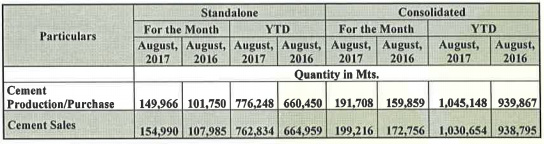

The company consolidated cement sales volume stood at 5,98,063 tonne for Q2FY18. The company has dispatched 5,61,140 tonne of cement by road transport and 13,262 tonne from rake as compared 4,89,731 tonne by road and 21,830 tonne by rake in corresponding previous quarter.

The consolidated gross debt as on 30th September 2017 stood at Rs. 496.22 crore out of which Rs. 372.12 crore is long term debt with the remaining Rs 124.10 crore constituting working capital. Cash & Bank Balances held by the Company at the Balance Sheet date was Rs. 100.86 crore. The Net Worth of the Company as on 30th September 2017 was Rs. 777.76 crore.

The company average fuel cost increased 9% to Rs 926 per tonne in Q2FY18 from Rs 866, (down 3% to Rs 842 per tonne for Sagar Cement while up 36% to Rs 1179 per tonne for BMM). Increase in price of imported pet coke and coal has resulted in increase in average fuel cost per tonne of clinker produced. Domestic: International coal mix was 04:96. The company average coal cost stood at Rs 4896 per tonne for Indian coal and Rs 7508 per tonne for imported coal, as compared Rs 4618 per tonne for Indian coal and Rs 6060 per tonne for imported coal in the corresponding quarter in previous year.

The company average freight cost rose 12% Rs 840 per tonne in Q2FY18 (up 11% to Rs 814 per tonne for Sagar Cement and up 17% to Rs 917 per tonne for BMM), due to hike in freight rate and fuel prices.

The company employee costs stood at Rs. 12.60 crore on consolidated basis in Q2FY18 as compared to Rs. 11.40 crore during Q2FY17 on account of annual increments released in second quarter. The company Raw Material cost was up to Rs 34.37 crore from Rs 26.27 crore corresponding last quarter due to higher production during the current quarter.

The Company expects cement demand outlook remains positive on the back of sustained government spending, slowing capacity addition and expected moderation in input costs.

The Company expects demand for cement in its key regions like Andhra Pradesh and Telangana is likely to grow 12%-15% in FY18. Moreover, other markets like Maharashtra and Karnataka are also likely to grow 5%-10%, and in Tamil Nadu the company expects demand to decline 5% because of sand mining problem and political instability, but these problems are expected to be resolved soon and thus overall demand outlook is stable.

Started tracking the stock recently and impressed with what I have seen so far. Would be interested to understand the negatives in detail though

What I like

Impressive EPS Growth expected in future

Return Ratios should improve going forward both ROCE and ROEs should improve

Reduced Debt considerably over the last 5 years . Debt to Equity has come down to 0.58 from 1.85

Net Margins started improving as well

EBIDTA Margins steady over last 5 quarters

Zero pledge and also good Promoter Holding

Tax Paying

Revenue Growth and Asset Growth consistent over last 5 years . Very impressive Asset growth over last 5 years

Ability to generate good cashflow

DSO and DSI both are consistent overy last 5 years and impressive ability to collect cash reflected from DSO and Cashflow

Valuation Ratios are on higher side but with Expansion and Improvement in Utilization they should come down considerably :

EV / EBIDTA , EV / Sales , EV / Tonne are slightly on slightly on higher side but if we consider growth then shows a different picture

Strategic location being in the right state will help for sure