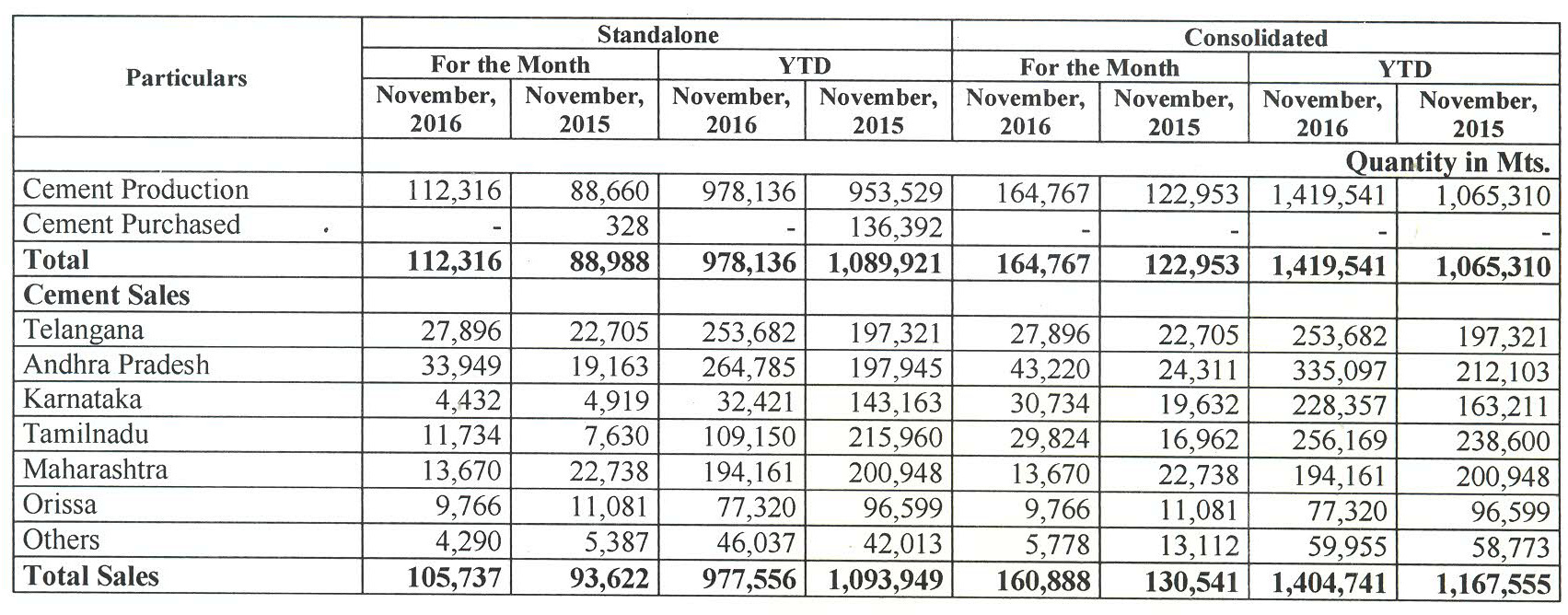

Good numbers in their November despatches:

Hey can u tell that even if sagar has declared QIP at 800 , why the price is not catching up ??

And if it will not then why Institutional and HNI are paying so much when they can buy from market at much discount ??

Please explain what I am missing …

@DEEPAK_AGARWAL The volume traded for stocks like these are very poor for large investors to buy in bulk. The average volume is about 10-11 thousand shares, which will not help their cause. That is why the QIP is done.

1 Like

But then if QIP is coming at 800 , so wouldn’t this news generally take price near to 800 ?

Normally if QIP price is this much above current price , so it’s shows stock is at undervaluation despite good fundamentals or QIP price doesn’t have any relation to current price . Please clarify if possible …

If I am not mistaken, the QIP is being subscribed to only by promoter and Belgian investor which already holds 18%. Please correct me if my understanding is wrong.

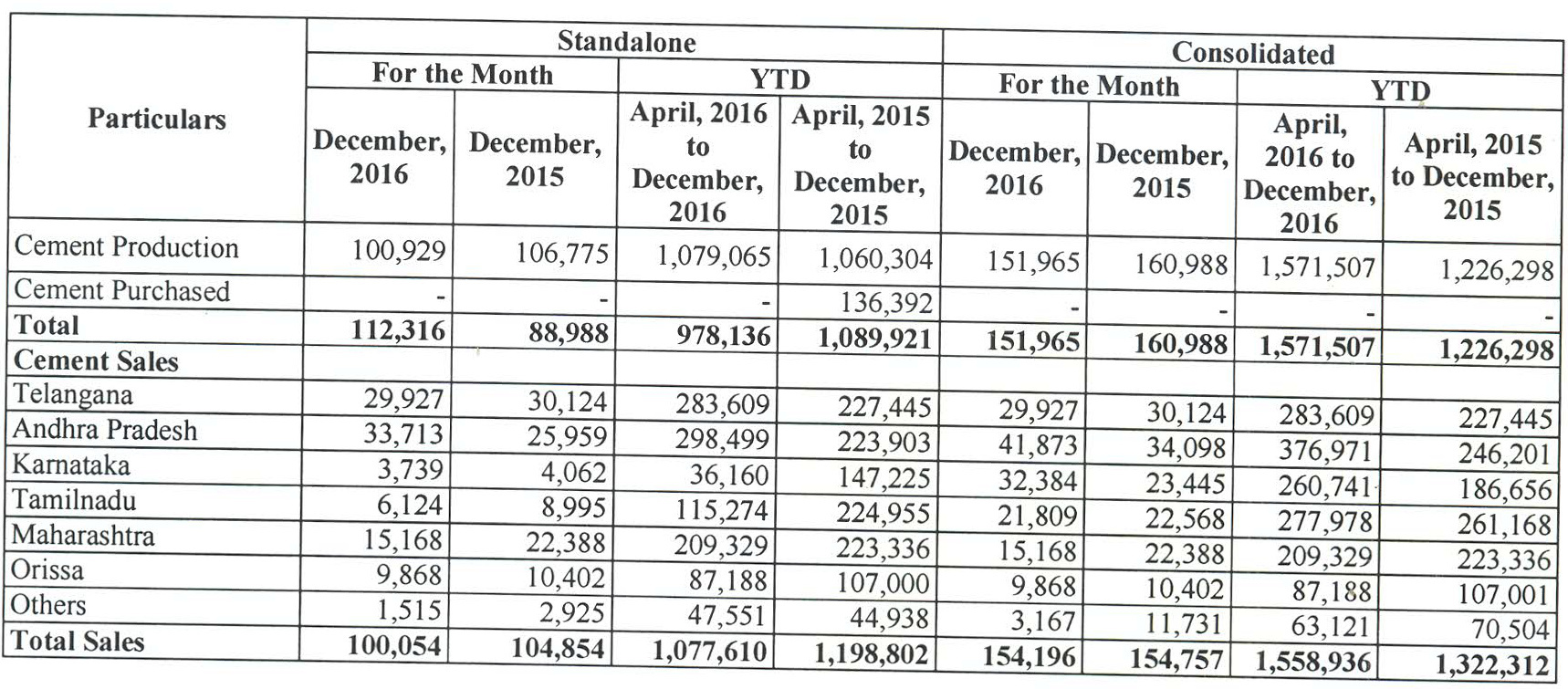

Q3FY17 Concall Details

• The actual situation was not as bad as envisaged at least in the markets wherein we primarily operate.

• Volumes and prices both remained relatively stable in the southern markets as the region.

• Prices remain steady on the back of institutional demand in the regions that SCL operates.

• Price contracted in the Gujarat while Maharashtra witnessed price improvement during the quarter.

• The overall impact was mainly in terms of receivables and the working capital cycle, which got stretched.

• Co is seeing the environment normalizing and long-term outlook remains positive on the back of government thrust on developing infrastructure and affordable housing schemes.

• SCL completed the allotment of approximately around 6 lakh preferential shares to promoter and a non-promoter group at an issue price of Rs. 800 per share.

• SCL has completed the acquisition of a grinding unit located at Bayyavram near Vizag. The acquisition should help lower logistics costs as well as enable SCL to reintroduce the slag cement in parts of AP and Orissa.

• The average fuel cost for Sagar during the quarter was at Rs. 819 per ton as against Rs. 757 per ton higher on account of greater usage of imported coal. Average fuel cost for BMM during the same quarter was slightly higher compared to the previous quarter.

• Freight cost for Sagar stood at Rs. 775 per ton as against Rs. 596 during Q3 FY16, higher primary on account of increasing diesel cost and also incremental freight rates. Freight costs for BMM stood at Rs. 929 as against Rs. 725 for the same quarter during last year.

• Sagar’s Mattampally plant operated at 43% utilization level while BMM operated at 64% during the quarter. Consolidated utilization of 55%. SCl does not expect utilization to go beyond 60% in the next 12-18 months.

• On a consolidated basis, gross debt stood at Rs. 483 crore out of which Rs. 395 crore is a long term. Debt equity ratio stands at 0.66:1, cash and bank balances were Rs. 7 crore

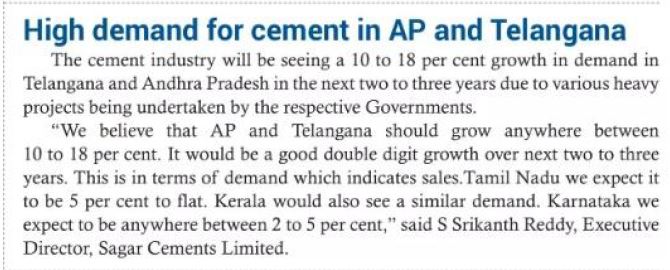

• Growth forecast for next year:

○ AP + Telangana - 15%-20%

○ Kerala, TN - Flat

○ Karnataka - 5%

○ Maharashtra - 5%-10%

• On Amravati

○ On the ground, only the road works has just started. The other building projects are expected to start somewhere around 2nd half of FY18

○ Stalled irrigation and low cost housing is expected to pick up earlier

• In AP & Telengana, tender orders are being distributed based on market share (share of sales tax submitted). It’s about 2-3% of current sales.

• Incremental capex is expected to be 135-140 cr for the next two years

4 Likes

Dear Abhishek,

Can you please suggest a cement company which has high OPM and reasonably good balance sheet. The mid cap cement co DECCAN, NCL ind stand anywhere close to SAGAR with regard to outlook?

How about the large one like SHREE or INDIA cements?

Really appreciate your efforts for SAGAR cem.

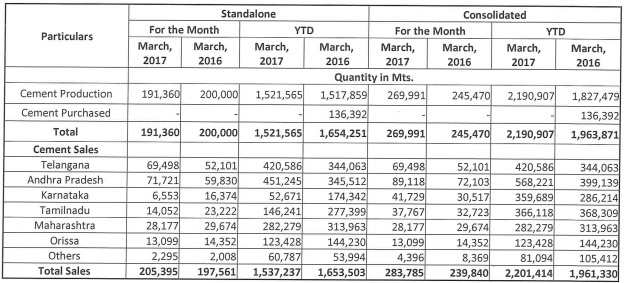

March 2017 despatches - good numbers

3 Likes

Sagar Cement has got the “best Management Award” from the govt of Telengana for a second year in a row.

1 Like

Abhishek Da, do you think at present price, Sagar cement is offering adequate margin of safety… Thanks

Depends on the investment horizon. My sense if that the cement cycle has just begun and it is likely to do reasonably well over the next 2-3 years. Also, the core demand from Telangana & AP is expected to be strong for the next 5 years at least. Cement prices, and price control by government, may act as a dampener, in the short term.

1 Like

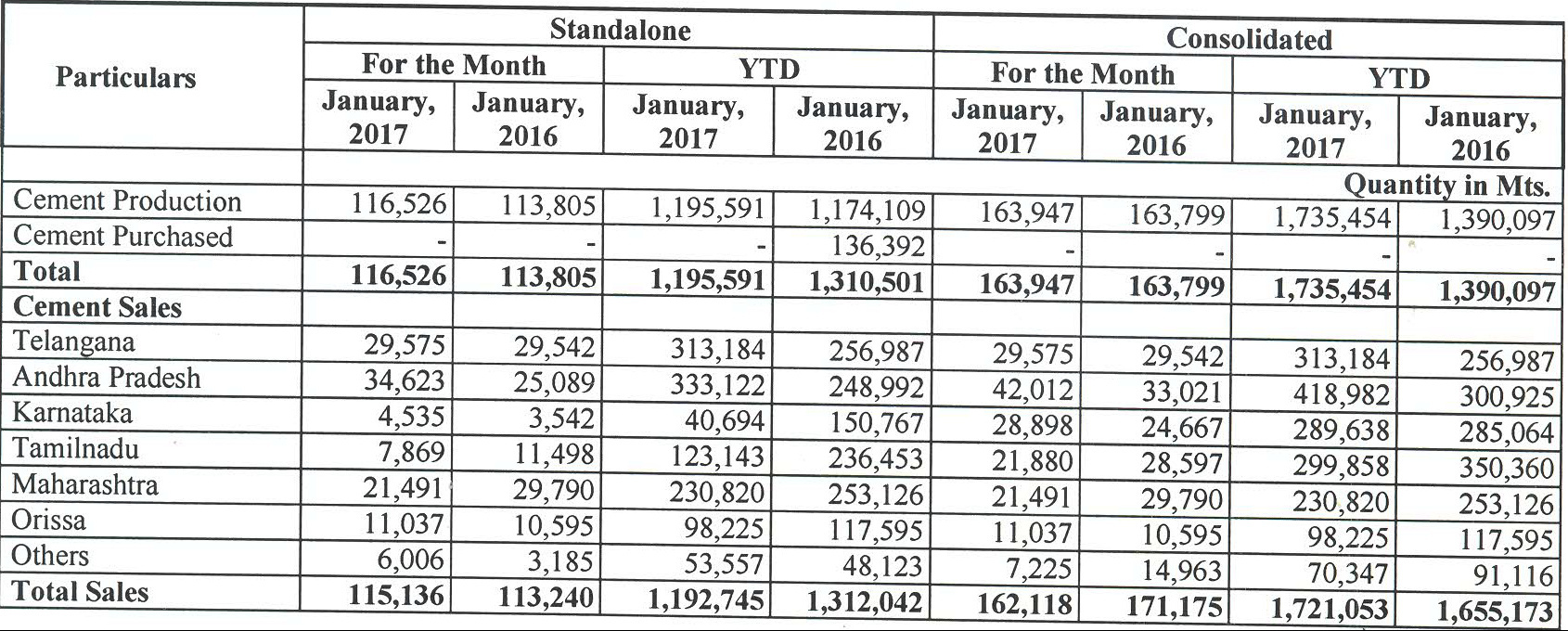

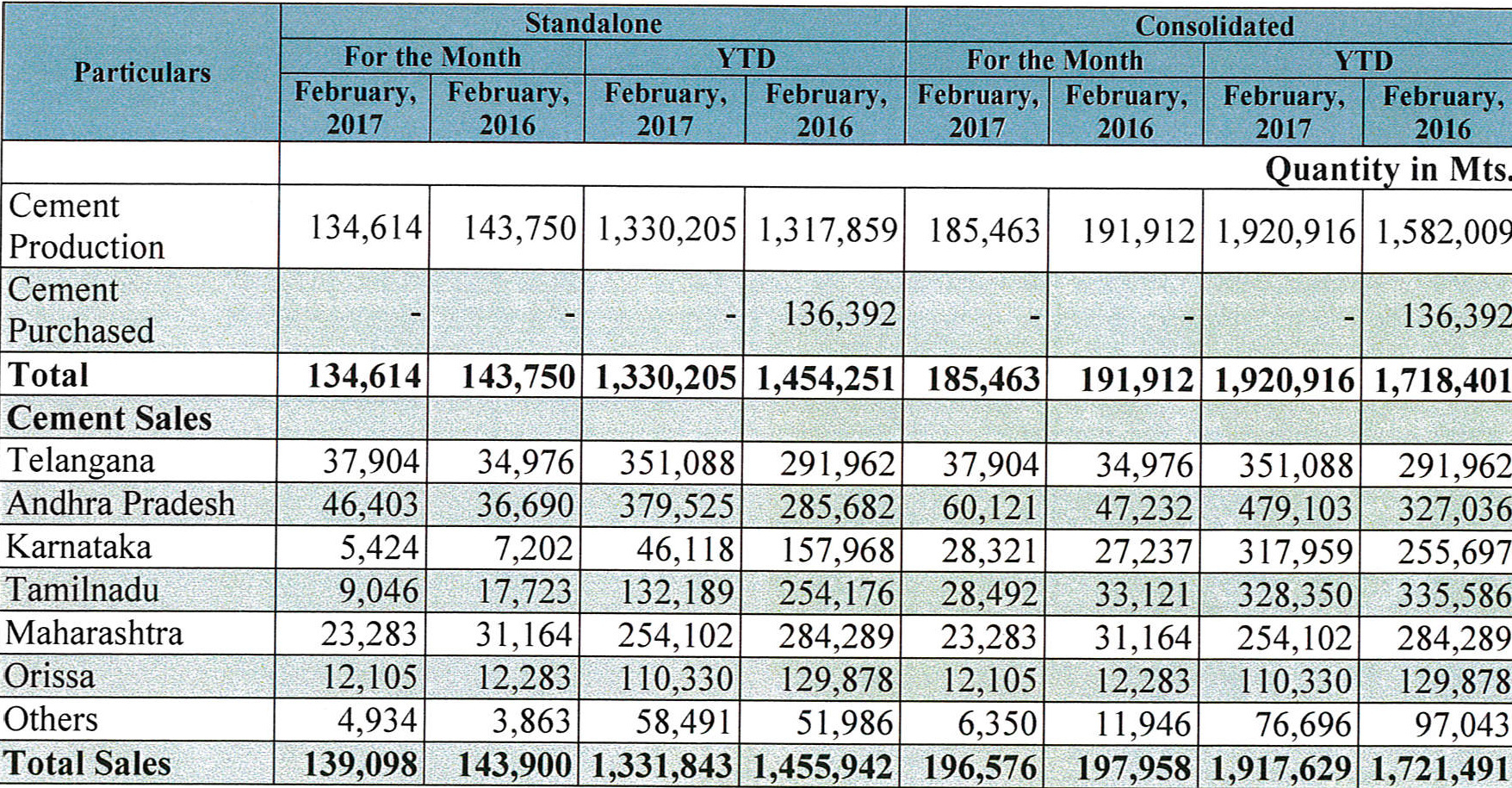

April 2017 despatches

Weak despatches in April…

Hi @basumallick, whats your analysis after the Q4 results and the commentary by the management?

Thanks.

Average and expected results… awaiting the concall for better understanding.

May 2017 despatches

1 Like

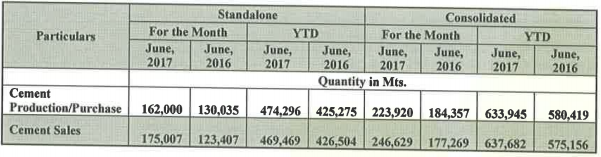

June despatches - significant growth in both production and sales

1 Like

5 Likes