I personally feel the cards and ATM utilisation will reduce and all banking functions will transfer to smart phone. Ultimately AADHAR + MOBILE no may become your identity and CIBIL also will depend on this. I feel that over a period of time all our free cash flows will be monitored and accordingly loans will be advanced. I think we will have a different days ahead.

Deepak, any idea on WHATSAPP entering the payment solutions and aadhar enabled smart phones?

will generation of black money decrease and tax compliance increase-what’s ur opinion?

I also think telecom providers will have some good days ahead. A good service provider will win the race.

Prasad.

On ATMs

If we notice many banks have already been charging us for ATM transactions. We get a freebie of 5 withdrawals and then you are charged. If you use your HDFC ATM card on ICICI ATM then HDFC has to pay a lot on that transaction (its called reverse interchange, I think its around 17-20 rupees per transaction). So like my dart diagram banks don’t want you to transact on ATMs actually. In fact nobody wants physical cash. My wife is a banker and she was taking care of cash reporting to RBI during demonetization in NCR for a bank. I could see the nightmare she was going through!

On Aadhaar

I also think this is the future. In 2013 September UIDAI and RBI asked pre paid wallets to do a pilot on Aadhaar based domestic remittance (for financial inclusion pertaining more to payments bank today). At that point of time the response was lukewarm. But since then I have seen Aadhaar being forced upon us and maybe its a blessing in disguise. RBI doesn’t allow Mobile + Aadhaar OTP as an ekyc authentication. If this was allowed I believe it would greatly improve financial inclusion. Aadhaar + OTP allows only linking of Aadhaar or verifying of Aadhaar. To ekyc you have to give biometric details.

Yes in the future our credit scores will all be linked. It’s a matter of time now.

On whatsapp

Facebook already has P2P payments on their messenger on their US app. FB also has payment widgets in Malaysia. Google also has send money on email. Whatsapp is also working on P2P transfers in India. They are riding on UPI that’s what the rumour is. In my opinion chat apps getting p2p is better than payments app building chat. Case in point is whatsapp/fb messenger/hike app building p2p vs a paytm/freecharge building chat.

On telecom

I am not very bullish from a digital payment point of view on telecoms. I feel they are best suited for payments bank though.

Nice Coverage @deevee Couple of questions from my side if you can throw some light on the same. It will help me and forum members

RBL and few other banks provide API access to Fintech companies. How this model works and how is the profit sharing works. I think they will be able to run the analytic tools as well to sell more services to clients (RBL conducted a Hackathon on the same recently I suppose to utilize its infrastructure to innovate and come up with new products)

RBL and few other banks provide services under Financial Inclusion which comes under priority lending as per the govt norms which many of the banks do not consider as a core revenue source and they consider the revenues from third party MFIs to match the govt criteria. Can RBL use its platform to cross sale its services to the client which are joined using Financial Inclusion?

Since we are all talking about Banking and financial institutions in generals, it is worth noticing Warren Buffet’s view on the Financial institution in General.

Mr Buffet was holding Freddie Mac and Fannie Mae stock(US Mortgage companies), and he sold them in 2000, well before financial crisis happened. In 2010 US FCIC conducted two hours session with Mr Buffets probing his thought process and view about the cause of the 2008 financial crisis.

When the interviewer asked him why he sold Freddie Mac and Fannie Mae- Buffet responded- "They were trying to -– and proclaiming that they could increase earnings per share in some low double-digit range or something of the sort. And any time a large financial institution starts promising regular earnings increases, you’re going to have trouble, you know*. 2010-05-26 FCIC interview of Warren Buffett_1.doc (195 KB)

When you have management which is foxing on achieving growth in Finacial service- be wary- be very very wary. It is very easy for a finance company to grows because there are always borrowers ready to take a loan. So, demand for the debt will always be there. During a good time, it is hard it finds good borrowers, so the companies comprise their lending criteria and grant loan to less creditworthy borrowers. This last for a while, but sooner or later reality catches and the company faces bad debt. It has happened time and again.

The valuation of the finance company (Bank in particular) relies on gross NPA/Net NPA. The company which has pristine NPA, enjoy high premium while rest of the banks have considerable less valuation.

RBL bank in the current form is quite new and it’s books is not seasoned yet. I think time will tell if it can retain the premium valuation, but it depends upon its ability to give quality credit and maintain good growth rates. IN the current environment it is not difficult to maintain growth rate, and you know the quality of loan only in hindsight. Looks at the major PSU banks, the NPA they are reporting is 7-10 years old. So it will be a while before one knows the quality of credit disbursed by RBL.

In my view, the stock is running ahead of time. HDFC Bank, Kotak Banks have a history of 20+ years behind them, which RBL bank in the current form does not have. However, it has ingredients to be a good stock.

"…And any time a large financial institution starts promising regular earnings increases, you’re going to have trouble, you know*

Good point. At the same time. RBL is not a large financial institution. Management has been repeatedly saying they are able to grow faster because of low base.Further, we need to keep a the NPA levels as suggested rightly. And above all there are newer opportunities emerging as pointed in lot of detail by Deepak which is RBL is capturing , and infact at top 2 of capturing those.

On the books you mentioned, kindly share the Amazon/Flipkart links…

This is because there are different books, editions, similar titles… and dont want to end up purchasing the wrong books, as they are expensive too.

On API Banking

Banks such as YBL, RBL, Kotak etc. are packaging their banking facilities to the external corporate clients as ‘API Banking’. It is nothing but an integration between their systems and the clients systems. Rather than giving manual requests it is systems of the client and bank speaking to each other. If you understand API I am sure you would clearly understand what this is. If you don’t know what APIs are then read this. Also have a look at these two videos - YBL API Banking, RBL API Banking. On the income side it is again back to what I said earlier its mainly float income from liability deposit of the client partner and fee income from transactions.

Honestly I did not understand the second point. Please could you help.

Since there is a nice but light debate on RBL from an investment point of view. I liked what Vishal Bharati mentioned about low base. In 2010 May if I recall correctly RBI shifted calculation of Savings Deposit interest rate to a daily calculation from least in a quarter and then few months after I think it allowed banks to offer any rates to their customers. YBL was in a very favourable position to immediately raise interest rates on savings deposits but ICICI and HDFC didn’t change anything as far as I remember for obvious reasons. At YBL we raised the rates to 7% and Kotak to 6% (which they advertised heavily). Will not go into the details how base rate is used to derive savings and term deposit rates and the management calls which are made. Like I mentioned before go back to old annual reports of YBL you will be surprised to see the CASA ratio. From ~6% or so then to today at ~37%. The whole focus of the bank was on getting deposits and we spent all our energies there. Simultaneously their loan book kept increasing, again have a look at the old reports.

My personal take is that RBL is charting a very similar trajectory as YBL just that the digital world on retail side is different today (to which they are coping up quite well) and on the asset side of corporate their asset quality ratios are quite good, they are trying to raise money and hopefully this crucial area is executed well.

Well none of us can forecast with utmost accuracy what the future of the corporation will be. But let’s hope for the best and atleast visualize the worst. That’s the key to happiness as per Epicurus

Damodaran on Valuation (2nd ed): Priced at 600 odd. Amazon link

McKinsey on Valuation (6th ed): Priced at 4000 odd. Amazon link

But both valued at priceless.

Do visit Prof Damodaran’s website, blog, youtube and twitter. If you have a good problem or an approach he is always willing to discuss with you. And yes he knows a lot about our Indian companies.

p.s. I got Damodaran’s book as part of my b school but I have read only the 5th edition of McKinsey. The 5th ed. is freely available now I think.

I will try to rephrase my second question. RBL was focussed on Financial Inclusion from 2012-2013 if I am correct as I watched some videos from management. Can RBL cross sale its products to the lower income clients which they have garnered through Financial Inclusion?

I could find one other similar book by mckenzie… 6th edition, universityedition and similarly priced.

Would you know the difference as compared to the book in your link.

Hi Deepak,

The difference between YBL and RBL is fee based income. For first 6-8 years (more or less) YBL 50% of income was fee-based. For a young bank, the fee based income is great, because the bank get’s without using the raw material (e.g money). I have not tracked RBL closely so far, so cannot comments much, but I suspect it may not be higher.

Another thing to consider is return ratios for YBL ROE (20+) and ROA (1.7+). RBL’s return ratios are not great. So as compared to YBL’s looks expensive and overvalued to me.

Perhaps I could not get my point across. I meant that the business trajectory is the same that is they are approaching it in a similar fashion. Do refer the charts I have posted sometime back on this thread.

You are rightly saying on the valuation front it might look costly. But which of the private bank is undervalued I am not able to figure out

Rgds

disclosure: YBL is the largest contributor in my portfolio

Thanks for the rich guidelines and references on Valuations. I also follow Aswath Damodaran and have huge respect on his knowledge and teaching style.

Though i am strong believer of valuation methodology (fundamentals, intrinsic values etc.) sometimes my thoughts are diverting to quality companies growing at faster pace (like Bajaj Finance, Eicher Motors etc.) and proves me Valuation alone will not help always!!! Like you stepped into fairly/slightly over valued “YBL”

Whats your view on quality companies growing at faster-pace and market is comfortable rich valuation for considerable amount of time? (e.g. Eicher Motors, Bajaj Finance, D-Mart, RBL Bank etc.)

Caution: The analysis I am presenting below is work in progress and is at a very preliminary stage. At the end of the post you will know what is the pending work yourself. The flaws/assumptions are also implicit. Also please don’t treat this as sacrosanct for valuation. This is data driven that does not mean you can make an investment decision basis this.

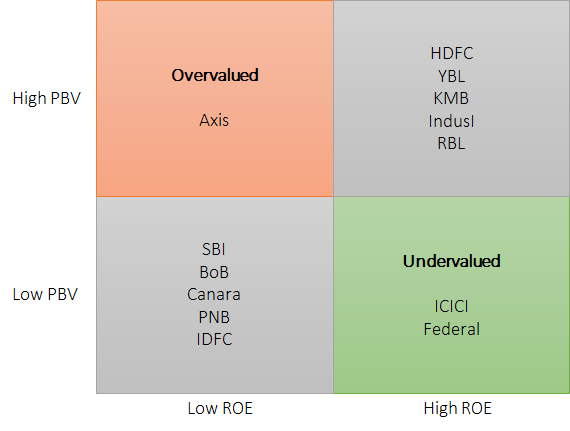

In my earlier post I have explained and given a document which essentially tells that PBV and ROE are the key ratios from a relative valuation standpoint for banks.

Before you go further run through the attached document by Prof Damodaran. In this he essentially does two things:

Takes a set of banks in a given year looks at their PBV, ROE and standard deviation of stock prices. Then classifies a 2 by 2 matrix of Low/High ROE/PBV based on each bank’s comparison with the median of this set. This gives a set of undervalued and overvalued banks in that year.

He does a linear regression of the PBV with ROE and Std Dev to arrive at the expected PBV. The he compares this regressed PBV to the actual PBV to arrive at the conclusion whether the bank is under or overvalued.

So what do we do in our analysis: We also do 2 things.

We take 13 banks (HDFC, ICICI, YBL, KMB, IndusI, SBI, Axis, BoB, Canara, PNB, Federal, IDFC, RBL) which includes all banks from bank nifty. For 2017 we find median PBVs and median ROEs and bucket them into the 2 by 2 matrix shown in the post later.

We take the 13 banks PBV values in 2017 and regress the ROE and Standard Deviation of stock price (as a proxy for risk) and arrive at the regressed or expected PBV value of the bank in 2017. We then compare the actual PBV to the regressed PBV to conclude whether the bank is under or overvalued by what percentage.

Result from 2 by 2 matrix

Result from Industry Regression of PBV with ROE & Std Dev of stock prices

All 13 bank’s data of PBV, Price, ROE, ROCE taken as of 31st March from 2008 to 2017. This data is got from screener.

As a proxy of risk for each financial year the standard deviation in the daily stock prices is annualized to arrive at the annualized number. I have calculated this for each bank for year 2009 and 2017. I will be calculating this for all years from 2008 onwards.

Regression for 2017 is a least square regression. The R square value is decent at ~.70. The Significance F is ok.

I want to do this analysis for all years and see how banks move from one block in the 2 by 2 matrix to the other. Also I want to see the regressed data results year on year. So some work left.

The clear pick for me seem to YBL!

The one to avoid for certain is SBI.

Deepak, one point to accommodate would be that RBL has been on the growth trajectory for only 5-6 years, whereas the others (except YBL) have had many decades to achieve a good ROE. I think RBL is showing a trajectory towards getting to a higher ROE than it is right now, whereas others (excluding YBL again) have had issues on this acount for n number of reasons. YBL of course is a standout.

While I do not generally engage in price discussions, I think it’ll take a lot longer than 1 year for RBL to get to 1000. You’re basically batting for 6-6.5 times PBV. That, my friend, is wishful thinking.

Thank Deepak for the detailed response again. What tool you have used to run the regression? If it is excel, we will wait for your final version of the sheet.

Also it will be good to run similar analysis in NBFC/MFI spaces and post your results here or respective thread… Many thanks.

No specific reason. Just that I wanted to check things empirically before being thorough. It did come in my mind that I should include it though.

One of the pain points is that I have to get daily stock prices from 2008 to 2017 for all of these banks to calculate annualized volatility. I usually dont trust any data other than NSE and screener. NSE allows only 365 days of historical stock prices. So involves a lot of manual effort. I dont have any subscription for data services either.

Tushaar agree with you.

On NBFCs like I said I have not tracked much except a very fleeting analysis of a few housing companies and a couple in consumer lending. So dont have much to share. If you can give a domain set for this analysis with some rationale I can work on it when free.

I also personally feel I get too distracted by books. Yes books. I spend all my free time usually reading and it doesnt give me enough time to work out things. And sometimes these books have nothing to do with the capital markets. Lets see.