This will definitely be the hot topic next week. Few observations

There is an unofficial report that RBL had sold some shares before the ipo at Rs 195/-

The ipo offer price is Rs 225/ which works out to around 23 PE. We can comfortably say that YES BANK has been a top performer in the banking sector, however it has a PE of 19 . So the stock is not available cheap.

However again we all know that ipo is a way for the existing investors to sell out at a premium rate, as they have been invested in the company for 4-5 years.

RBL Banks balance sheet has grown 10 times in last 5 years from 2011 to 2016. For banking industry in general, loans made before 2013 are going bad. RBL’s loan book is not yet seasoned (and so is YES bank’s) so it’s NPA number look good. NPA ratio (NPA as a % of total assets) can be kept low by rapidly growing the denominator (i.e loan book) which is what many PSU banks are trying to do and something that worries RBI and is also the case with RBL. Coupled with this, RBL is offering high interest rates on deposits (there is a branch near where I say, and I see the ads every day) to attract deposits and make it’s CASA ratio look good. RBL has managed all the key ratios well by attracting equity capital, deposits and made huge loans. NIM on these loans will be added to the equity and the party can go on until the loans begin to default.

I think it takes a lot of seasoning for a bank to perfect its lending skills, something that banks like HDFC took years and many other banks (ICICI, Axis) haven’t even done after years of (bad) experience in making loans.

Banks in general has two risks, credit risk and interest rate risk. Banks in India has very little interest rate risk because of access to low cost CASA deposits. Even the worst PSU bank earns a good NIM. It’s the management of credit risk that separates the wheat from the chaff. However, it takes a seasoned loan book to determine if a bank is good at managing credit risk.

A bank that is managed well can last a century and grow to the sky. I think I will wait to see how RBL loan book performs over next few quarters relative to other private sector banks and decide. IPOs in general are dressed to sell and markets (I don’t know how) usually arrives at true value in about a year after listing.

Completely agree. I would also be quite quite wary of someone who’s growing 3 -4 x of nearest competition in absence of any clear brand or technology or market moat. What does RBL brings to table that Yes can’t or Kotak can’t and therefore, why should it grow 3 x ?

I agree that new markets is a factor and would aid growth but anyone growing faster than their ROE tend to run into problem later on. (burnt my fingers on Suzlons and Educomps many many times !)

Big Negative Point : The bank has the lowest CASA Ratio in the industry . This means that it will have to spend more on acquiring funds ( Fixed Deposits and Market Borrowing), which might affect its margin . If a bank has a good CASA , then it reduces the cost of borrowing as it involves current and savings account which have low interest cost.

Big Positive Point : The Gross NPA is 0.98% , which means that less than 1% of the money it has lent out has turned bad.

Few positive points-

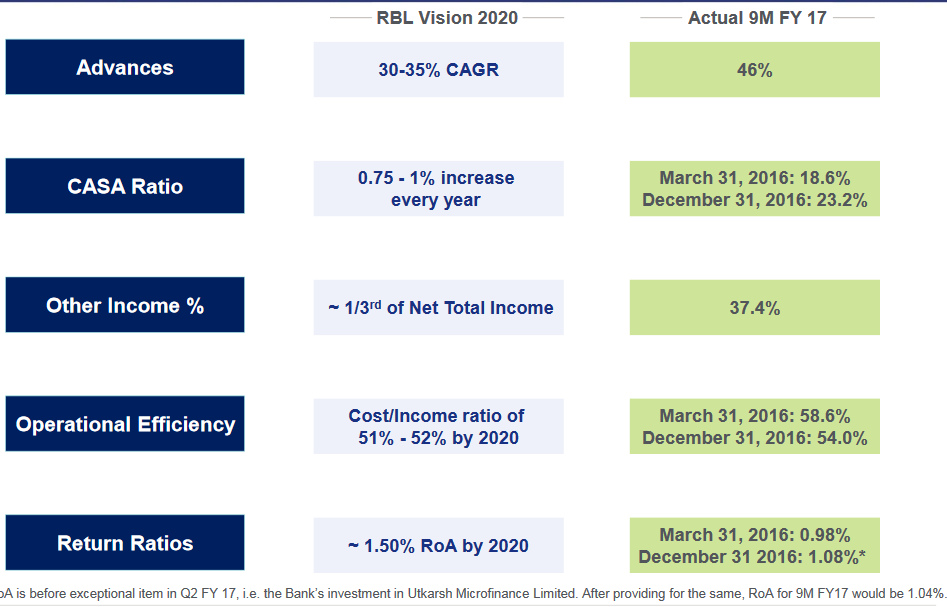

1.CASA ratio is going to improve further

2. Bank is expanding and focusing on the Business Correspondent network instead of expanding the branch network which will help substantially reduce the expenditure on the Branches

3. Able to cross sell Micro Insurance and Term Deposits to the existing and new Bottom of the Pyramid segment

Need to see if it is able to maintain the >35% growth rate mentioned by many analysts.

Disc: I am not expert on Financial segment, researching on RBL bank from last few months. Invested in RBL bank and adding more.

im an amateur so please take my response with a pinch of salt. But i would say that many banks are co existing in the same space and rbl is making its presence in corporate banking . It has huge scope of growth in other areas. Also as we can see there is huge migration happening from psu to private banks. So the size of the pie is growing larger. Also apart from a hdfc/icici retail is fairly dispersed over the others. IndusInd and Kotak are all catering to the non corporate segment such as small and family run businesses.

I feel that as investors we can look at RBL and IDFC bank as potential gains as they are small enough that they can clock high growth if run well for 10-15 years easy.

RBL is a great growth story and I am invested since pre IPO level. I believe the bank will continue to grow 3-40% for the next 3-5 years at least and hence will continue to command premium. The share of public banks will slowly migrate to private banks as it has been over the years.

I think RBL will continue to remain in demand after HDFC. It has the potential to be the future YES bank in some years. Can prove to be a great compounding story for the next few years.

RBL seems to be trying hard to increase their customer base and thereby increasing the CASA, i have witnessed many outlets migrating to RBL instead of any other bank (Mad Over Donuts being one of them)

Also, they are providing 7% of interest on savings account with certain terms and conditions, they also provide a wide range of credit cards and people really get benefited by availing various movie ticket offers and stuff, over-all the efforts are quite visible.

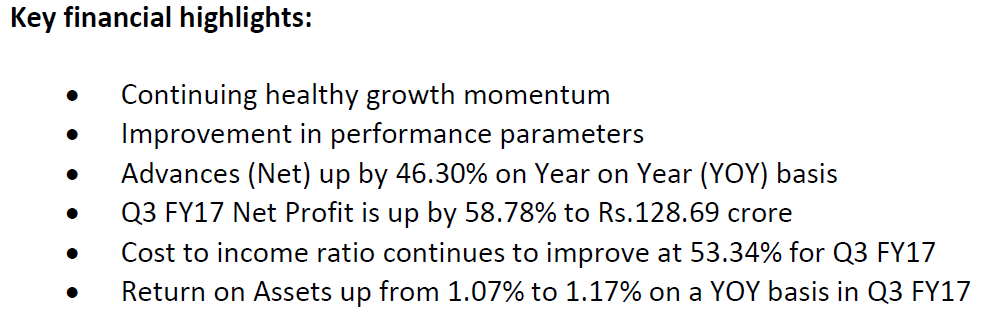

Excellent and consistent Q3 nos. Looks like the next IndusInd Bank in making. This should qualify among those candidates with 30%+ CAGR for min. 3 yrs. Management vision statement 2020 mentions the same, stock is fully priced though.

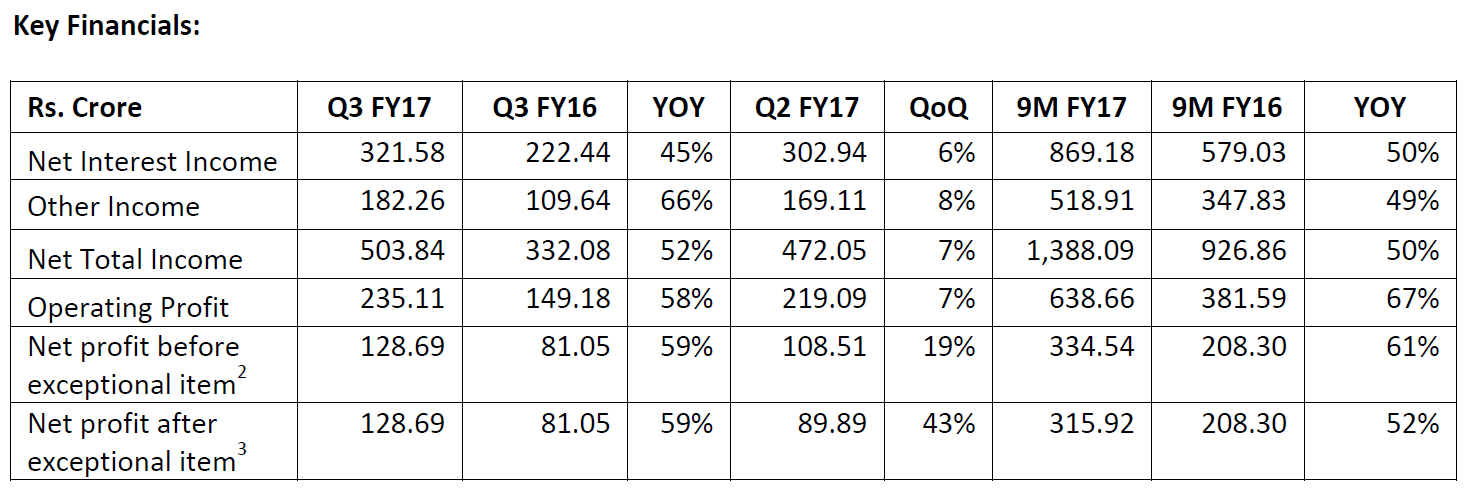

Any idea what other income is? It is higher than net profit. There is not explanation in the notes.

Gross NPAs are rising at 50%. NPA ratios are within range but that’s because they are growing denominator rapidly. ROA is still low. Banks in general earn at least 1.5%.

Usually Banks/NBFCs earn a lot of other incomes. These are processing fees, and similar income line. So they can be as high as 50% of interest income. No worries here.

I am more interested to look at the Gross NPA numbers, are they rising too very fast in absolute figure wise??

Overall it seems a decent (infact more than decent) set of numbers, can be a good three year bet…

Dont over analysis to miss the opportunity, sometimes you need to let the management do their bit. Any ideas on presence of any marquee investor in RBL?

Not only invested, Motilal guys seem to have a BIG conviction on this - when I checked few weeks back RBL Bank was ~9-10% in their Midcap portfolio(overall 2nd largest holding)

Axis had done a comparison how rbl can be the next indusind… will upload the report when i can find it.

Though one concern that people have is rbl has had too many esops which will lead to severe dilution in the next 2-3 years and growth in book value will not be as rosy as it seems… Ambit had flagged this in its pre-ipo note for RBL. In fact RBL has already increased its shares by about 3.4 million shares since IPO… about 7 lakh shares last week.

This trend is going to continue for 2-3 years, this is one major reason i didnt take a position in RBL when it was about 330