Tech update… Developing flag pattern. Correction can be till 460 (intersection of 50% Fibonacci and flag’s lower end.

Also, one can notice clear bullish divergence on the charts.

Tech update… Developing flag pattern. Correction can be till 460 (intersection of 50% Fibonacci and flag’s lower end.

Also, one can notice clear bullish divergence on the charts.

Of those who are not unnerved by the astronomically high valuation for this stock even when the company clearly has to rely on much higher risk segments as exhibited by its yield in the consumer segment thinking that this is a long-term bet because of the long-term banking opportunity, I must point out few things:

More importantly, I am unnerved for the long-term prospects when they almost everyday file an update with the exchange about investor meets. Such regular (almost daily) investor meets (while the CEO and top management may not be devoting much of their time to it) smells of a great desire to manage the stock price upwards which means that management may get cold feet to do things which are great for the long-term if they stand in contrast to the short-term performance. I ain’t sure how such an investor focused management will take such tough decisions in favour of long-term value creation when they meet investors almost daily (90% of investors in any company are anyways short-term oriented and will jump at the first sign of deep correction in the stock to retain their huge short-term profits earned on this name as well as not look stupid in front of their peers).

Overall I feel that this stock offers no margin of safety at this valuation. Raising money at high valuations and hence artificially increasing BVPS is not a sustainable driver of returns as ultimately risk management and differentiation in strategy along with execution with a focus on long-term performance and willingness to undertake short-term pain is the only way any BFSI company can be a winner especially given the digital age which is coming to us.

@8sarveshg I am bullish on the stock as i see the bank growing at 40 % with good control on the NPA . ( In th e banking sector I dont see too many doing this) . Also it has diluted shares recently at a price of 515 /- which is another positive.

Capital is food for the bank, whether you raise it as debt or equity (pros and cons of both being debatable). Capital is how you increase your lending (partly) and acquire more customers, to whom you cross sell products. Why would great investor interest in providing capital to the bank be a sign that the company wants to “manage the stock price upwards” and consequently not “take tough decision in favour of long-term value creation”? Have you seen any correlation between these announcements and jumps in the stock price? How does maintaining open capital raising opportunities not driven towards long term value creation?

How is raising money at high valuations in any way related to risk management and differentiation in strategy? Do you have any independent comments on risk management at RBL? And how is capital raising a detriment towards long term performance? What short term pain do you want the bank, or any bank, to take? What aspect of digital do you see RBL Bank ignoring?

I am not going to lie and say I do not wish to be argumentative - indeed I do, in a logical manner. I would be interested in some logical viewpoints, but yours assertions and conclusions don’t have a hair’s breadth of substance in them.

Hi

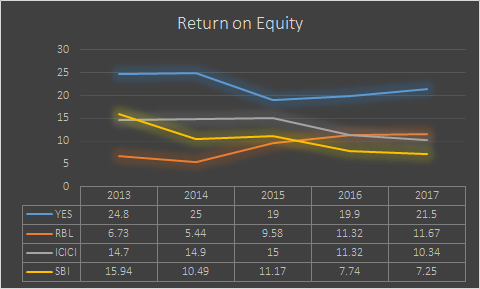

I am sure many of us have compared key numbers of RBL vs other private sector banks as well as some public sector ones.

Some of the observations I am pulling out from my notes basis:

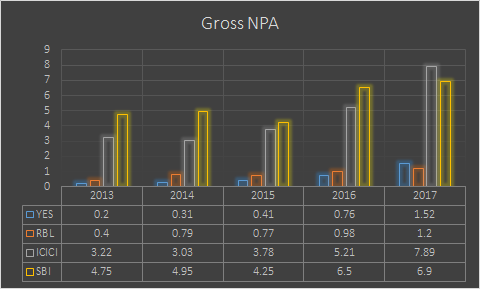

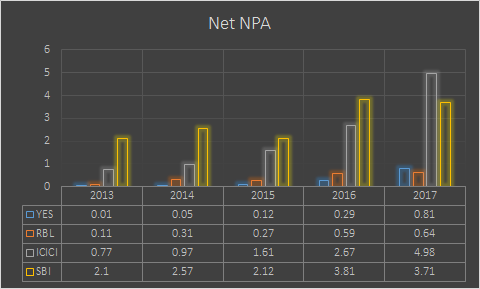

Yes RBL is a small sized bank but it appears to have the lowest GNPA & NNPA.

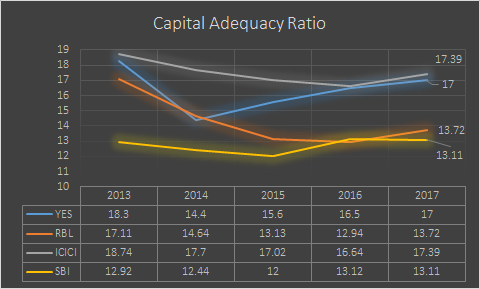

RBL is only second to Yes Bank on NIM as well as ROE. All banks have dropped on NIM or maintained it but RBL has increased it in 2017.

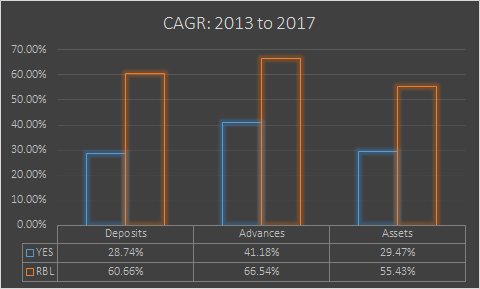

RBL vs YBL. Though RBL is roughly a quarter in size of YBL in deposits, advances and total assets its growth in same period has been far better. Agree that RBL is a small bank but it cannot be written off.

One of the members wrote about digital banking and fintech. I can assure you RBL is one of the most aggressive banks out there to partner on digital initiatives. The top banks which a fintech company reaches out to are YBL and RBL followed by Kotak and Indusind.

ICICI and HDFC have stuck to their own digital banking initiatives. They are very good at card issuance but when it comes to pure pure digital banking I feel YBL and RBL are better bets. Axis is no where in the picture, they have already had a disaster with an earlier product and now they have just acquired FreeCharge. SBI buddy I have nothing to talk about ![]()

Regards

Deepak

Disclosures: Invested. And I am from the fintech industry so have some background on the digital space

Capital is a food for all the BFSI companies but have you thought about why is RBL is perhaps which is meeting investors almost every other day, beating the next competitor in terms of highest number of investor meetings by a factor of maybe 10:1. For any listed company, BFSI or otherwise, can you please tell me the logic of having an investor meet almost everyday.

My thoughts are very simple and come from my reading and investing experience over the past many years - companies which are too investor focused are often unable to take short-term pains for the long-term gains. It is like you watch CNBC TV18 a lot then chances are you will trade more than normal, booking profits after a 25% fall and missing a 1000% appreciation (example of short term pain/long term gain). Now nobody knows the future for sure, but given my experience, this situation tells me that probability is not materially low enough (for me to invest or advice anyone to invest) that RBL would not fall in that trap. Emphasis is on the word ‘probability’, given my experience of such companies I feel that long-term profitable growth in case of RBL carries a lower than high probability (high probability is needed given extremely high valuations) and hence I would not pay these ridiculously high multiples - a multiple which is at least 1 or 2 SD above historical mean of private banks (which were always faced with great growth prospects in the past as well).

For raising money at high valuations, you need to grow fast at all costs because high multiples always need super-normal growth. With credit, however, high growth’s impact always comes with a lag of many years - ICICI or even PSU banks for instance were growing great in the past (similar to many microfinance firms where the industry itself grew by more than 50% in FY17 before the consequences of such a high growth got known, interesting even RBL is a great believer in MFI and I am sure that explains a good part of their profitability given that their corporate loan book is all low yield WC and God knows what the real risks in their MFI/rural book are, many BFSI people explain this by what we know as ‘evergreening’).

So the biggest short-term pain that BFSI companies undertakes at times is slowing growth itself especially when the environment for the area to grow is challenging - SME because of demonetization/GST/slowdown in GDP growth and rural/MFI for reasons we all know. Whether, RBL is managing it all this perfectly (given that it is priced to perfection or may be more than perfection), I have my doubts given my experience of watching too much investor focused firms. So yes, I may be wrong here but we are all creatures of what we have seen in the past. In any case at this valuation, growth or no-growth, good credit or not, I find no margin of safety, I am perhaps much more demanding of value and that’s my style that has served me very well in the past many years and I am happy even if I wrong in the case of RBL, but I feel that probability of myself being wrong is not materially low for me to put in money at these levels. To all those who feel otherwise, I can only wish all the best.

Different opinions make a market!

While being cautious is alright, at the same time we also saw some marque investors participating in its latest capital raising at 515 per share - CDC Group, Multiples Alternate Asset Management, HDFC Standard Life , Insurance Company, Global IVY Ventures, ICICI Lombard General Insurance Company, Steadview Capital.

I only want to know what should I add to my portfolio. Though I do not have a fixed target, would like to have 25-30% growth. If you look at figures, financial and micro-caps are leading amongst those who have such kind of yoy increase in business or profitability.

Banks have high reserve ratios but they do get capital/deposits at a lower rate and if they manage loans well, they have relatively lower risk than NBFCs. Now this leaves me only with RBL, Yes, Indusind & Kotak. HDFCBk will give slightly lower, albeit assured growth. There are plus and minus in each of these, but you cannot discount RBL just because of their meeting potential investors. They are just repeating what they have been doing since last 5-7 years. nothing new. And see their growth rate. This is a stock that can give more than 30% growth so do not brush its positives aside.

discl - Invested in all 5 Pvt Sector Banks mentioned above.

Add to it, interest rates are low and there are no indications around the world of them rising anytime soon… in such times one can bet on banks which needs capital to grow… and in next few years they can set up processes and IT and slowly improve there ROEs. And small size would help them grow at a faster pace.

NPAs need to be worried once you see any sign of NPAs rising… untill then its all theoretical talk (applicable to all fast growers)

Dear Deevee, Your post is indeed good. Can you please throw some light on technological capabilities of these banks. Which one has the latest tech or for that matter - Block chain, which will put these banks in a higher orbit of growth.

Thanks,

Prasad.

Hi Prasad

Caution: This is a long post

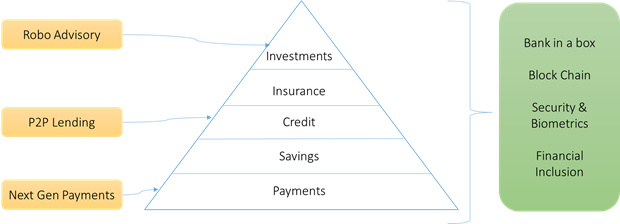

Essentially what is happening perhaps from 2010 onwards is a disruption of traditional banking activities. KPMG had come out with an outlook on FinTech in India last year. It identified 7 themes for India namely:

In my opinion I visualize this in a sort of a traditional Maslow’s hierarchy of banking and financial service needs. All the themes fit into the hierarchy triangle.

If you look around you will see that payments is where the traction is and that’s because it is the base of this triangle. Do refer to the Google BCG report on Payments in India in 2020. I have attached that too. The report says that Indians will make retail payments over $500 billion in the next 4 years and non-cash retail payments will overtake cash in 2023. I was a part of a global McKinsey study in 2012 which extended to 2014 where we studied the retail payments. The biggest land grab opportunity perhaps is in India! That’s what we have seen with everyone coming to party. This growth is actually being led by non-banks such as Paytm, FreeCharge, Airtel Money etc. Data says that these wallets (called non-bank pre-paid instrument issuers) do over 2 times the transactions than mobile banking transactions of banks.

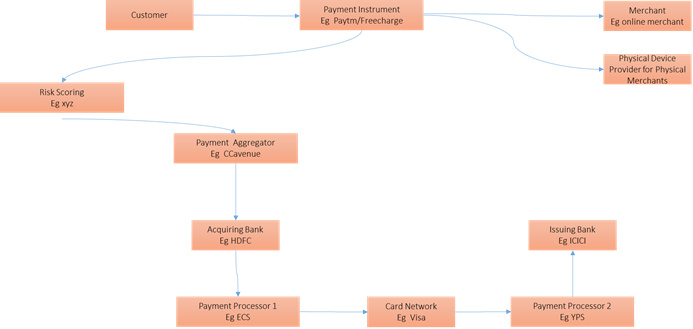

A payments value chain essentially consists of a variant of a 4 party model (this is what card associations such as Visa and MasterCard call it). In a typical 4 party model we have an issuing bank, an acquiring bank, a customer and a merchant. But the entities in a modern day value chain are aplenty!

Banks in this space are mostly used for payment processing or providing escrow services (meaning they hold funds of the pre-paid instrument issuer say Paytm with them, they earn float income on this amount and also earn certain transaction fees). Banks provide BIN sponsorships (Bank Identification Number, the first 6 digit on your cards). RBI allows only banks to be issuers of these 16 digit cards (these 16 digits are called PAN Primary Account Number). Thus a non-bank issuing cards needs a bank. This is one business line. Check out ItzCash you will realize what they do. Ratnakar is a leader in this space followed by YES bank. Every transaction is an earning here. ICICI and HDFC don’t do much of these programs. They rely heavily on earning interchange on their cards (interchange is the income which an issuing bank makes on every card transaction). Though smaller banks such as YES, Kotak, RBL, Indusind have comparatively smaller card programs and spends on cards they are providing digital services which are far better than the big three private banks. ICICI though is doing quite well in itself.

On the merchant acquiring side many people especially banks are not interested as it is not attractive from a pure financial perspective. The income is much lower compared to issuing. RBI is working on correcting this. Though entities like to have ‘on us’ transactions meaning both acquiring and issuing is done by the same entity, this has better financials. For instance American express, it is the issuer, acquirer as well as the network. Card networks are an expanding moat business as I see it. Wish I could invest in them! Trivia: Warren Buffet has investments in all three - Amex, MasterCard and Visa.

New age form factors such as QR codes (individual company codes as well as Bharat QR codes) are slowly gaining adoption, UPI has a poor success rate but it is picking up transactions on Peer to Peer transactions. Our payments industry has experimented on all sorts of form factors – visual, audible sound, ultrasonic, Bluetooth, simple mobile number, merchant initiated pushes etc etc. Honestly on which we can bet is a guess I do not want to make.

Leaving aside payments which you can read a lot in the Google report.

Financial inclusion is a separate animal altogether. If I were allowed I could upload my published paper (academic) on domestic remittances to show you the details. The need is very different in this segment. It’s a very big industry in itself. The form factor is primarily assisted mode. RBL and YES bank are clear leaders in this service. The big guys are not interested.

No bank I think is into P2P lending yet. They are focusing on personal loans rather. The tragedy is that they offer credit lines to ones who don’t need it. Risk scoring is the need of the hour. That is where the P2P lending and security and biometrics kick in. Again here the banks which stand out are YBL, RBL, ICICI, Indusind and Kotak for me. I believe this space will see great value addition from third party. Banks will not develop anything I am guessing.

Coming to insurance and investments part of fintech, banks are doing zilch in my honest opinion. One experiment here and there is what is happening. It is the non-banks who are doing something in this space.

Lastly the famous and mythical blockchain. One of the banks that is ICICI did a blockchain transaction for a cross border remittance last year I suppose. Block chain for us is a record keeping mechanism and not a payments mechanism as in bitcoins/cryptocurrencies. I was a part of the team in ICICI in 2012 which eventually did this blockchain transaction. I had done near real time remittances from Saudi Arabia to India using the plain vanilla SWIFT messages and back guarantee methods (you can check on world bank site now). Yes banks are running explorations in this space but I honestly don’t feel we are at any level compared to the developed economies in doing anything effective with blockchain so soon. There are a lot of proof of concepts by non-banks but that’s all and they are essentially bitcoin exchanges. RBI has set up a committee to study blockchain but I am not sure what’s the progress there.

Briefly summarizing bank wise what I have seen in my last 7+ years in this industry:

Apologies for the long post. But I feel there are so many more things in this space that it’s better to discuss ![]()

Also recommend if you want more details at a global level. Get a copy of the MIT’s FinTech Report here. And if it really interests you then you might like to enroll in their program.

Regards

Deepak

Sorry I am not being able to upload the KPMG report. The link is this.

BCG-Google Digital Payments 2020-July 2016_tcm21-39245.pdf (1.8 MB)

Really enjoyed reading your previous few posts. Very informative.

That’s amazing work Deepak.

How would you rate the NBFC’s strength and focus in the digital space? Any NBFC that you think is ahead of the curve?

Thanks again for the detailed explanation on bank’s fintech strengths.

Deevee,

An enlightening post indeed. Thanks for all the info you have shared.

As for me, I am seriously thinking on the following:

Recently Capital Float raises $45 mn in Series C round led by Ribbit Capital

RBL Bank has successfully built a strong partnership model delivering technology led banking solutions to a variety of companies across the retail as well as institutional space. Capital Float is one one of them.

Interesting times ahead.

vary well written disruption in traditional banking

As u know payment bank and e Wallet do not have margin so not viable at present

reference http://www.livemint.com/Industry/prilUXNB7Ll97ieR2QYvbP/HDFC-Bank-chief-Aditya-Puri-says-ewallets-have-no-future.html

p2p lending is having good margin but vary risky

ref http://www.forbesindia.com/article/weschool/peertopeer-lending-opportunities-and-risks/44055/1

Financial inclusion is I think Adhar base distribution of government benefit low margin business

ref http://www.thehindu.com/opinion/columns/C_R_L__Narasimhan/the-challenge-of-financial-inclusion/article6345276.ece

Issuing card is probably good margin business

I don’t see any disruption with good margin of profit May be its your domain so you can correct me

For me oversimplification of banking profitability is spread between cost of capital and interest earned

Prudent lending is the key for any bank

thanks

ashit

disclosure invested in kotak HDFC Fedral bank for more than 15 years

One very basic question. Would you not look at P/E ration for bank at all? I know P/B, ROE, NIM, NPA, GNPA, CAR, CASA should be checked for banks/NBFC. But how should one look at P/E

e.g. If P/B is 3.46 but P/E is 50 - Is this not expensive? compared to a bank trading at P/B 4 and P/E 30?

Hi

Caution: Another long post. Apologies.

Well I am guilty of showing only one side of the coin in my earlier post on the disruptions in retail banking. As pointed out I should shed some light into what matters for us as an investor in banking. I am sure most of us know how a bank functions and how it makes money. I will try to answer how these disruptions ‘could’ add value to banks and some pointers on how we value such companies.

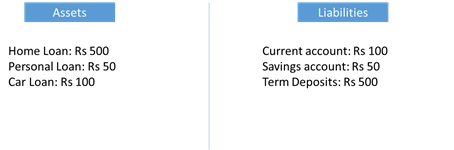

Liability vs Assets in Banks

Banks take deposits from their customers in the form of current accounts, savings accounts, fixed deposits and recurring deposits. This deposit base is ‘given’ out to the borrowers. So in a very simplistic fashion we can say the ‘debt’ or ‘liability’ which the bank has taken on its books by accepting deposit is invested by giving out loans to customers. The differential rate is the income which the bank makes. So the traditional language of debt in a banking parlance is the deposits base or the liabilities it takes on. The investment of this liability is in loans which are assets for the banks which earn a higher interest rate. A modified balance sheet (leaving equity aside) of a bank will look like:

Income Generation in Banks

From where all and what type of income does a bank have? Banks earn two types of income – interest income and non-interest income also called fee income. A bank when it takes deposits from customers receives float. This float after appropriate adherence to reserve ratios earn an income for the bank. This is called float income. For instance the bank is paying 4% interest to its savings account holder, this is a cost to the company. Basis this it can have a portion of its capital earn money in money market or basis this deposit base the bank lend to a consumer at say 12%. The difference in interests is the Net Interest Income at a high level. The bank has to match duration of its assets to its liabilities so that there is no asset liability mismatch. This is usually done by a team in treasury usually called the Balance Sheet Management Group. For overnight requirements or short term requirements many avenues are present to the banks.

The bank makes interest income from all forms of loans (which are assets to a bank eg home loan, car loan, personal loan, overdraft, education loan, the notorious corporate loans etc). Also from credit cards it makes interest income in case of revolving accounts or default accounts. Do read about revolving accounts.

On the fee income side the bank makes fee on transactions of all sorts whether its cheque issuance, cash collection, remittances, merchant payment acceptance etc. To get a glimpse have a look at the schedule of statement here for YES Bank. You will see both a fee income and an interest income component.

The wholesale side of banking is perhaps the most steady income generator for a bank, investment banking earns a lot of fee income, treasury income is also steady and last the retail side just manages to make money for small banks. But without having retail the wholesale side loses balance. Without retail banking ie deposit base you can’t grow as a bank.

The above section was to just give a background. Pardon me.

Let’s take each FinTech item and see what they can do at an overall level to the income of the bank.

Payments by wallets

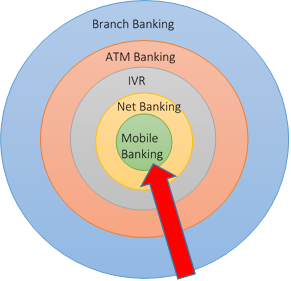

If you notice my last post I pointed out that banks prefer to be in the payment processing and escrow services fee business. Why? Escrow gives them a huge float income. For instance Paytm maintains say 500 crores with its escrow banker. By payment processing I mean that say when a consumer decides to use his wallet to send money to another bank account then IMPS service for money transfer gets used. For providing this IMPS service the bank charges the wallet operator. Another thing which I referred to is that banks do BIN sponsorship. Say a wallet issuer like Itzcash has an RBL BIN sponsored card. Whenever the card gets swiped Itzcash earns 1.1% of the transaction value and the BIN sponsorship agreement will say that 20% of this income will be that of the BIN sponsor bank. So in essence by virtue of being a bank it gets both fee income and float income by just entering into a BIN sponsorship. Look at RBL they have the most! Likewise banks earn from these fintech payment partnerships. Now coming to the fact of floating a bank wallet like say ICICI Pockets or an HDFC PayZapp (with due respect though Mr Aditya Puri has written off wallets but HDFC has two wallets Payzapp and has investment in Chillr I believe). The advantage these own wallets for banks give is 100% share of the fee income on transactions, they are akin to spends on credit cards. So more the users use their own wallets the better it is for banks. Again let me ask why? The more the user uses the more balances he keeps thus more float income. One more – why should he use the wallet to transact why not withdraw from an ATM and purchase with cash? Leave aside inconvenience, the banks always want customers to use their phones without contacting them to transact. The below diagram shows what the banks are trying to do that is to shift the customer to transact on their own using their handsets. Again why? Because of negligible costs in doing so. Our bank hates it when we walk into their branches!

Also when we talk about payment banks we should not write them off. I was part of the team in Airtel Money which got the license for the Airtel Payments Bank (the first one to get). Payments bank can earn fee income and have potential for cross sell. I believe telcos have an upper hand here as they have the distribution reach which is a huge asset to them in this payment banking space. Also please understand payment banks were created with the aim of financial inclusion. Financial inclusion is a very thin margin business. Thus size matters to a great extent. I am not aware how P2P lending is trying to make money but have some idea.

Now we have asked why we can’t use PE ratio to value banks. I purposely gave the above background on how banks make money. I would earnestly recommend you read Prof Damodaran’s 75 pager on how to value financial companies. I have attached the document but anyways quoting excerpts from it.

When we talk about capital for non-financial service firms, we tend to talk about both debt and equity. A firm raises funds from both equity investor and bondholders (and banks) and uses these funds to make its investments. When we value the firm, we value the value of the assets owned by the firm, rather than just the value of its equity. With a financial service firm, debt seems to take on a different connotation. Rather than view debt as a source of capital, most financial service firms seem to view it as a raw material. In other words, debt is to a bank what steel is to General Motors, something to be molded into other financial products which can then be sold at a higher price and yield a profit. Consequently, capital at financial service firms seems to be more narrowly defined as including only equity capital. This definition of capital is reinforced by the regulatory authorities who evaluate the equity capital ratios of banks and insurance firms. The definition of what comprises debt also seems to be murkier with a financial service firm than it is with a non-financial service firm. For instance, should deposits made by customers into their checking accounts at a bank be treated as debt by that bank? Especially on interest-bearing checking accounts, there is little distinction between a deposit and debt issued by the bank. If we do categorize this as debt, the operating income for a bank should be measured prior to interest paid to depositors, which would be problematic since interest expenses are usually the biggest single expense item for a bank.

The price to book value ratio for a financial service firm is the ratio of the price per share to the book value of equity per share. This definition determined by variables– the expected growth rate in earnings per share, the dividend payout ratio, the cost of equity and the return on equity. Other thing remaining equal, higher growth rates in earnings, higher payout ratios, lower costs of equity and higher returns on equity should all result in higher price to book ratios. Of these four variable, the return on equity has the biggest impact on the price to book ratio, leading us to identify it as the companion variable for the ratio. If anything, the strength of the relationship between price to book ratios and returns on equity should be stronger for financial service firms than for other firms, because the book value of equity is much more likely to track the market value of equity invested in existing assets. Similarly, the return on equity is less likely to be affected by accounting decisions.

Thus while quickly evaluating banks we must look at

Other pointers:

I diligently do not follow NBFCs. I used to hold Capital First but have exited it due to certain uncomfortable reasons. Not that it is not worth holding onto. Bajaj Finance I believe has entered into a partnership with Mobikwik. There you go. I see people like Angel Broking and Motilal Oswal going into something like robo advisory where the algo recommends investments/trades/capital allocation. Haven’t seen it up close though. On bank side like I said all private sector banks are doing well in the fintech space. Do not expect them to turn the tables in a year! We Indians love slow, extremely slow and steady pace ![]()

Sir I envy you having been an investor in HDFC for 15 years! An awesome investment it would have been.

Hope this quickly written out post made some sense.

Regards

Deepak

Valuing Financial Firms_Damodaran.pdf (103.6 KB)

Suggestions on Valuation Books: McKinsey on Valuation and Damodaran on Valuation.