Rain Ind is manufacturing only CPC and CTP besides cement . To my knowledge major requirement of Petcoke is imported. Rising of petcoke is affecting cement as well as DI pipe mfrs.

How can increasing raw material prices be positive for the company ? I believe pet coke is the raw material for the Indian unit of Rain which does the calcining of raw pet coke to produce Calcined Pet Coke (CPC). Rising prices of raw pet coke will rather have adverse impact on the gross margins of the company.

Folks

Let’s not jump the gun.

There is Fuel grade pet coke-FPC(used in cement manufacturing)

Green pet coke ( used in making aluminium smelters)

Rain is mostly fully integrated getting most of the intermediaries from its subsidiaries . GPC alone it procures…but this mostly a byproduct of crude…

Now coming to ban of FPC and import duty …it will have negligible impact on rain as cement is only 10% of rain revenue and more over they don’t import as far as I read for their manufacturing …

So don’t get carried away with the news …or buzz.

As far as rain ,CPc prices is all you need to worry about as long as it is intact eps will grow…and so as the share price.

It will be around 350-400 range for now and post dec results I expect result to be good and we can see 500 levels around Jan /Feb18 when results are declared.

And if markets reacts positively for loan refinancing we could see some momentum .

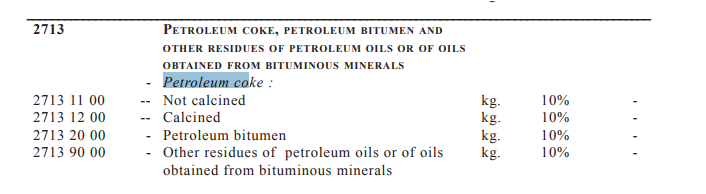

From import tariff perspective, there are only two types of pet-coke - calcined or not calcined (image given below) (no bifurcation of import tariff with regards to FPC vs GPC).

So, import duty increment from 2.5% to 10% will impact both Fuel Grade pet-coke (FPC) and Green pet-coke (GPC) equally as both fall under not-calcined.

So this probably should impact CPC India division of Rain (Vizag plant). I recall that Green Pet Coke (for aluminium anode production) is mostly imported as pet-coke from Indian refineries are not of anode grade quality. Now whether it comes from a third party or from a subsidiary should hardly matter as in both the cases this will hit their consolidated profitability.

CPC primarily used by Aluminum/Steel sector does not get Impacted either by ban on Pet Coke or does not have positives from the rise in import duties on Pet Coke.

There is confusion among the investor community about the Pet Coke required by cement industry, which has no connection with CPC supplied by Rain to Aluminum/Steel industries.

Anode grade (Low in sulfur and metals) type further calcined to produce Calcined petroleum coke (CPC) is used to make anodes for the aluminium, steel … Rain manufactures this CPC*

Keep an eye on CPC prices… Hope it crosses 10k and trades above that range for the next 6-12 months

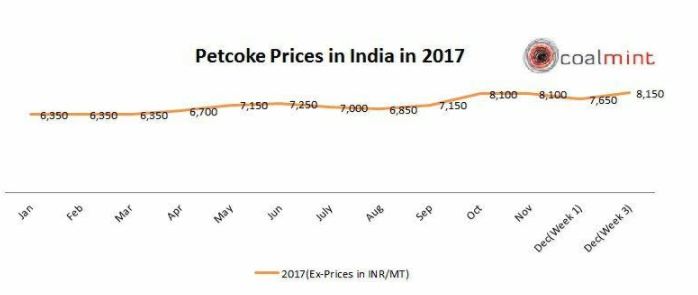

Where did you get the chart on coke prices …can you point to the website …and is there a way where we can track across the globe …particularly us and China prices

the chart you copy pasted is not for cpc but pet coke…completely different things…there is no public source for cpc prices unless you subscribe to one of the major research houses like platts.

Rain Industries has now been moved to A group in BSE (previously it was in B group). What are the implications of this? Does this automatically enable the stock to be part of F&O segment? Any other advantages due to this reclassification?

Mohanish pabrai opinion on Rain industry and tailwinds like

China’s pollution control policy

US corporate tax cut policy

Thanks

Ashit

Disclosure invested in Rain industry

Goa carbon posted stellar results. Goa has 75000 TPA of CPC where as Rain as 3 times more apart from CTP and Cement. expect a stellar results fr Rain as well.

BTW Goa equity base is very small and Debt compared to Rain. Strongly feel Post The Q3 results even the CMP will look cheap. Expect to see a EPS of 8 rupees for Dec… extrapolating for FY 19 will be approx 32 with the current PE of 25 , FMV will be 800 Rupees and Goa carbon is tailing at 40Pe where as Rain is at 25 , so even if we discount EPS for FY18 to be 25(which should be approx the FY17 EPS) , we should still see a FMV of 625. and if the PE expansion happens then easily 1000.

and if this was not enough … Dolly Khanna Increased the stake to 2.57% another 18L shares added in the dec quarter. Total holding is approx 85L shares for dolly khanna .

Thanks Sunil, from where you could find out the increased holding Dolly Khanna in Dec. quarter. It would be a useful source of information. Thanks in advance!

Seems she has gone out of the textbook to allocate more than 40% of her capital on a single stock. Shows her level of confidence and future potential of Rain.

use bajaar.me website to find shareholdings of famous investors and mutual funds. But this website can only track the Shareholding from BSE. It cant track holdings in NSE.

While Dolly Khanna has increased holding, all other funds like ICICI,

Reliance and Goldman have completely exited - this is intriguing - even

they have solid research capabilities.Do they believe that the high price

of CPC, being a commodity, is not sustainable and that it is only a short

term transient phenomenon.

… Dolly Khanna Increased the stake to 2.57% another 18L shares added in the dec quarter. Total holding is approx 85L shares for dolly khanna .

… Dolly Khanna Increased the stake to 2.57% another 18L shares added in the dec quarter. Total holding is approx 85L shares for dolly khanna .