How to check the graphite electrode pricing trend…any references?

Refinancing of old loans will aid interest cost reduction.

2 Likes

Why it is that Rain industries , goa carbon, HEG and graphite India are all following same trend…? What is the relation between them. Can any senior VPer please help me to understand.

Carbon products from Rain are CPC and CTP.

CPC is also produced by Goa carbon and CTP is also produced by Himadri.

So Rain moving along with Goa carbon or Himadri is justified.

5% of Rain revenue comes from graphite which is core business of HEG and Graphite India. In my view HEG and Graphite India moving along with RAIN is is not fully justified.

I agree…the only real commonality is that HEG, Graphite India and Rain India have all risen a lot in a short span.

Regards

SJ

Thanks Akshay and Jaju. So rain is independent of HEG and Graphite…but honestly most of the times the trend is exactly same…its like rain sneezes, HEG and goa & graphite gets a flu

2 Likes

HEG and Graphite India are the largest suppliers of graphite electrode which is in short supply and deficit situation is expected to continue for another five years. GI also has CPC plant for captive consumption. Acute short supply of graphite electode which is used in Blast furnaces in Steel/ Aluminium Ind. Upturn of Steel and Aluminium Ind and closure of plants in China is contributing for skyrocketing of Graphite electrode prices and fattening bottomline of HEG & GI.On the contrary Rain Ind is mfr of CPC CTP and cement. Multiple product;s demand supply dyanamics and contagion effect of Electrode shortage is dictating the stock price of Rain . IMHO, Rain Ind price rise in sync with HEG and GI is not fully justified.

Discl:Holding position in Rain , Himadri and GI .

1 Like

Any news on Rain for its fall in the last leg of trading…anyone having any info?

I picked up three near term triggers for Rain - one technical and two fundamental:

Technical - the share got added to MSCI index

Fundamental -

- US tax reforms (in final stage), add to Company’s cashflows

- Refinancing of debt at cheaper rates

4 Likes

People need to understand that 5% of Rains revenues come from graphite. Any investor on this thread talking about graphite prices influencing Rain’s bottom line should reconsider their investment thesis as it is completely flawed.

4 Likes

Adding More Details on the +ve Triggers

-

Moodys has Assigned Ba3 Ratings to the Proposed Senior Euro Term Facility Due 2025, which is a 1 Notch Upgrade from the Current B1 Ratings, which will Aid Rain Industries to Get lower Rates on the Refinanced Borrowings, So potentially it could be 6.75% To 7% Range from Existing Rates of 8.25% TO 8.50% .

-

The US Senate has JUST Passed the Republican Tax Reform Bill .With this Passing Corporate Tax might get Reduced to 20% which will be “Major Win for US Companies/Companies like Rain having Major Interests in the US”. The effect of which can defintely be seein 2018

-

Global aluminum market to be in relative balance from a slight surplus as estimated for full year 2017, a change from the second quarter projection of a slight surplus as reported in Alcoa 3rd quarter results . The improvement is mostly due to planned and actual curtailments in Chinese smelting capacity as well as increased Chinese demand which should keep the CPC prices stable…

and ofcourse the EV boom should contribute the demand of aluminium and why aluminium would be preferred over steel but thats a long shot …

5 Likes

Below are the key terms launched on Rain Carbon’s EUR loan.

It is significantly cheaper, taking advantage of lower EUR rates and liquid leverage loan market conditions in the US!

Loan is rated Ba3/BB by S&P.

- a seven-year EUR390m covenant-light term loan B (matures 2024), with price talk of 275bp-300bp, a 0% EURIBOR-floor, plus

- a USD150m RCF (revolving credit facility), with 5-yr maturity (matures 2022).

Loan should be finalized by end of December.

Source: Bank loan markets / Loan Radar

Disclosure: I’m invested

See above Sunil. Loan is coming in much cheaper, even with EURIBOR floor at 0.

Do you have a sense of cashflow impact (in INR crores) for US business with 15% lower tax?

Not sure to whom these are hidden but that is what Ambit thinks

3 Likes

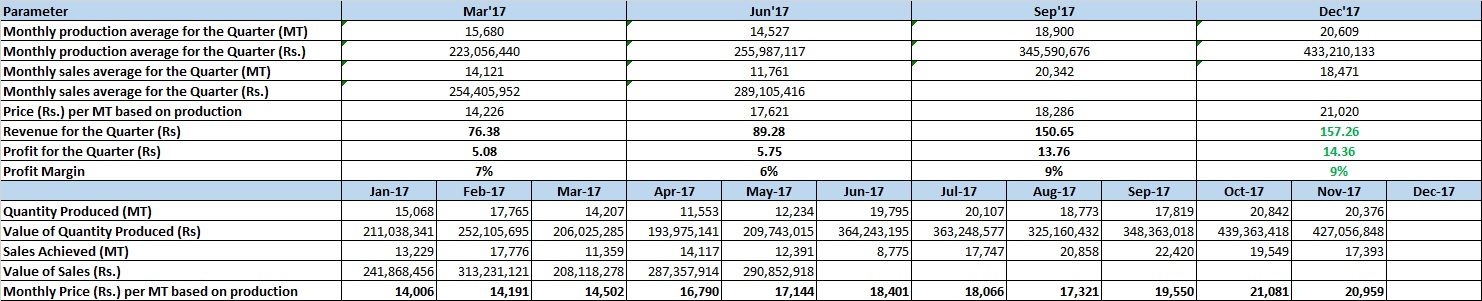

Goa Carbon has come up with the latest production and sales details of CPC for the month of Nov-17. Average monthly sales in terms of MT is down by 9.2% for the first 2 months of Q3 as compared to Q2, but the CPC price per MT shows a good improvement of 15%. Hence, overall I expect an improvement in the revenue figure in Q3, as compared to Q2. Using these figures, I have tried to make an estimate of Q3 revenue and profit, based on my best judgement. I am attaching below, my calculation sheet. Cells marked in Green color are estimates and I have assumed a profit margin of 9% for Q3 (same as Q2).

As a significant portion of Rain’s revenue comes from CPC, I thought of posting this detail here. I feel that, Rain’s Q3 revenue will be positively impacted by the increase in CPC price during Q3.

Disc: Invested in both Rain and Goa

4 Likes

Can you do a similar working on rain as well ?

Hi @pla7yer, Goa Carbon publishes its production & sales data for every month prior to 10th of the subsequent month. In case of Rain, there is no similar data available. Also, Rain’s product portfolio is much more diversified. Hence, I will not be able to come up with similar estimates for Rain.

2 Likes

For Q3FY18, the Goa Carbon has given only production volumes alongside its value. While they have given sales voumes for CPC, the value is not available for the same. Hence, it is not possible to calculate what CPC per MT stood during Q3FY18.

Yes @bhavveshh, My calculations are just estimates based on available info & assumptions based on trends and there can definitely be a margin of error (plus or minus). That way, we don’t even have the production figures of the month Dec-17 available right now, hence I assumed it to be the average of the figures of the first 2 months of Q3. As you can see from my worksheet, Goa Carbon stopped giving the sales value starting from Jun-17 onwards. The estimated revenue figure of Rs. 157.26 crores was derived using the following calculation: 150.65*(21,020/18,286)*(18,471/20,342).

One real benefit that came out of the above exercise was that, I got reaffirmation that, the CPC prises are on a steady rising trend since Mar’17, as mentioned in the following article and it should benefit companies like Rain: http://www.moneycontrol.com/news/business/stocks/rain-inds-good-results-confirm-strong-tailwinds-for-carbon-products-in-metal-industry-2434853.html. We also got the trend that, the demand for CPC has been more or less steady between Q2 & Q3 without any significant decline.

1 Like