My two cents :

I think its good that promoter are buying shares at ~CMP. So that the interests are aligned with minority shareholder. Though equity dilution per se reduces the overall return.

Also, I had read somewhere that bad promoters has an incentive to steal from other people’s money - but investing self money more or less covers that risk.

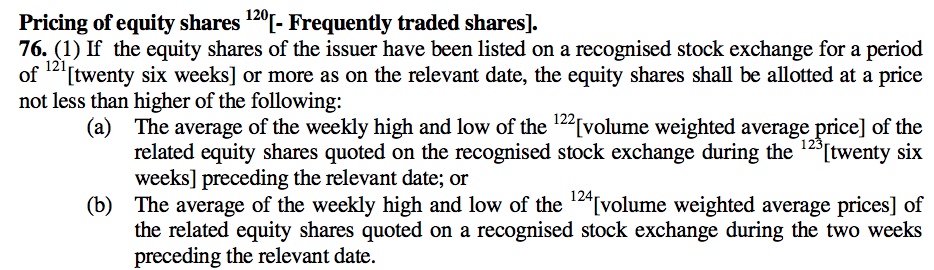

26 week average of the high and low of the VWAP would be much less since much of Aug-Sept was spent in the 150 zones so (a) is out which means (b) was used to arrive at the price as it would be definitely higher (the price has to be higher than the high of (a) or (b)). It looks like the price drop from 250 levels to 180/190 was very convenient for the promoters. Average of the high and low of VWAP for the latest two weeks would work out to be exactly the price the promoters are issuing the warrants at. Very convenient and advantageous indeed. And they only need to pay 25% upfront and can wait around 18 months to see if its worth converting. If the idea for the Warrants was Capital infusion, I would have expected the pricing to be higher.

They have already issued the current warrants at higher price. Remember, they had issued similar number of warrants at Rs.137 in November, but cancelled them couple of weeks ago and now re-issued at Rs. 208. If they have no concern for minority shareholders they could have converted the previous warrants.

The promoters are also investors and hence personally they would also like increase their Stake at reduced price so that they can acquire more shares. However earlier also they already had the opportunity to buy the shares @ 137.50 which was later rejected by the board. Though the offer price is less then the current market price it is substantially higher almost 50% then their earlier offer.

Secondly infusion of capital of Rs 208 Cr by promoters gives a lot of comfort to the existing investors and also the offer price of Rs 208/- will act as a huge resistance against any down fall in future.

The stock had rallied substantialy after the promoters announcing of capital infusion @ 137.50, lets see how the markets reacts this time.

As mentioned by @phreakv6 that the promoters will have a time of 18 months for conversion, I have to add that in worst case the promoters do not opt for conversion they will loose the 25% i.e Rs 52 Cr which will be an income for the company.

I would have also wished that the promoters should have come with a better offer however I am still happy that promoters are having confidence and infusing more then 200 Cr and that Rs 208/- will be a very very strong fundamental support for existing as well as new investors.

So now we have a growing company in a growing sector where we can discuss about the future prospects and value creation with a strong support of stock @ Rs 208.

Interesting how Steel Exports are up. The govt recently imposed a tariff duty of 20% on Graphite electrodes used in Arc furnaces in the manufacture of Steel to curb export so it could be used by local Steel industry. The measure in fact came into play because of complaints from local Steel producers. Interestingly, the same players that cried foul about higher Graphite electrode prices due to exports don’t mind exporting Steel at higher prices. In terms of “Parental Investment” in Ethology, this is the equivalent of a parent favouring one child over the other.

I wanted to summarize the issuance of warrants by the company in the light of various parameters -

The company has 15.43 cr outstanding shares with market cap of 3400 cr. It proposes to issue 1.125 cr warrants of 234 cr which is based on SEBI formula for calculation. When price of stock is Rs 220, warrant proposed at Rs 208. Promoter wants to subscribe to 90% of these(1 cr) to the tune of 208 cr.

What does it tell us about intentions of promoter. Does he look like minority shareholder friendly ? Company has capex plans and growth prospects are high.

The debt to equity is 0.42 at the end of 2017 which is approx 930 cr. They have reduced debt by 160 cr in 9M FY18 and planning to reduce by 300 cr in Q4 FY18.

The ebidta for Q3 was 150 cr and for Q4 they expect it to be 250 cr + which means they will be able to reduce debt.

Promoter shareholding reduced in Dec 2016 from 46.11% (50.73 % pledged) to 40.76%(52.96% pledged) . No of outstanding shares at that time was 13.56 cr and now it is 15.43 cr. Market cap was 521 cr at that time now it is 3394 cr. Though they have diluted equity but that has been more than covered by 6 times jump in market cap.

One important point to note here is that earlier they planned to issue warrants at Rs 137.5 in Nov 2017 which was also approved by votes. But on January 20 when the stock price ran up to Rs 241 they decided not to proceed with issue of convertible warrants amounting 0.91 cr shares.

They decided instead to issue at Rs 208 on 15 Feb 2018 for 1.125 cr shares when the price was around Rs 220.

My take is that business being a cyclical was stressed due to down cycle and had lot of debt issues. Now its seeing an up cycle may be, at least the last 5 quarters have been good and now they are in hurry to get out of all the debts etc.

But how do we see the issuance of warrants at this moment which when converted will be almost 7% of outstanding shares ?

But does that really matter when the business is seeing such a good time. Or does it matter ? Please share your thoughts.

Which type of furnace Prakash industries is using for steel making?are they using EAF which needs graphite electrode because sponge iron plant generally use EAF route.

They use induction furnace DIR based method dont require graphite electrode, cost of expansion is lower than BOF and EAF but quality is a bit on lower side and not used for heavy structure steel and flat products

@phreakv6 “Parental Investment” in Ethology, this is the equivalent of a parent favoring one child over the other.

I agree with your thoughts but we should also appreciate that generally the weak child is given more preference over the stronger ones. As we all are very well aware that Steel Industry had been bleeding like anything for the last 4 to 5 years and the bleeding had been to such an extent that most of them have even reached to the grave yard. The contamination has in fact reached to the financial sector also and there are stresses asset to the tune of Rs 2.0 Lac Crore.

It is now imperative for the government to give preference to the Steel sector and make it attractive so that it can find buyers for the stresses asset. The green shoots are very much visible with the aggressive bidding of Tata Steel for NPA assets of Bhushan Steel and Power.

With the global tailwind (China cutting its production and revival of global demand) and the preferential treatment of Steel Sector by Indian Government we can see stress resolution not only in Steel Sector but also in financial sector. It is just like killing two birds with one stone.

The resolution of Steel assets will at least take 18 to 24 months until which I am confident that the all the government decision will be heavily biased towards Steel Industry and which I think is also the need of the hour.

I think you had also endorsed the same logic in your previous post

Forbes article also points that after a 9 year down cycle a revival seems on the way in steel sector. Only time will tell but I am cautiosly optimistic. Also it made a point that there is lot of interest for steel assets set for auction. The cost of building one tonne steel plant will be around $750 to $800 but they can have a chance to get it at $500 to $600 in auction. Also they won’t have to wait to build capacity to meet the demand.

Last time Tata steel did a bid at the up cycle of steel, this time again they have bet big, I hope this time they caught it in the down cycle and do not repeat history.

An up cycle should be good news for Prakash as well.

OPERATING PROFIT MARGIN:

The operating profit margin has been continuously improving for the last 10 quarters which is positive

Sept 15 - 8.63%

Dec 15- 10.91%

Jan-16 – 11.38%

Mar 16- 9.73%

June 16 – 11.12%

Sept -16-13.25%

Dec – 16- 13.90%

Mar -17- 16.61%

Sept- 17 -18.31%

Dec -17 – 20.73%

Further the company has advised that due to higher realization in the current quarter the margins are going to further improve in Mar-18 to 25% . Also with the commissioning of Iron ore mines the margins are expected to improve further or even if it stabilizes at 22 to 25% there will be a huge positive impact in the bottom line.

NET PROFIT VS CASH FLOW FROM OPERATION :

Cumulative CFO for the last 10 years is Rs 2365.61 Cr and total Net profit for the last 10 years is Rs 1656.05 Cr. Depreciation and Interest expenses for the same period is around Rs 822.61 Cr & Rs 463.40 Cr. The cash flow from operation should be higher than the Net Profit over a long period which is a healthy sign. It gives a comfort that the profits are not merely book profits but are actually being converted in to cash. The cash generated from operation are being invested in fixed assets which is also a good sign. However large amount of funds are blocked in CWIP (Capital Work in Progress), which is definitely a matter of concern.

Debtors Level and Debtor days

The debtor level as on 31/03/2017 is RS 76.33 Cr where as on 31/03/2008 it was Rs 114.78 Cr. The rise in debtor level should be commensurate with the rise in sales figure. The annual sales as on 31/03/2017 were Rs 2173.50 Cr and as on 31/03/2008 it was Rs 1253.71 Cr. Although the sales has increased by 73% the debtor levels instead of rising have actually fallen by 34% which is good sign.

During the last 10 years the debtor days has also significantly fallen from 33.42 days to just 12.82 days. This is also a positive sign and in fact I was going through the data of other steel companies and I found that it is amongst the lowest of all Indian Steel companies.

Debtor days as on 31/03/2017 of other steel companies for comparison:

Tata Steel = 36.02 Days

JSW Steel = 27.24 Days

Sarda Energy = 17.77 Days

Kalyani Steel 119.86 Days

Inventory and Inventory Turnover:

The inventory level as on 31/03/2017 is RS 187.75 Cr where as on 31/03/2008 it was Rs 98.63 Cr. The increase in inventory should be commensurate with the rise in operations/sales figure. The annual sales as on 31/03/2017 was Rs 2173.50 Cr and as on 31/03/2008 it was Rs 1253.71 Cr. The sales has increased by 73% and the inventory levels have increased by 90%. As the inventory level is low the 90% rise in inventory level against increase in sales of 73% is in line.

The inventory turnover in 31/03/2008 was 12.71 and as on 31/03/2017 is 11.58. The inventory turnover is amongst the highest when compared to other Indian steel companies which is also a positive sign.

Higher ratio indicates that a company is able to rotate its inventory faster and its capital is not stuck in inventory.

Ideally, Inventory turnover ratio should be stable or increase with improving performance. Declining Inventory turnover ratio should raise the flags and an investor should delve deeper to understand its cause. If the investor is not satisfied with the outcome then he/she should avoid investment in such company and look for other opportunities.

Inventory Turnover as on 31/03/2017 of other steel companies for comparison:

Tata Steel = 2.34

JSW Steel = 1.91

Sarda Energy = 0.98

Kalyani Steel = 10.55

Debt Equity

The Debt to equity of any company should be ideally less than one. In case of Prakash Industries the Debt/Equity ratio as on 31/03/2008 was 0.51 and as on 31/03/2017 it is 0.42. The debt to equity ratio is comfortably below 1 and over the period of time it has reduced which is a good sign.

Debt/Equity ratio as on 31/03/2017 of other steel companies for comparison:

Tata Steel = 4.73

JSW Steel = 4.88

Sarda Energy = 4.06

Kalyani Steel = 0.32.

With the management target of reducing debt level down to the level of Rs 500, the Debt /Equity ratio is expected to further improve to 0.20, which will be amongst the lowest in the Steel industry.

INTEREST COVERAGE RATIO: the interest coverage ratio is also comfortably above 3.5 which is expected to improve further with reduction in DEBT

FIXED ASSET TURNOVER RATIO

The companies fixed asset turnover ratio is very poor and the main reason behind it could be the large amount of CWIP of Rs 1141.15 Cr which is almost 42% of the total fixed assets. This can be treated as matter of concern and also as an opportunity. The company should expedite to commission all the CWIP so that additional revenues can be generated. It would have really been beneficial if the company would have given details of the CWIP to share holders for better analysis.

The company however poorly ranks in ROE and ROCE, comparitive anlaysis of which I will be submitting later.

While I agree with the 3000 Cr for annual turnover, are you sure about 125 Cr for annual net profit, considering that that NP for the first 9 months is about 231 Cr.

Convertible warrants proposed to be issued to promoters on preferential basis @Rs208/- stipulates that they have to pay only 25% of the amount while subscribing to the warrants and the balance to be paid at the time of exercising the warrants. Company is not gettting the full amount now . Is it not against minority shareholders’ interest?