I analysed Prakash Industries at my blog -

http://kiraninvestsandlearns.wordpress.com/2010/12/12/prakash-industries-ltd-prakash/

I look forward to your comments, analysis and ruthless-dismissal-by-logic of this particular idea.

Fundamental rule I use yet again -

I look for stocks with a low P/E, low P/B, high ROCE (ROE, I think doesnat account for debt and hence a little skeptical), low D/E, good operating and NPM, consistent increase in Sales, EPS, OM and NPM over 3-5 yrs and finally low EV/EBITDA. If all this is good, then I look at the managementas track record. If all the above are satisfied, I then do a deep dive of the stock. As you realise by the above criteria, I hate losing money even if that means I overlook a few so-called multibaggers.

I use normal screeners to find such stocks. A list of screeners can be foundhere.

One such stock was Prakash Industries Ltd.Prakash Industries is a steel maker with facilities in Champa and Raipur in Chhattisgarh. Besides producing steel (0.7 million tonnes per annum or mtpa), the units also make sponge iron (0.6 mtpa) and billets (0.5 mtpa). The company also has a 100 MW captive power unit.However, Prakash does not sell billets or sponge iron, as these are further processed into value-added products such as structurals, thermo-mechanically treated (TMT) steel and wire rods (higher margin products, typically). The company also has a coal mining capacity of 1 mtpa.

The company is expanding its sponge iron and billets capacity to 1 mtpa by FY13. Not only this, the company is planning on doing backward integration by getting into iron-ore mining which would reduce its cost by a substantial percentage (estimates range from 40-60%). They are also venturing into merchant power business by setting up a power plant with 625MW capacity over the next 5-6 years.(I am kinda skeptical towards these 3 year and 5 year plans. Variables might change so dramatically over these time periods (like change in environmental policies, license policies, macroeconomic factors like steel prices etc.) that some of these ‘planned’ exercises might not turn out to be practical. Since I am not a seer, I shall restrict myself to the past data and the capability of the management to produce higher returns given any economic condition (typically the past 5 years. Assuming a going concern than all these fancy plans, we now move on to the analysis).

Moving on to the more boring part of financials than the interesting strategic part of planning,

CMP: Rs. 100.05

Market CapINR 1,236.2 cr

Book Value per share 117.57

Enterprise Value per share 120.49

Total Foreign Holding 14.75%

Total Institutions Holding 3.34%

Total Non Promoter Corporate Holding 16.03%

Total Promoters Holding 50.29%

Total Public & others Holding 15.59%

Again, Walter Schloss’s criteria of Promoter holding >= 50% is satisfied.

Moving along,

Parameter Value Industry Median Industry Weighted Avg

Price-to-Book 0.86 2.08 4.91

EV / EBITDA 4.12 15.18 17.32

Price-to-Sales 0.79 2.63 2.97

Financial Leverage 1.16 1.66 1.73

Interest Coverage 11.72 5.62 4.94

Adj Price-to-Earnings4.38 37.96

Debt to Equity 0.15

Back to our fundamental criteria,

Low P/B (0.98), Low P/E (4.38), High interest coverage (11.72), Low EV/EBITDA (4.12), Low D/E (0.15).

The current parameters look excellent. Let’s go back for the past 4-5 years to check on operating margins, return on capital etc.Letas look at the history of managementas performance, rather than a single snapshot (just to ensure we are not under the influence of some accounting shenanigans or one time fad market).

Variable FY06 FY07 FY08 FY09 FY10

Net Profit Margin 8.94 14.23 15.86 13.37 17

Operating Profit Margin 19.10 21.29 22.70 19.50 17.2

Asset Turnover 0.70 0.80 0.96 1.17 0.94

Return on Assets 6.29 11.39 15.20 15.59 16

Return on Equity 13.62 19.99 21.05 19.43 18.6

Capital Employed 1128.81 1161.67 1307.03 1309.82

ROCE 9.39 15.37 18.41 20.25 22

Debt to Equity 1.15 0.75 0.38 0.25 0.15

ROCE has been consistently increasing on an average at 20% over the past 5 years (inspite of increase in capital employed - extremely good sign). Debt is reducing consistently over the years (and close to zero, except for the FCCB bonds). Return on Assets has been increasing consistently and so are Operating and Net Profit margin (except for a slight dip last year).

The above analysis suggests that the company is extremely healthy at an extremely attractive price. The past 5 year data suggests that management has the capability to ride through cycles and recessions pretty comfortably. On top of that, Promoter holding is greater than 50% which is, most of the time, a very comforting sign.

Risks

-

They primarily operate in the steel business. They are diversifying (or backward integrating, if you want to call it) into iron ore mines and power. These businesses are extremely sensitive towards licenses, govt. policies on environment and in general, the macroeconomic demand for steel.

-

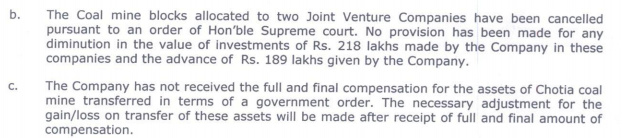

The management credibility has been questioned by a CBI enquiry on the use of captive coal mines (the rumor is that the management has sold a lot of coal on a private party basis for thousands of crores). The management has however clarified that the company has produced 2.44m tons of coal from Chotia mine till FY09. Of this, it has utilized 1.27m tons for production of sponge iron, and the remaining washed RoM and middlings were used for power generation and all these records were verified by Coal Controller to the Under Secretary of Ministry of Mines, Govt of India. However, doubts remain in the short term.

Opportunities:

-

There were talks that Prakash Industries wanted to buy out Nova Iron and Steel (which has a sponge iron plant near Prakash Industries plants). This might boost capacity. However, both managements declined to comment on this.

-

There were also rumors that Arcelor Mittal was interested in a stake of Prakash Industries way back in March. However, no other details are available. If any such rumors surface again, we might see an upshot in the stock.

I would term Prakash Industries as a Value Buy at current levels. Inspite of an extremely healthy business and decent outlook, it is quoting at 52wk lows (52wk high is approx Rs. 240). I would see a healthy return of 20-25% from current levels over the next year, if not more.

[As an aside, I analysed some of the peers of Prakash Industries - Welspun Corp, Nesco and Balmer Lawrie. Balmer Lawrie is an excellent stock (analysis by Rohit Chauhanhereandhere). I don’t trust Welspun Corp’s management and hence am not comfortable investing in that stock although it has decent numbers. Nesco is an interesting company. Excellent numbers. Very good Free Cash Flow. However, its more of a real estate play than a steel play. Analyzing real estate stocks is beyond my competence as of today (although am learning bit by bit). Unlocking of real estate might take a ton of time too. If someone could (or already did) analyse Nesco, please point me out to the analysis. I’d be grateful to you]

_Disclosure:_I donat hold any Prakash Industries stock as of today. And more importantly, this is not investing advice. Please do your due diligence before investing in Prakash Industries.