It seems the company has now turned around

The margins have improved substantially and the management is positive that there will be further improvement in margin. The current capacity utilization is around 80% and the management is positive of increasing it to 100% so conservatively the sales for next quarter will be around 900 Cr and accordingly PAT will be around 115 Cr. Further with the commissioning of mines in April2018, the margins are expected to furthr improve in next financial year. I expect FY 19 PE to be around 30 and with a PE of 12 the share can easily reach to around Rs 350 in next 12 months i.e 60% upside from this level… Disclosure invested since Aug 17 from the levels of 110 and added gradually, average hold price 145.

In the words of Porinju Veliyath the company was categorized as so called Chor Management with all negatives right from cancellation of Coal block, Check Dishonor case, Syndicate Bank Bribery case, Shell company , CBI investigation for allocation of coal block etc etc… I think now all dark clouds are clearing out and now with its performance the company is in the radar of value investors

1 Like

Management has guided 60% growth with 25% ebidta margin, so Revenue ~ 1000Cr and EBIDTA ~ 250Cr next quarter. They will have ~ 50Cr depreciation and interest expense, so pre-tax they will do 200Cr. Not sure whether they will pay tax next quarter or not, if not than they should do 200Cr odd PAT next quarter.

1 Like

Yes, there have been loads of negatives with the company in past. Came across an article about illegal mining - http://archive.tehelka.com/story_main51.asp?filename=Ne031211Mining.asp

Not sure what is the current status of the CBI case.

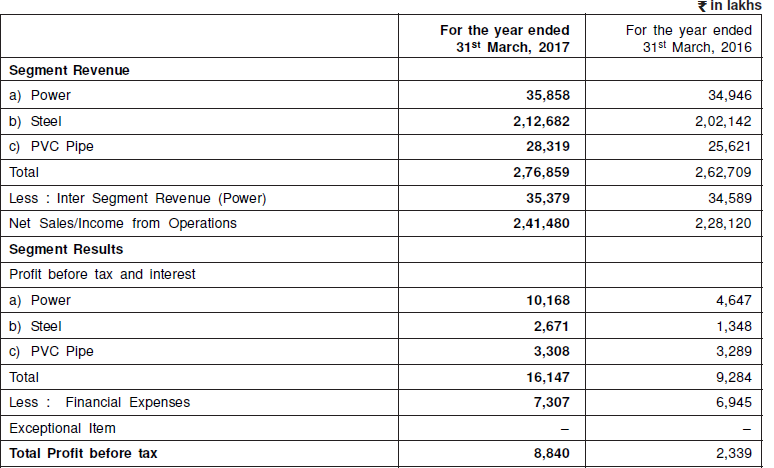

I also don’t understand as to why the company reports a substantial income from power (if one looks at segment results) rather than steel? Is it for the taxation benefit on the power plant? Also, the tax has been zero, need to understand why the company hasn’t been paying taxes?

In past they defaulted on loans and FCCBs too.

It’s interesting to see that the markets were smart to give a very low PE to the company despite reporting substantial profits during 2010 to 2012 to 2014 period before the profits went away.

But anyways, now the cycle has turned positive and as the steel prices have doubled and some of their long overdue capex has got completed they are seeing good times:

10 Likes

Mutual funds hold only 35000 stock in the company - as per Sept 17 filing

in BSE.

As per my analysis the company is having outstanding MAT credit of Rs 240.86 Cr.

And as per Note 42 in Annual Report : “Considering the future profitability and taxable position in the subsequent years, the Company is recognizing Minimum Alternate Tax(MAT) credit entitlement as an asset and is carrying the same in its accounts under the head of Non-Current Assets. In case the credit entitlement is not availed by the Company within the time limit prescribed under the Income Tax Act, the same is set off against the Retained Earning.”

The company has set off tax liability against the MAT credit available. The outstanding MAT credit of Rs 240.86 Cr is a huge positive for the company if it is reporting higher profits with high tax liability because the same can be set off against MAT credit…

Experts opinion invited for further clarification.

Ayushmit, regarding default in FCCB loans , while going through the past Annual Reports I have observed that the FCCB default coincides with the cancellation of Coal Block(By the orders of Supreme Court) allocated to the company. This is important because upon cancellation of coal Block the company was required to pay around Rs 250 Cr .

As per their Annual Report for 2014-15

“Consequent to the Hon’ble Supreme Court order dated 24th September, 2014, the

Company has paid the additional levy amounting to Rs.234.22 Crore on the coal

extracted from the operative coal block till 24th September, 2014 and will also be

paying additional levy in respect of coal extracted till 31st March, 2015 by 30th June,

2015. In terms of Section 198 of the Companies Act, 2013, the additional levy paid by

the Company will be treated as legal liability and liable to be deducted, while calculating

net profits for payment of managerial remuneration. This one time aforesaid payment,

which is exceptional in nature and is not related directly or indirectly to performance

of the Executive Directors of the Company, resulted into inadequate profit in the

financial year ending 31st March, 2015”

This event is important because in my opinion the FCCB default was due to sudden cash outflow of the company for Rs 250 Cr. The company might have conserved this cash for FCCB repayment but had to default on account of meeting statutory obligations under directions of Honble Supreme court .Had there been no cancellation of Coal Block, the company could have timely repaid its FCCB obligations

5 Likes

While going through their past Annual Report I had observed that the companies operational performance was significantly better then the market had priced… however there had been flow of bad news around the company one after the other because of which the shares did not performed upto their potential… I am trying to analyse all the bad news and if it comes clear then planning to increase my investment in this company… I had already done some analysis which I will share in this forum…

For the FY 2014-15, in-spite of paying Rs 235 Cr due to de-allocation of Coal mines , the company reported a PAT of around 10 Cr . I found the companies performance to be consistently good even during the down trend of Steel Industry, which I think is really commendable.

5 Likes

Company is creating MAT credit against its current tax liabilities. The MAT credit is carried as an asset on the balance sheet, to be set-off against future tax liabilities. Came across this explanation in the AR for FY 2017 regarding taxes:

Company seems to have created MAT credit of ~Rs. 240 cr. (as on March 31, 2017) in this manner, which is shown as an asset in its balance sheet:

Now, this MAT credit which is shown as an asset is available for utilisation in future only if company makes sufficient taxable profits within a specified time period. Else, this has to be written off against the net-worth, which is what the Company has done to the extent of Rs. 17.09 cr. during FY 2017

Bulk of the revenue from power is eliminated as inter segment revenue, as power is being consumed captively, and very little is sold externally. However, for segmental profits purpose, company seems to be taking transfer price of power to steel division on arms length basis (possibly at grid rates):

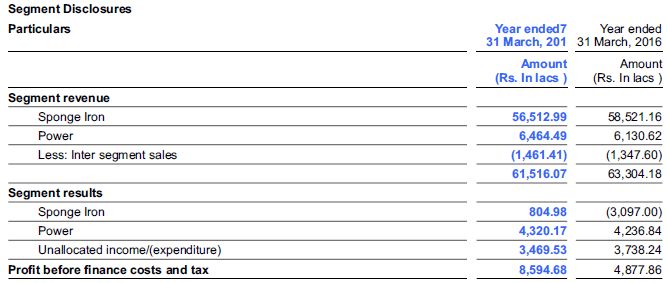

Not sure of the reason for showing higher profits in power division, however, this seems to be accepted practice, as even Tata Sponge is doing something similar as seen in their segmental performance from FY 2017 AR:

Most of the power is generated from waste heat/flue gasses of sponge iron kilns and by using coal washery rejects, etc. so cost of generating power should be very low

Discl: Have tracking position

4 Likes

The company will be generous in reporting profits in coming years because then only will be able to utilize the MAT Credit of Rs 240 Cr. If the MAT credit of Rs240 Cr available with the company is not utilised then the same has to be written off.

So going forward we can expect high profits and lower tax outgo on account of huge amount of MAT credit available with the company i.e Rs 240 Cr. We can expect substantial improvement in EPS in future.

2 Likes

As per latest Annual report “Pursuant to the cancellation of the Choita coal mine of the Company vide Hon’ble Supreme Court’s Order, the assets pertaining to this mine have been vested with the new owner in terms of a government order. The book values of the assets transferred to the new owner have been aggregated and shown as claim recoverable in the Books of Account.The outstanding balance as at 31st March,2017 is 2165 lakhs. Necessary adjustment for gain/loss will be made in the Books of Accounts on the final settlement of the compensation claimed by the Company.”

The company may receive Rs 21.65 Cr (or more or less)from the Government against its investments made in Chotia Mines which was de allocated as per orders of Honble Supreme Court.

1 Like

I was going through the orders of SEBI, wherein Clean Chit was given to the company in matters pertaining to shell company , and i found that some queries raised by SEBI were also pertaining to allocation of Coal Block which is also under CBI Scanner.

One of the queries of SEBI was :

"Manufacturing capacity and Net Worth of the company that has been represented to the Ministry of Finance/Government at the time of each application of Coal Mine allocations (Considered as reference period)"

Date of Application of Coal Mines : 12/11/2001 (Chotia Mines)

25/09/2004 (Madanpur Mines)

12/01/2007 (Fatehpur Mines)

The company had submitted suitable reply in this regard and which has also been duly admitted by SEBI, this gives a very strong argument that when one statutory authority has admitted the facts the other authority will also have to accept the same.

Going by this logic the overhanging risk on the company regarding CBI case on Fraudulent allotment of Coal Blocks can be mitigated.

I understand that when company utilise the MAT credit, it is amortized in profit & loss account to the extent it is being utilised. But I don’t see any tax charge in the PL. Though there may not be any cash outflow but the MAT credit should be charged to PL.

I think in terms of accounting, MAT credit utilisation against provision for tax is a balance sheet to balance sheet item and should not impact the P&L no?

For instance if the company had 100 PBT in 2016 and recognised 20 as MAT credit for additional tax that it paid that year and for instance in 2017 it had 150 PBT on which it was meant to recognised 50 as provision for tax (33% tax rate). Then out of this 50 provision, 20 MAT will be adjusted and the balance 30 will be paid in cash.

So to that extent I don’t think MAT credit is amortised in P&L (unless I’m totally mistaken), on the other hand. Deferred Tax asset and Liability are recognised in the P&L as the timing difference converge or diverge.

1 Like

As per latest Annual report of Prakash Industries:

"Considering the future profitability and taxable position in

the subsequent years, the Company has recognized

Minimum Alternate Tax (MAT) credit as an asset by

crediting the Statement of Profit & Loss and including the

same under “Other Non-Current Assets. In case the

Company is not able to utilize this credit within the time

limit prescribed under the Income Tax Act, the same is set

off against the retained earnings as tax credit pertains to

an earlier year”

It means that if they are generating Sufficient profits then they will utilise proportionate MAT credit as an alternate to Tax Payment , this treatment of MAT credit will be in P&L ,

Where as if the company is not generating sufficient profits then will not be in a position to utilise the available MAT credit and it will lapse over a period of time, however if it is not utilised and has to be written off then the same will not be routed through or Charged to P&L but will be set off against retained earnings therby having no effect on the P&L of the company.

In my opinion, as the company is showing a substantial improvement in its profit it will be able to utilise the entire MAT credit of Rs 240 Cr over a period of time i.e it will save a tax outgo of around Rs 240 Cr over a period of time which I think is a huge positive for the company.

Experts opinion required…

Going through balance sheet since 2008…will share my observations on the company shortly…Joining the dots to get understanding of the company as well as management

3 Likes