This might help http://sanjaymeena.io/investing/analyze_banks_nbfcs/

Courtesy: @sanjaymeena

That statement has more to do with anticipated stock price movement post announcement/issue rather than fundamentals.

Stake Sale cancelled. PNB will continue to be the promoter.

Sale to both General Atlantic Varde Holdings has been terminated.

As per the notification issued by PNB “PNB will continue to be the sole promoter of PNB housing and stay strategically invested in the Company. PNB strongly believes in the growth story of the Company and will continue to support the business and its management in pursuing their growth plans. Further, PNB will continue to provide branding support till PNB is the promoter of the Company”.

The direct support of the second largest PSU bank, and indirect support of the Govt. of India, and major stake by Carlyle, provides a unique combination, creating one of the great growth stories of our time, worthy of emulation.

The sale did not go through only because RBI approval was not received in time. Also, my understanding is that PNB mentioned it will be the promoter till it sells its stake which is driven by the government and the board of PNB has very little say in this (ie government may deny to recapitalise).

The clarification mentions that PNB will continue to be the sole promoter of PNB housing and stay strategically invested in the Company. This implies that there will not be any further attempts to dilute the stake in the near term, also since PNB believes in the growth story of the company.

In this matter, it is the prerogative of the board of PNB to take the final decision. It was the board which decided not to divest in their subsidiary PNB gilts, stating that they wanted to grow that business. Even though the Govt. may give guidelines for loss making banks, it is up to the board to make the final decisions. Since PNB has already started making profits, there is no immediate need for further funds through divestment.

My statement indeed was related to Fundamentals. I will explain with a simple example.

Lets take two companies

Now both companies want to raise 20 cr equity capital to fund the growth. This is how it will go.

ABC has to issue 20 Lakh new shares at price of 100 (PB 2X) which results in 1.2 cr equity share base and dilution for existing shareholders will be approximately 17%. The new book value per share comes to 70 / 1.2 = 58.33

XYZ has to issue 10 Lakh new shares at price of 200 (PB 4X) which results in 1.1 cr equity share base and dilution for existing shareholders will be approximately 9%. The new book value per share comes to 70 / 1.1 = 63.33

Did you see what happened? BV per share of XYZ is more than ABC after equity raising. Shareholders of XYZ faced less dilution than ABC because of higher valuations. And on top of that due to expensive valuation, shareholders will eventually benefit more.

This was a very simple example. But things happen in real world the same way. Just notice how raising equity at high multiples benefited shareholders of HDFC Bank, Bajaj Finance etc and how it’s counter-productive for PSB’s where PBX is 1 or less.

Note - Go through threads of Gruh, Bajaj Finance, Yes Bank on VP to understand more on how to value financials.

Thanks for your explanation. Point taken.

Also, please note that my statement earlier was not meant to mock you in any way.

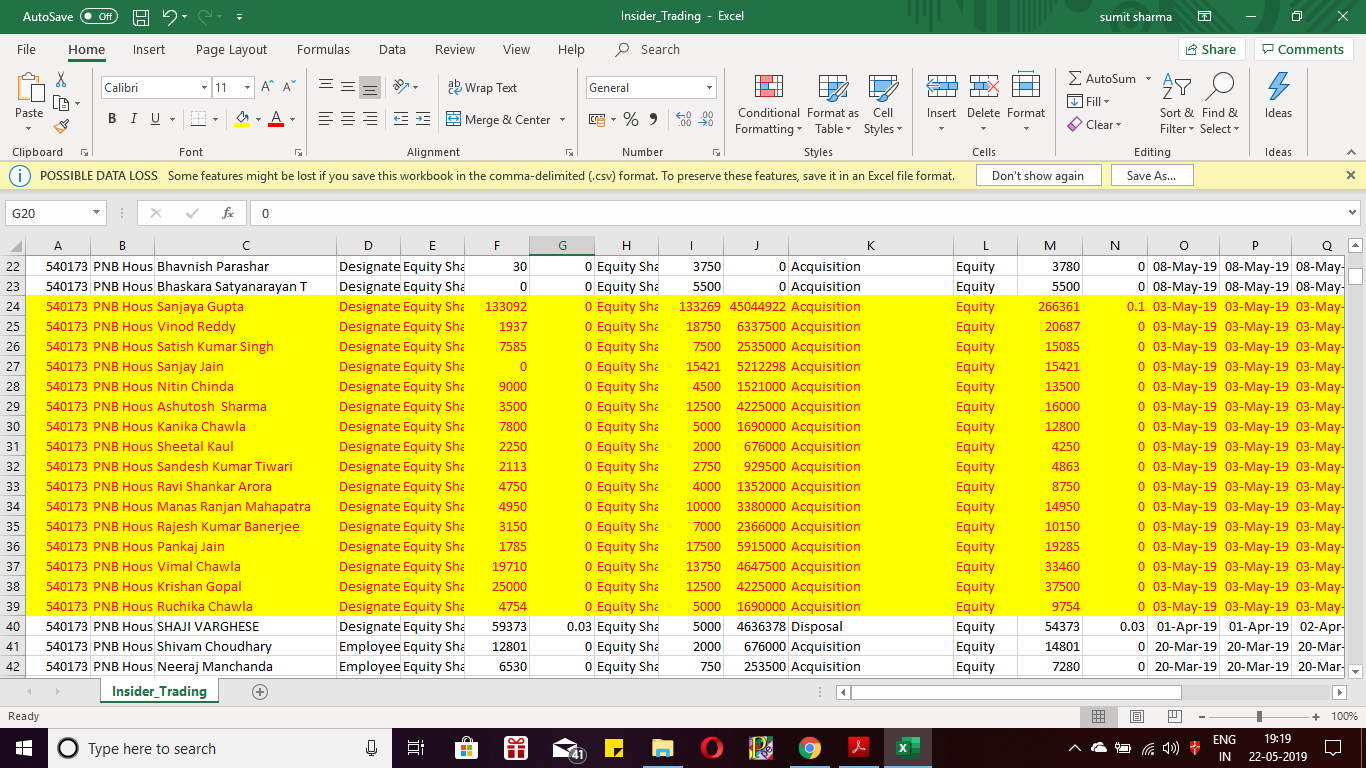

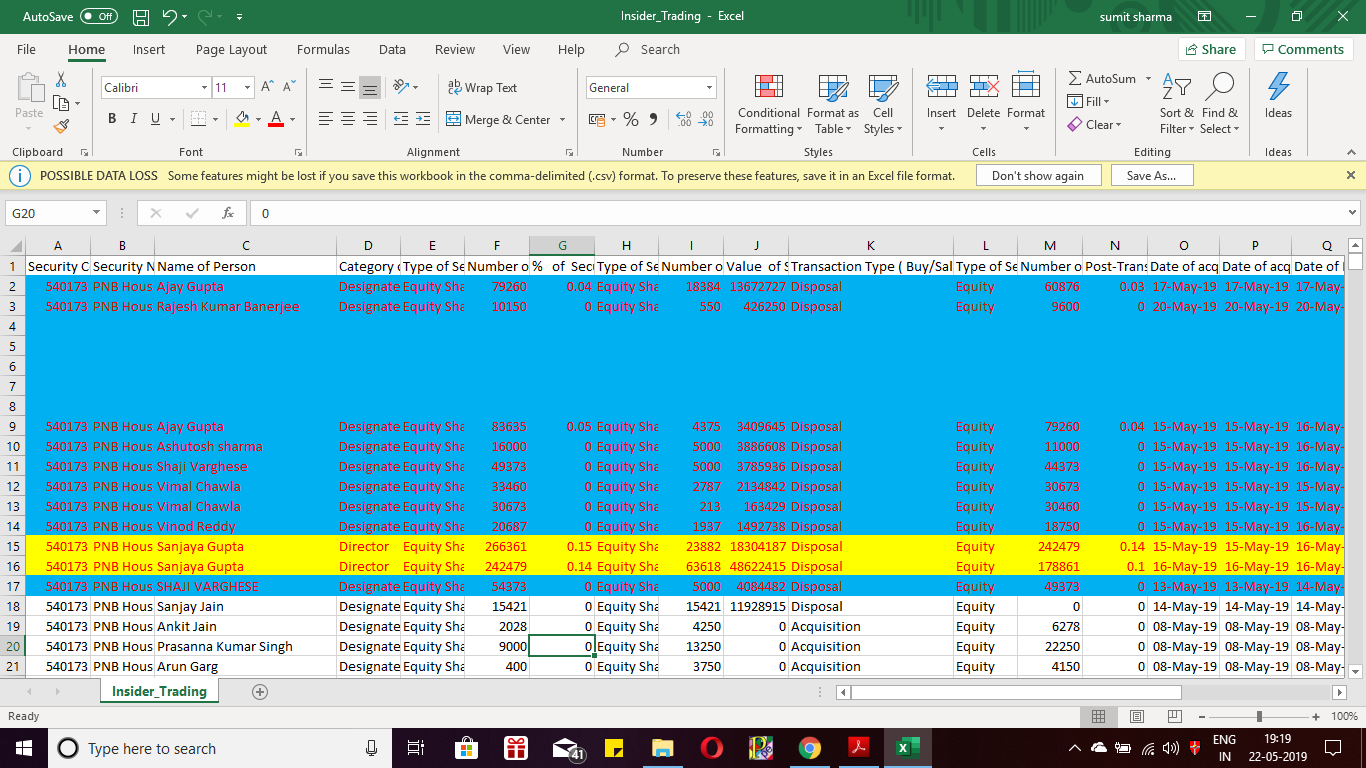

Hii fellow investors, i recently invested into PNB Housing attracted by its low price and high growth…Just wanted to bring case of insider trading by Director Sanjay Gupta and other employees…

On 3rd of may 2019, Director and other employees purchased huge amount of shares at price below 700…Director acquired 4.5 Cr worth of shares while others betn 50lac to 10 lac…

This was before closing of trading window…

However 12th may onwards, director has disposed off shares worth 5.5 cr and other employees are also following the same…this has been at a price of above 760…

i feel this has been purely a case of insider trading and reflects cheap standards of corporate governance…a company in a difficult sector with low corporate governance is difficult to trust…

i am attaching a screenshot of the same downloaded from BSE for reference…

Why ? Idont think anything wrong with it.

They aren’t promotor / owner of entity …and they are disclosing what they doing in terms of buying and selling it.

What’s exactly wrong in doing it ?

I can treat it as morally wrong if any promotor owner does it in his own entity but in this case he isn’t promotor owner .

Correct me if I you think my views aren’t correct and share yours too

Yeah, there is nothing incorrect technically…

actually i added more on the lower price when i saw that director himself is buying…now that logic behind my investment has become invalid…

But as pointed out by Bharat…i have got it all wrong…

Thanx a ton Bharat for pointing out the ESOPs…

If these are ESOPs I wouldn’t worry about it. Rajeev Jain of Bajaj Finance has sold his ESOPs immediately after they were allocated for the last 5-6 years and we all know it has not impacted either the share price or the performance of BFL. Some CEOs don’t like to hold shares of companies they run there is nothing right or wrong about it

PNB housing among the few good NBFCs which improved profits and loan quality last year says Debashis Basu of Moneylife

Check out @Moneylifers’s Tweet: https://twitter.com/Moneylifers/status/1137947327870537728?s=09

It is astonishing to see that when cockroaches (scams)are coming out one after another from DHFL, Indiabulls Housing , Piramal Enterprise , PNB housing stands tall though there are much talk in Pnb Housing Developer Loan book in SM . Till now it seems it is more ethical and well professional than DHFL, Indiabulls and PEL

As Debashis Basu in that article rightly said that PNB housing , Canfin , LIC Housing are unaffected in liquidity crisis but surprised to see of Mr Piramal’s response to RBI for 10% share of Loss. Piramal management used to say indirectly in every concall that no nbfc will survive except piramal but recent update suggest exactly opposite…

It is still early to say how things would affect PNB Housing. While I think PNB Housing is not unethical like other players, it still has may problems that other NBFCs face such as increasing interest rates, high exposure to developer loans and increasing NPAs. Canfin Homes would be a much safer options where the NPAs actually is declining and they have just 1% exposure to developers.

Biggest overhang for pnbhousing is stake sale: Promoters want to sell for quite a while now and at top of it even management wants to sell to raise capital for growth. Lot of supply doesn’t go well for stock price in near term.

For Housing finance companies like PNB and Canfin, the problem is far different than being ethical or even potential NPA’s.

PNB Housing trying to reduce developer loans, LAP and all non-retail loans. When their cost of borrowing is 8.2% how are they supposed to make anything with retails loan of 8.6-8.7%? It’s the non-retail loans that has made it sustainable so far. Reduce it and you loose position to be in business.

Canfin homes situation is even worse. Their cost of funds will be even higher than PNB housing. Unless they underwrite successful LAP, how are they supposed to survive?

After last September, liquidity, availability of funds and cost of funds are major issues for these HFC’s along with much discussed ALM position.

HDFC and LIC Housing are far less impacted due to their name and implicit trust it wins them. My take after this crisis is done, only large and niche players will remain. Rest will be reduced or vanish. DHFL will be out of business and IBHF won’t be a major player if things go like they are right now. Let’s watch what happens to PNB Housing and Canfin.

Canfin has better yield and cost of funds…the below pic from latest investor presentation. Also, they intend to raise upto 1000 crores, which, if done, will further bring down the cost.

Canfin is not into LAP and other non-retail loans like PNBHFL. Instead they are focusing on non salaried segment of the retail loans to increase the yield. This led to some increase in NPA in past couple of years but looks to be coming under control. Btw, when I said increase in NPA, that was still much less than 1%