Hi Ranjan_r …Please explain what scam has come out of Piramal Enterprise.?

As per q4fy19 presentation, Canfin cost of fund is 7.9% which is less than 8.2%. You mentioned PNB housing finance cost of fund is 8.2% and also mentioned that Canfin cost of funds will be even higher than PNB housing. How can both be true simultaneously?

On page 17 of Canfin Homes, company has disclosed that their mortgage loan or flexi lap which I am assuming is LAP for salaried and professional is 369cr and for non-salaried is 439crore. Total about 808 crore. Their total loan book according to same slide is 15,743 crore which is 5% of book. Also their NIM of same period is 3.14%. I could not understand why do you say - Unless they underwrite successful LAP, how are they supposed to survive?

My bad on Canfin cost of funds. I didn’t check before writing. It’s indeed 7.9%.

Why I am stating the trouble for HFC’s in general is that plain vanilla salaried loans rate is 8.6-8.7%. The borrower here has credit history and can shop for better deal. So there is very less spread in this segment. You have to make up your spread in other categories. And loans like LAP or non-salaried have proven to carry more risk. Look at NPA’s of Aspire and Repco and others who ventured in affordable housing.

Nothing against Canfin specifically but this is situation for all HFC’s. And look what market has done to valuations of these companies.

Hi Nikhil, HFCs like Canfin don’t target the customer base that is eligible for 8.6% ROI. This is the primary segment for banks, and big HFCs like HDFC & LICHFL. I am not very sure about PNBHFL primary retail customer base but that of Canfin primarily is those who are not eligible for 8.6% type of ROI and hence Canfin lends to them at higher rates and thereby their yield is also higher, which helps in profits.

PNB Housing target customer is same as other major players.

One question if you or anyone else can answer. Who is this customer who is not eligible for 8.6% home loan? I can understand self employed and low ticket customers that Gruh and Repco targets at 11-12% rates. But who are these guys who are in middle and take home loans at 10%? What’s their profile?

One guess from my side would be normal salaried guys / self employed (doctors/lawyers/CA) but the houses bought will not be metro A grade but in 20-40L range. I myself had availed home loan from GIC at 10.5 when going rate was 9.5 since house I bought was built in old times with collector approvals but no new municipal corporation regulations.

PNB Housing Finance raises $100 million (~ INR 690 Crore)

from IFC to finance purchase of affordable housing projects

The fully-hedged facility has come at a landed cost that is much lower than the domestic pricing

for similar tenures.

5e782461-e092-4c4b-93dc-523aad318596.pdf (386.8 KB)

Financial performance (Q1 FY19-20 vs Q1 FY18-19)

Net Interest Income registered a growth of 45% to INR 625.5 crore from INR 432.8 crore.

Profit after Tax grew by 11% to INR 284.5 crore from INR 255.8 crore.

The Spread on loans for Q1 FY19-20 stood at 2.53% compared to 2.11% for Q1 FY18-19. The Spread based on IGAAP i.e. excluding the income on derecognized (assigned) loans and other Ind AS adjustment is 2.01 % for Q1 FY19-20.

Net Interest Margin for Q1 FY19-20 stood at 3.14% compared to 2.74% for Q1 FY18-19.

Gross Margin, net of acquisition cost but including fees, for Q1 FY19-20 stood at 3.44% compared to 3.21% for Q1 FY18-19.

The cumulative ECL provision as on 30th June, 2019 is INR 598.0 crore. In addition to the ECL provision, the Company has INR 156.5 crore as a steady state provision for unforeseeable macroeconomic factors. The total provision to Asset stands at 0.99% as on 30th June, 2019 compared to 0.74% as on 30th June, 2018.

Return on Asset is at 1.37% on an average gearing of 9.4x against 1.54% on an average gearing of 8.7x during Q1 FY18-19 resulting in a Return on Equity of 14.8% for Q1 FY19-20 vis a vis 15.8% for Q1 FY18-19.

Business Operations

Disbursements stood at INR 7,634.3 crore during Q1 FY19-20 compared to INR 9,767.3 crore in Q1 FY18-19 with 92% disbursement in retail segment. Retail disbursement grew by 7% from INR 6,595.2 crore in Q1 FY18-19 to INR 7,029.8 crore during Q1 FY19-20. Corporate disbursement degrew by 81% from INR 3,172.0 crore in Q1 FY18-19 to INR 604.5 crore during Q1 FY19-20.

Asset under Management (AUM) is at INR 88,332.9 crore as on 30th June, 2019 moved from INR 68,577.5 crore as on 30th June, 2018 registering a growth of 29% during the period with share of Housing Loans being 72% and Non Housing being 28% of the AUM.

Loan Asset grew by 19% YoY to INR 75,933.0 crore as on 30th June, 2019 from INR 63,905.8 crore as on 30th June 2018.

Borrowings

Total borrowings are at INR 72,261.4 crore as on 30th June, 2019 expanded from INR 60,439.7 crore as on 30th June, 2018 registering a growth of 20% during the period.

The Deposit portfolio grew by 32% to INR 15,445.5 crore as on 30th June, 2019 from INR 11,723.7 crore as on 30th June, 2018 with expanding retail penetration.

Total outstanding loans assigned amounts to INR 12,399.8 crore as on 30th June, 2019.

Asset Quality

Gross Non-Performing Assets (NPA) stood at 0.85% of the Loan Assets as on 30th June, 2019 against 0.43% as on 30th June, 2018. At an AUM level the Gross NPA is at 0.76%.

Net NPA stood at 0.67% of the Loan Assets as on 30th June, 2019 against 0.33% as on 30th June, 2018.

Capital to Risk Asset Ratio (CRAR)

The Company’s CRAR based on IGAAP stood at 15.13% as on 30th June, 2019, of which Tier I capital was 12.04% and Tier II capital was 3.09% compared to 13.98% with Tier I at 11.00% and Tier II at 2.98% as on 31st March 2019

3 Likes

Results review

1 Like

There is no smoke without fire … yet management came up with below clarifications

This is with reference to your email no. L/SURV/ONL/RV/PA/(2019-2020)/99 dated September 16, 2019 seeking clarification on recent news item which appeared in “www.livemint.com" dated September 15, 2019 captioned “Goldman Sachs, PremjiInvest and Munjal look to invest in PNB Housing Finance” In this regard, please find below our pointwise reply as under:

a. Whether such negotiations were taking place? If so, you are advised to provide the said information along with the sequence of events in chronological order from the start of negotiations till date.

We would like to apprise you that the Company is in the process of raising Tier I capital as approved by its Board on July 30, 2019, which was informed to the Stock Exchanges. However, on the above mentioned news, we would like to state that currently no such negotiations are taking place. The Company is aware about the provisions of Regulation 30 the SEBI (LODR) Regulations, 2015 and duly comply with the same. We will intimate to the stock exchanges of all the material information and events as and when they occur.

b. Whether you/ company are aware of any information that has not been announced to the Exchanges which could explain the aforesaid movement in the trading? If so, you are advised to provide the said information and the reasons for not disclosing the same to the Exchange earlier as required under regulation 30 of the SEBI (LODR) Regulations, 2015.

We would like to state that the Company or its officials are not aware of any such information, which could explain the upward movement in the stock price/ trading.

Company is getting queries with respect to the impact of tax change on the Company. To

give a perspective for FY18-19, PNB Housing effective tax rate on a consolidated basis was

31.30%. Considering the tax reduction as per the announcement, the expected reduction in

the effective tax rate for PNB Housing can be anywhere between 8%-9%.

21215e54-1746-448f-8e7b-b35d2bab9907.pdf (182.1 KB)

2 Likes

Please someone explain why suniel mehta has resigned from chairmanship of pnb housing,will he be going to be reappointed or he has permanently resigned?

As Mr.Sunil Mehta completed his tenure as MD and CEO of PNB on 30 Sept…

as per bse announcement.

1 Like

Again a desperate attempt (they were ONLY company coming out with calculated impact of tax reduction on 20th Sept,2019) to arrest the downfall… declaring numbers of Q2 well before scheduled release of result

All these actions have failed to provide any respite. Although the sector itself is getting badly hit but the sharp decline hints something more fishy… we have to wait for getting the exact reasons

0e58b6fc-3578-427e-ab06-62daf759c0ba.pdf (491.7 KB)

1 Like

Currently the challenges seem more of sentiments rather than actual deterioration of financials. In many cases the target companies remain in denial mode until a breaking point is reached.

Thus some companies are available at cheap valuations.

1 Like

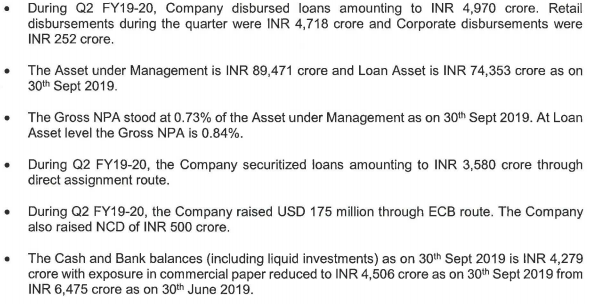

What is the meaning of 4th point,please somebody explain,what is the meaning of securitized loans?

hope this helps

1 Like

What happens to Loan book of NBFC post securitizataion ? Will the Loan book size reduce proportionately in the NBFC books post selling these loans through PTC and direct assignment ?

The securitized assets move off balance sheet and thereby improve the leverage ratios.