Is the fall justified or market knows something that we ( though we too part of market ) don’t know ?

Is the sharp free fall giving opportunity to accumulate it for 3-5-7 years investment horizon ?

When are the plan to announce result ?

Is the fall justified or market knows something that we ( though we too part of market ) don’t know ?

Is the sharp free fall giving opportunity to accumulate it for 3-5-7 years investment horizon ?

When are the plan to announce result ?

Results and Dividends are on 9th May.

A lot of perceptions start emerging with the fall in Stock Prices. Current fall is not new and we had seen similar fall in October when it fell to 700 levels and eventually rose to 1000 in a Month. Current fall before the results for whatever reasons was more fueled by PNB Stake sale pressure and Credit Rating on Watch by CARE (Interesting that Credit Rating came after fall in Prices from 1000 to 800).

There may be some doubts on the quality of the Book and when the Book itself is doubtful , P/B becomes less important for considering valuations for the financial business.

Around 22% of Loan Book is to Construction Sector/ RE which is facing a slowdown. LAP accounts for around 20% of the loans which looks on a higher side. Their may be possibilities of default by the clients and thus high NPAs and low liquidity which market may be anticipating. Their ability to borrow funds to aid growth will be crucial factor to watch out for.

Its ability to control its funding cost , Maintaining NIMs and maintaining its asset quality will be critical.

As per the ratings , Gross NPA ratio are around 0.47% and Net NPA ratio are around 0.37% as on Dec 2018 which looks extremely Good (Though Share Prices indicate a very different picture). It is quite tough for me to understand the accounting by the HFCs. They have maintained sufficient provisions for the Gross NPAs but there may be lot of loans seasoning out and next 2-3 Quarters may present a better picture. They have declared NIL NPAs on the Corporate Real Estate Loan Book (Comprises 22% of the loans) which is quite strange and looks very aggressive accounting with high risks.

They are looking to raise capital on 9th May Board meet. Let us see how it goes from here.

For a 3-5 Year term, it looks good but need to wait for clarity and arrest in fall in prices. Buying 5-10% above these levels may be better than playing blind at current prices in my opinion. Also need to understand Loan Book which is very complex to understand. Regarding Management , Mr. Sanjaya Gupta has a rich experience and i have not come across any Negative News on him.

Disc: I have a Position around 840. Not averaging !

They are taking the ECB route to raise money instead of domestic market. What are the implications of this? Would this expose them to exchange rate risk?

Key monitorables -

For a 3 year view, next 4 quarters are crucial a the picture will emerge. Stock is hitting 52 week lows, indicating anticipated problems.

disc- invested at higher levels. holding for now.

HFC need to mandatorily hedge with FCY and interest rate risk in case of ECB or equivalent borrowing.

The need to borrow through ECB route could be:

Financial performance (Q4 FY18-19 vs Q4 FY17-18)

Net Interest Income registered a growth of 13% to INR 609.7 crore from INR 540.8 crore.

Profit after Tax grew by 51% to INR 379.7 crore from INR 251.6 crore.

The Spread on loans for Q4 FY18-19 stood at 2.59% compared to 2.98% for Q4 FY17-18.

Net Interest Margin for Q4 FY18-19 stood at 3.18% compared to 3.59% for Q4 FY17-18.

Gross Margin, net of acquisition cost but including fees, for Q4 FY18-19 stood at 3.51% compared

to 3.78% for Q4 FY17-18.

Financial performance (FY18-19 vs FY17-18)

Net Interest Income at INR 2,063.5 crore vs INR 1,659.9 crore registering a growth of 24%.

Profit after Tax grew by 42% to INR 1,191.5 crore from INR 841.2 crore.

The Spread on loans for FY18-19 stood at 2.35% compared to 2.54% for FY17-18.

Net Interest Margin for FY18-19 stood at 2.93% compared to 3.19% for FY17-18.

Gross Margin, net of acquisition cost but including fees, for FY18-19 stood at 3.34% compared to

3.50% for FY17-18.

The net worth as on 31 st March, 2019 stood at INR 7,543.9 crore.

The cumulative ECL provision as on 31st March, 2019 is INR 437.6 crore. In addition to the ECL

provision, the Company has INR 156.5 crore as a steady state provision for unforeseeable macroeconomic factors.

Return on Asset is at 1.61% on an average gearing of 9.3x against 1.56% on an average gearing

of 7.6x during FY17-18 resulting in an expansion of Return on Equity to 17.44% for FY18-19 vis a

vis 14.20% for FY17-18.

The Gross NPA, as on March 31, 2019, of the Company is 0.48% as against 0.33% as on March 31, 2018. Net NPAs of the Company is 0.38% of the loan assets as on March 31 , 2019, against 0.23% of the loan assets as on March 31, 2018.

Did anyone attend the concall? Any updates on the liquidity profile of the company and management guidance.

Listened to the concall on the research bytes app. It was extremely long, with the operator, forced to reduce the questions to two and then one. Even the famous investor Bharat Shah, who can smell money from any distance, was present for the con call asking his smart questions, and was allowed only one question. In the next few weeks the company will finalise it’s capital raising plans and go slow on real estate lending, this market expected to normalise only in October. EPS growth for the year is around 42%. The question is how long a 30% growing company will continue to sell so cheap, and when the general public will join the Sanjaya Gupta bandwagon.

The real question here is how long will 30% growth continue? Looking at single digit disbursement growth in FY19 and spiked up gearing ratio, it won’t be long. They will start growing at 15-20% till they are able to raise equity capital.

Results look good on face of it. A few negative points which I observed

Their yield is up by 8 bps while cost of borrowings has shot up by 47 bps. Clearly pointing to stress in borrowing after ILFS crisis. The spread has reduced by 39 bps.

Their average cost of borrowing is now 8.06%. At that rate, A retail home loan of 8.6-8.7% won’t be profitable at all. Meaning they have to resort to higher risk LAP, construction and developer finance which they already have and market is worried about.

ALM mismatch for assets greater than 5 years is 10,000 cr.

As I mentioned above, their gearing has shot up to 9.3. Which means they have to raise equity capital soon or slow down growth. Else they will face rating downgrade on just this basis.

They are showing NPA of 0.48%. With the loan book they have, even if market’s worries are materialized by half, this NPA will go up a lot.

The stock is cheap at PE of 11 and PB of 1.6. My feel is they have no choice but to slow down growth to 15-20%, focus on reducing LAP, construction finance etc. and focus on not letting existing book slip into NPA. And of course manage liabilities which they are trying their best to do.

Raising equity capital at PB of 1.5 is not great for shareholders. It’s only good when raised at PB of 3X and 4X.

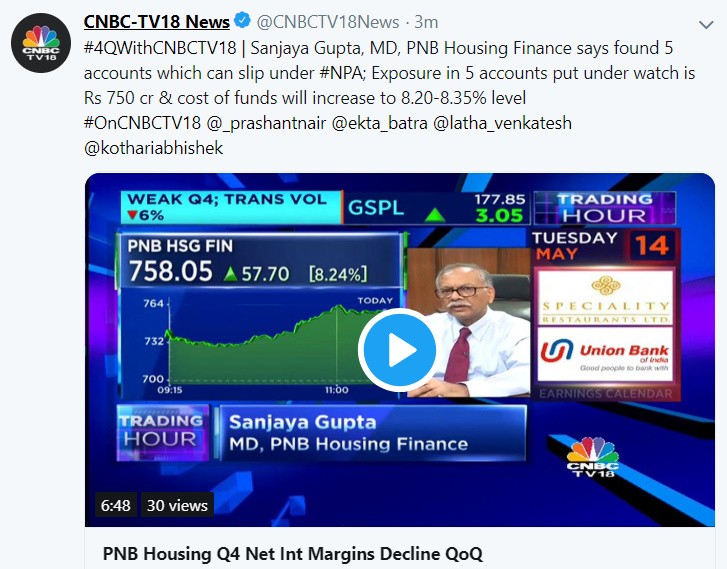

I am not sure if they will grow at 30% moving forward due to potential NPA issues…Rs.750 crores under watch…

Today’s research report from Motilal expects a spike in NPA as compared to their own report based Q3. Guess something’s gone wrong as otherwise why would there be such a huge difference in estimates within 3 months…

Jan 2019:

May 2019:

Sanjay Gupta’s statement that they have disbursed all the loans based on the construction stage is a complete lie. They have disbursed entire loan amount to me for Mantri Webcity, Bangalore project without a single brick being laid on the ground. Still construction has been completed for 5-6 floors (out of 20 floor) and developer has stopped the construction. They are many buyers who have been duped by the developer and on PNB housing part they have not followed the NHB guidelines of disbursing loans based on the stage of the construction.

Is he talking about builder or retail loans? Yours is a retail loan

It was for retail loans. He was answering to a question around a PIL filed against PNBHFL on illegal lending.

They are not alone , Axis bank has done the same for many builders like shobha and prestige. There is a money aspect, if things go well, and projects get completed but delayed by 1-2 years , the bank makes windfall gains on the interest due to early disbursement compared to construction. None of the 1000-2000 plus units apartment projects are getting completed on time.

Main concern raised in this interview is builder loans, if you see the results presentation they have 2-3 times collateral against these loans, 30 days past dues on construction book has come down compared to last year

This is bad for the consumer and good for the company.

Due to early disbursement, pnb will get good interest income.

This is bad for the end customer. That’s how many big businesses do things globally.

Hdfc bank levies unauthorized charges on many accounts. Many complained, still it continues to grow.

Similarly, maruti sells pretty poor quality cars (with respect to safety aspect) in India.

At the end of the day, there will be negligible defaults from the customer… Both mantri and pnb know… And even if someone defaults, pnb will get the flat which will be 1.3 times the value of the loan at the least.

So, it is the customer who loses, not the company.

This was done under a Buy back scheme , where developer promised to pay pre EMI for 3 years. After that there was an option to exit the project with some incentive. Now developer is neither paying the EMI nor allowing to exit. Poor customers are in a very bad shape as they never planned their cash flow for a scenario where developer will not pay. So , many have already defaulted and others are on the verge of default. So, saying that it will not impact PNB housing may not be correct. It is going to hit them at some point of time. Since apartment construction is nowhere near the completion, PNB Housing can not sell it and recover the amount. Majority of the loans have been provided by PNB Housing for this project. Other lenders like Axis Bank and IndiaBulls have also given loans to some flats.

I am not understanding reason behind this statement. Kindly educate me Sir.