Only way to price real estate for an investor is Rental yield + Expected Price appreciation = Home loan interest rate. In most developed countries appreciation is minimal so Rental yields are closer to home loan rates. But in India historically low Rental yield (2-3%) was compensated well by high price appreciation (7-8%). In the future though I see absolutely zero scope of 7-8% price appreciation in India, given real estate in big cities like Mumbai is already priced at par with say New York and other big developed cities. But some how, real estate market expectations in India are still stuck in the past, but at some point it is bound to change

2 Likes

The best way for Real estate to correct is time wise correction . If it corrects price wise - since most of Indian population Networth is tied in real estate - they will be affected by decreasing wealth effect – this impacts consumption and finally economy in big way … No political party will like to risk this …

Add to that lot of political money is tied in real estate . They will not allow price to go down by level . Look at amount of resistance to repealing Rent control Act in Mumbai … or RERA in Kolkatta … or diluted RERA in karnataka …

All said in election years Politicians need money which earlier chunk used to come from developers for regionals and other parties ( other than BJP who has diversified resources ) . RERA , black money + NBFC money control is effective tool for them to stop developers from giving cash to political parties …

I see NBFC money squeeze till May 2019 … Remember in Kolkatta just before state election one of the biggest chit fund was busted - I see few busts of NBFC affiliated to political parties in this period too …

1 Like

Well, I agree here. Some price correction has happened across NCR markets and in luxury segment in other cities but there is not much correction in properties up to 70 - 80 lakh rupees in tier 1 cities. Even today in markets like Bangalore / Pune branded properties from quality names up to 80 lakhs gets sold very fast in good locations (Whitefield, Sarjapura, Kharadi (Pune), Hinjewadi (Pune), etc.

We are in the business of supplying materials to construction projects and surprisingly in 2018 we have had the best order booking from builder segment. Not sure if this is sustainable but one of the reason why we are getting orders is because almost all builders are improving the quality of their products to differentiate themselves from other builders. Real estate is now a buyer’s market and consumer is spoilt for choices. We being in the higher quality segment are getting benefited from this trend. Along with credit crisis + Rera, this changing consumer profile will ensure that top and quality conscience builders will further strengthen their grip on the market. Market consolidation will happen for good. Sooner rather than later.

5 Likes

One sincere and humble request to all fellow VPers:

Let us keep the disucssion focused to company specific instead of discussing generic things which are mostly our subjective opinions and add very little value to the other fellow members. Even though PEL does lending to real estate sector, disucssing about the rental yields, housing market and pricing scenario or comparison with RE sector in other countries may be tangential and veer us off from the objective for the thread i.e.: to analyze and understand the business better including risks and opportunities around the business. It is perfectly ok to allude to real estate scenario if it is required in the context of the discussion around PEL’s business. However, generic industry discussions around the industry can be taken up on more appropriate threads (may be dedicated to real estate industry dynamics). This way, we can declutter the thread and help other members who visit the specific threads to know more about business dynamics deal with more relevant information. I hope everybody takes this in right spirit

28 Likes

@desaidhwanil - How different is it from discussing cotton prices in a textile business, or steel prices in a pipe business or milk prices in a cheese business? We very much discuss supply/demand dynamics, govt policy/regulations in those sectors, international prices of said commodities, ability of businesses to withstand RM fluctuations, taking inventory write-downs due to underlying commodity price fluctuations and in case of gold-loan businesses, the impact of gold prices and LTV on business prospects and so on. Why is discussing rental yields and possibility of RE asset price fluctuations affecting HFC loan books different?

Thing is even I felt it was perhaps off-topic when I posted the comment on rental yields but when I reflected on it, I realised that it may not be. Taking it very much in the right spirit but wanted to express my stand. Please feel free to remove the chain of comments on rental yields if you find it off-topic.

8 Likes

I appreciate your view point. My personal view is that it is ok to discuss some of these factors in the context of the discussion around PEL’s book/assets and how these factors might impact it. However, general discussions around only industry and real estate scenario takes away lot of space and makes the thread difficult to scan through from PEL’s business perspective. I almost got lost in the web of opinions/beliefs (without much of supporting data/clear analysis) on generics while going through the thread and hence thought of pointing out. Rest, I leave it to the best judgement of everyone.

22 Likes

this is not new and they have been doing this for a while…what’s the issue with it now…more insights maybe in tomm earnings con call…but when you have robust risk management…what’s there to be worry of…i think the yield they are generating in close to 13 to 15% on this ILFS fiasco has made all nbfc look so mean and vulnerable…40% fall in a month is nerve racking to many…also we must note that major chunk is with FLL’s who are on a selling spree

Piramal is redeeming the NCDS early even when the market is hit with liquidity issues. Wondering what could be the reason for this?

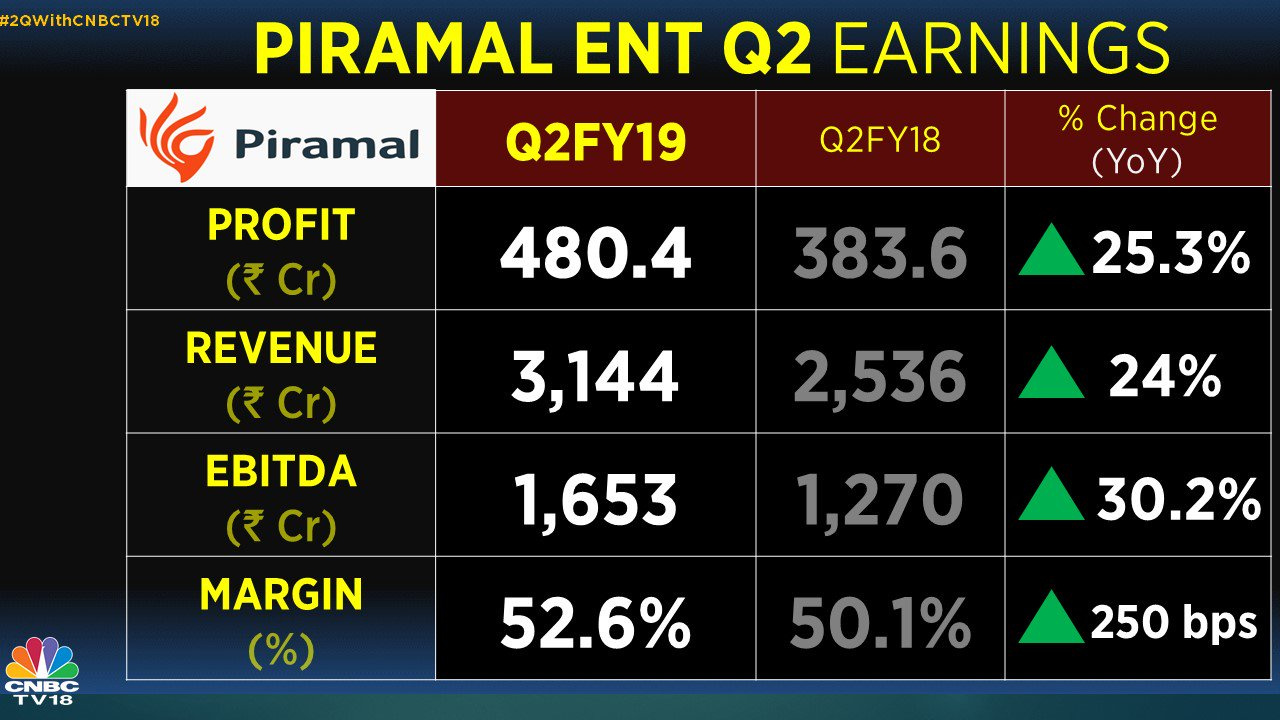

Investor presentation

Profit 26% does not include non-recurring and non-cash accounting charge towards Imaging assets in Q1 FY2019.

On Liquidity front -> Robust liquidity position, with more than INR 7,500 Cr in the form of cash and several unutilized bank lines

Loan Book Size -> Total Loan Book grew by 59% to INR 52,793 Crores as on 30 September 2018. ’

NPA - > Gross NPA ratio (based on 90 dpd) was at 0.5%, total provisioning at 1.74%

Key words - > Tightening of Liquidy, Risk Management, Company able to get sufficient liquidity even in the current volatile environment, Added Strength to Board of Directors by appointing Former SBI Chairman, Largest effective promoter shareholding among major non-banking financial institutions of India, around 51% Skin in the game.

Interest expenses for Q2 FY2019 were higher primarily on account of the increase in borrowings for growing the lending business.

Pharma Revenue - Flat 2.5% growth

Financial Services - Strong - 46.7%

Healthcare Insight and Analytics - Good -14.1%

Particulars H1 FY2019

Total Loan Book size Rs. 52,793 Crores

Total Equity on Lending Rs. 9,864 Crores

Average Yield on Loans 13.7%

Average Cost of Borrowings 8.6%

Net Interest Margin 6.9%

Cost to Income Ratio 17.7%

Gross NPA ratio (based on 90 dpd) 0.5%

Total Provisioning 1.74%

ROA 3.4%

ROA (considering Cash Tax and other synergies from merger) 4.0%

ROE 17%

ROE (considering Cash Tax and other synergies from merger) 19.6%

On ALM Management

Robust liquidity of >INR 7,500 Cr in the form of cash and several unutilized bank lines

• Additional bank lines of INR 2,200 Cr sanctioned since the last week of Sep-2018

• Additional measures / proposals to boost liquidity:

− Issuance of non-convertible debentures (NCDs)

− Raise external commercial borrowing (ECB)

− An Euro medium-term note (EMTN) programme

− Expect to secure additional bank lines of Rs 7,000 Cr

ROE of 25%+ prior to fund raise. ROE calculation for PEL on a cash tax basis, considering the capital allocation from the fund raise.

100% secured lending with unique ability to takeover, complete and sell a project, if needed.

80% of projects are in the construction stage or completed

Completed project can be sold through Brickex, the in-house broking and distribution arm, if required

The Group can take over, complete and sell a project (in a worst-case scenario).

Independent risk and legal teams, reporting to the Board

100% deals with conservative underwriting assumptions based on delay in sales velocity by 6-12 months

Borrowing costs increased only marginally, despite the recent increase in volatility and rising interest rates

Overall lot of coverage on Financial services than other segments.

Key commentary from Mr Ajay Piramal

- “My view is that because of the high valuations that Financial Services companies are getting, people are indulging in reckless lending… it’s high time that we start distinguishing between the good players and the not so good players in the space.”

- “….my concern comes that if there is a blow up in the space and it is bound to happen, let me give you this as a prediction, it will affect the entire industry…”

- “…availability of capital to the financial services sector is the No. #1 risk.”

13 Likes

My jot downs from today’s concall. I must say one of the best concall I have ever attended in terms of clear answers provided by any company management.

- Banks and Mutual funds becoming selective.

- Best in Class definition – low leverage, high promoter %, good equity – PEL is one of them

- Only 3 amongst 30 NBFC received additional bank funding in Oct

- Sufficient liquidity – 7500 cr as on 30th Sept,

- 2200 cr addl bank lines on 30th Sept, additional 7000 cr bank lines planned

- Further steps are being under taken, like ECB this quarter, Dollar bonds Roadshow in Jan 19

- PEL - Largest promoter shareholding in financial services business in India

- PEL - Lowest leverage NBFC in India

- Top 10 developers form 42% of PEL’s portfolio

- RBI comments – best processes in NBFC, NHB audit expected to provide similar comments

- Lodha – 4300 Cr exposure – 6 deals over several projects

- 90% of the 1 yr pre payments – paid for Oct 19

- Lodha – since IPO got delayed – working on plan B – sale of non strategic assets worth 4500 Cr,

Private equity deals worth 1000 Cr - 1700 Cr – 2 projects in Omkar – fulfilled its obligations – L&T realty and Piramal Realty – part of top 5-6 projects in Mumbai

- 1200 Cr – 1973 – receivables funding – Jun 19 onwards – fully prepaid against 1973

- Vatika – 1393 Cr outstanding – 45% against working hotel cash flow in Gurgaon, rest against 3 projects – 2 residential project, 1 got delayed by 1 year, cross collatarisation helped getting interest paid

- NIMs would improve, best in class

- Cross collatarisation in rest 30%, RERA mandates 70% in escrow

- Consolidation

- No growth targets, focus on risk containment, liquidity maintained, roe above 20%,

- All drawn banks – enough liquidity- flight to quality

- Refinancing? – 70% of the book in construction finance, we take over project and complete and sell it, PEL does not depend on refinancing

- SME sector 31% of GDP, 26% of the employment, it is funded by NBFCs

- Only 10% of the developers will survive, nbfc consolidation will happen. Will separate Men from Boys

- Opportunities have doubled for good companies

- No change in approach to lending from PEL

- Thanks to HFC, now long term sources of funds, $250M ECB loans this quarter, Jan 19 – roadshow for US bonds, constantly looking for diversification of liability sources, decided long back.

- ROE for pharma and healthcare analytics would be lower – 15% ROE as threshold as target

- Consumer pharma - OTC- sales growth would come from this year,

- Next 2 years Real estate financing share will come down to 50% from current 74%, due to higher growth in Corporate Finance, housing finance, ECL etc

- All agreements are bankruptcy proof, 100% SPV, Lien on land and building,

- Interest rate increase of .5% passed on, competitors who were undercutting earlier have now raised rates by 2%, PEL customers appreciate that PEL is not using this opportunity to raise rates much higher

- Others sources of funding – ICD, non bank etc, no loans from Piramal group company

- Bain – JV – India resurgence fund - $100M each, may announce new deal

- Lot of investors are interested (NBFC and Banks) in lending to PEL- perpetual providers of funds – family office, pension funds

- Change in foreign exchange – goodwill 800 Cr

- 8.6% - cost of funds for Q2

- Funds raised 1500 Cr after 30th September

- Cost of funds Increased by 20 basis points in Oct

Sorry for less details as I have typed this out while call was on. Others who have attended the call can add more details.

36 Likes

I am amazed by PEL confidence … But going through concall notes - I personally am scared of being PEL customer.

I am surprised why some large real estate developers are signing " Head PEL win & Tail You lose " contracts with PEL . This means these developers are in stress or have some issues .

Asian paints / HUL etc do have similar one sided contracts with distributors , but they try not to speak about it – rather they downplay their strength …

Indian Buffett should not boast off . He should keep quiet and let his action prove that market is wrong . For him share price is irrelevant , and even then if does fall below its intrinsic value he should buy back

PEL has all ingredients of being survivor in this cycle , he should keep low profile and let other NBFC fail so that he can gain MKS and be stronger post this cycle …

But that is not happening … Since August 2018 … I am surprised by piramal aggressive promotion of his company …

10 Likes

You are speaking as you have some insider information of line of credit being offered to Piramal from Reliance. This sounds little off to me.

Promoting your own company, even if it sounds aggressive to some is welcome. Lot of time we here that Indian promoters do not market their companies well to attract investment. IMHO PEL is on good trajectory. We could see some issues with RE developers below Grade A for funding and that would help PEL to improve their NIMs further. Too much pessimism has come to this counter now.

2 Likes

Hopefully it may never come to that and Shailesh could have put it a more sophisticated way, but there is some logic to his statement. One does not need insider information. Ample examples are readily available, including recent package given to younger brother. Holds true for many other business groups, so in that sense is fairly common.

I agree with Piramal promoting company. Even Bajaj finance did the same ( though both companies results will speak by them self) .The times are different and the share fell from around 3000 to around 1900 . If company believes crisis is temporary he needs to give confidence to share holders and not flush them away.

when piramal said that only top 10 builders will be left going forward and he says all is well with the big developers…then why lodha is selling their assets…does it not mean they are in distress too?

I see nothing wrong in AP strongly promoting his company as being the largest shareholder, he has “skin in the game” . He has suffered the most (financially) in last 45 days without any of his fault. I am sure all of us would have done the same (or may be more) if we would have been in his position…

Piramal has steller performance record of shareholder returns for last 26 years and being a contra player, I am sure he would be looking for gaining market share. Since PEL business model is much different than normal lenders (PEL team first understand the business before deciding whom to lend), he has to do the job of explaining the same to the investor/analyst community.

Disclosure : PEL is my largest holding so my views could be biased.

4 Likes

Huh! forget about Lodha … one of my friend called up Piramal to enquire about one of their projects. He didn’t go ahead but now for the last 3 months every alternate day gets desperate call from Piramal about offers at different projects of theirs. Does Piramal provide booking data under their own management like we get from Godrej etc?

BTW, I find this self glorification little too much. Smart folks let numbers do the talking and keep their sermons limited.

1 Like

Piramal Realty is not part of listed company so its not correct to expect them to share details about their privately held company.

1 Like