This is interesting & Important piece of information … Does PEL own stake in Piramal Realty . Now if PEL takes over project by booking loss and transfer the property to Piramal Realty … Has he shared how that will be done … Any links …

Piramal Reality is a seperate entiry managed by Anand Piramal. Its in no way related to PEL . Piramal Realty is funded by Goldman

We are discussing the merits/risks and business of piramal enterprises. Please dont bring in the ambanis name into this conversation without any definite reason.

Such flippant and useless posts are not welcome and everyone needs to take note and ease the jobs of moderators.

These kind of posts dont add any value.

16 Likes

I wasn’t aware of this fact. There is another brand Address Makers for Bengaluru city which uses Piramal name.

Then through which entity PEL intents to takeover projects and develop it … ??

@hitesh2710 : The whole idea of any discussion is what are safety valves for any business . I am surprised why this is not allowed . Any way pl delete any thing which you feel does not add value to group as you are veteran and understand the forum better than me …

Its happening with all the developers.Once you show interest in any projects, the Developers chased the prospective buyers with frequent phone calls and messages. This is practised by all the builders including Godrej and Kanakias. Why just builder, just go to a big jwellery showroom, ask for any jwellery and come out without buying it.Yhe jweller also will chase you the same way the Developer do. Its a new normal for business.

1 Like

check kolte patil and oberai reality results

they have decent growth , I feel worst is over for good developers (delivery on time , quality build ,customer satisfaction, location etc., ) .

Interview with Mohnish Pabrai on CNBC , he had the same view on real estate because of GST , RERA, DEMON — 80 to 90 % will be gone or on life support .

I heard Parbai interview…

How does this impact PEL - Has industry structure changed for worse

-

If Developers consolidate - that means there is customer consolidation is happening - I believe that is bad for financer as it has to compete for lesser customers

-

Big brand name customers who have transparent & compliant or even builders like Kolte patil have taken finance from global financial institution like blackrock , IFC etc … These are often at much better terms than what local NBFC offers esp IFC which is development organisation – More global finance organisation to offer finance @ better financial terms means more competition intensity

-

Suppliers of Credit has reduced - With Debt mutual funds losing clout and banks being major supplier of credit the supplier ( bank ) bargaining power has increased … Again this is negative for Local NBFC lending to real estate

Two things we kept hearing since last year. 1) Unorganized builders will vanish due to RERA. 2) Unorganized businesses (not specific to RE) will vanish due to GST. Stock price also kept going up. And we developed conviction in the theory.

I dont know how 1) is playing out. But for 2), this is what I hear in various con calls. a) Before GST implemented, they said unorganized players would suffer. b) After GST implemented, they told its too early to say if it has any impact. c) Now they are saying, unorganized players are getting organized.

3 Likes

Regulation makes industries mature … History indicates when industries matures - RULE of Three becomes valid …

This happens across the world - across industries . But will it happen tomo – No it takes long time typically one to two decades … post market sees the trend …

In the conference call held day before, there was one question asked by Ravi Mehta of Deep Financial, which went surprisingly unanswered ('ask us offline" was the sort of response). It was the only other question on financial statements.

I wanted to ask that question here to see if I can get an answer:

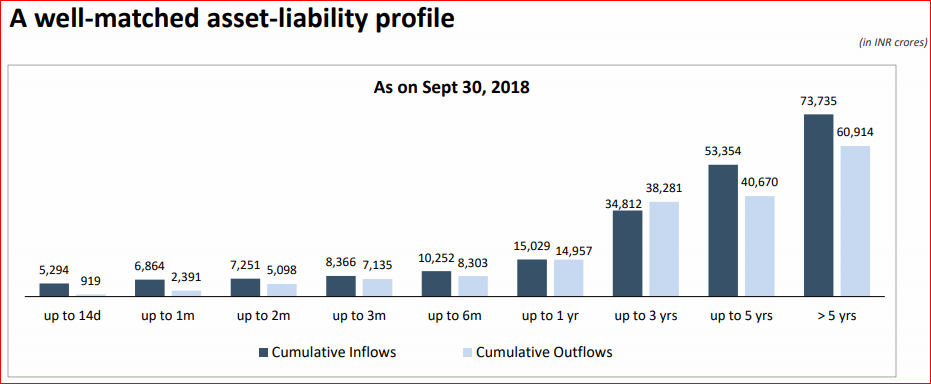

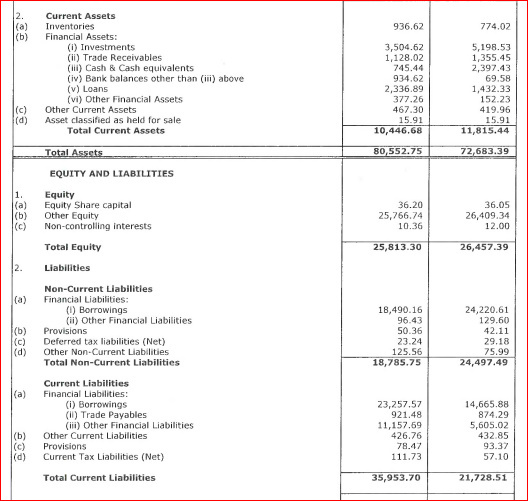

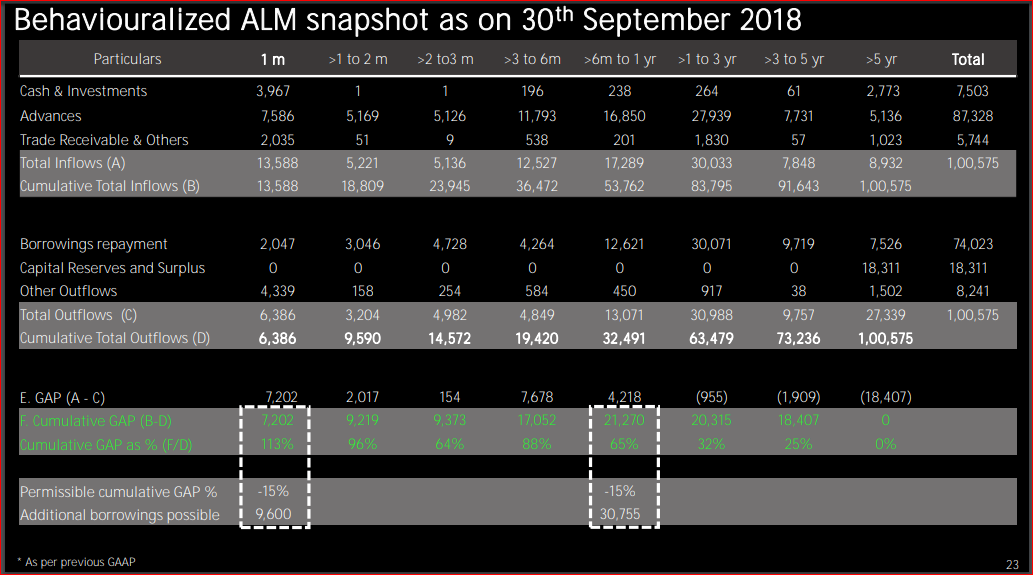

On slide 30 of the presentation that shows the ALM buckets, cumulative outflows upto one year is Rs 14,957 cr as on 30 Sept. The financial liabilities as of 30 Sept in the consolidated financial statement was ~ Rs 34,300 crores (Current Borrowings + Other Financial Liabilities, the latter is mostly fully current maturities of long term debt as per AR 18). Most of this pertains to Financial Services business as can be seen from the capital employed.

How does one explain this? The former in fact should have also an interest component too - how can it be less than half of what is stated in the accounts?

The same also goes for the 14 day bucket (Ravi did not ask this, but this was also surprising). 14 day inflows were estimated Rs 5,294 cr but their total current assets (which includes all segments) - to be realized over the operating cycle of a year was itself about 8,600 crores of which Cash was only Rs 1600 crores.

The relevant pages are attached here

Slide 30

Extracts from Statement of Consolidated Balance Sheet

Thank you!

9 Likes

This whole concept of movement from unorganised to organised was highly overrated from day 1 and propagated by excel experts who have limited connection with the ground reality. Many are small due to lack of ambition or fire in the belly and not because lack of ability. If they are forced, they will be organised, thrive and compete. Of course they will lose ground in the long run due to scale, disruption etc but only in the long run. Coming to real estate if the hypothesis is that only 10% will survive (which I don’t agree with) those remaining ones will become financially stronger eventually and why would they go to Piramal for extortionist rates of interest (~18-20%). I still wonder how these developers make money at these funding rates when capital values have not moved up but other raw material keep going up.

Disc: Is in my watchlist. evaluating but unconvinced

2 Likes

@diffsoft - Good catch. Are there guidelines on what is considered as Current liabilities? The reason I ask is that Cumulative Outflows upto 3 yrs seems to match the current financial liabilities in the HY BS. Maybe upto 3 years is considered Current? Just guessing. Even if this is the case, the Current Assets should reflect cumulative inflows for 3 years but it’s nowhere close.

For a layman like me, a simple subtraction of Current Liabilities and Current Assets between March '18 and Sept '18 shows all’s not alright here.

March '18 - 21728.51 - 11815.44 = 9913.07

Sept '18 - 35953.70 - 10446.68 = 25507.02

The difference of about 16000 Cr is made up of about 9000 Cr increase in short-term borrowings and 5500 Cr increase in other financial liabilities. The Current Assets have barely increased. Interestingly long-term debt has come down between March and Sept. Was this financed by the short-term debt? If that’s the case, isn’t this a Ponzi scheme?

2 Likes

Accounting Standards prescribe them quite well. Essentially any resources (mostly monetary) that would flow to settle established / accepted obligations.

The period current depends on the operating cycle the firm opts for, which is here 1 year (notes to accounts).

We need to accommodate for the fact there can be some quirks. For instance bank lines are always renewed annually and may be considered 1 year but in the minds of most management it is just a plain rollover with adjusted limits based on some computation and ratings.

Replacement of debt is not a Ponzi scheme (or rather it can be looked like a legalized Ponzi scheme in the fractional reserve system of banking that Austrian school hates - and I can see myself stepping out of my limited circle of competence :)))).

Dear All,

The interest rates 18 to 24% are typically considered benign in the unsecured & unorganized markets. In fact financial institutions can only lend to few entities and majority players look for short term funding , say one to three years. I think Piramal offers considerable flexibility & support to such Builders who also benefit from the discipline essential for structured funding. I feel Piramal will continue to do better than his peers due to the due diligence they do plus the understanding RE of micro markets within the metros…

I wish to remind and highlight that many people had doubts about Piramal getting the money fully from the Abbot deal eight years ago and the stock was available below cash due. Then,PEL yearly EBIDTA was around 400 cr, Eight years later we can look forward to a net profit of 2000 to 2500 cr ( with little change in equity ) and in the meantime PEL returned most by way of dividend and buy back.

In between he succeeded in many deals ( vodafone,DRG,financial foray etc) and lost in few ( Drug research, imaging. cargel etc).

AP was not seen much in public nor was he interviewed regularly in those times… However. AP took a considered decision some time after the Vodafone engagement and is seen being more vocal about his ideas. I feel, the present crisis in the industry will help AP to reassess and reorganise the companies stance towards risk…

To sum up, I feel PEL can continue to deliver better returns ( over long term ) to other instruments and the main reason for this is the firms superior capability to understand the pharma and RE industry dynamics.

Disc… invested since 2010.

1 Like

Good job @diffsoft. I too though the question deserved a public response. An ALM mismatch question at this point of time requires better scrutiny and a better response.

1 Like

Didn’t listen to the concall, but in the ALM slide, the “upto 1 year” figure doesn’t mean everything up to one year, but from 6 months to 1 year.

If you want EVERYTHING up to 1 year, you will have to add all the figures starting from “up to 14d” to “up to 1 year”, which comes to around 38k, which is approximately 34k (mentioned as current liabilities in the B/S) plus interest.

I think the premise that “past performance is the answer to all your doubts” is an invalid one to support the argument on future prospects.

The business is vastly different, and well…the man is different as well (as my partner pointed out - not much talk about failures, questionable transactions, an almost impenetrable financial statements in the annual report)

It seems to defy logic, English and how others present (say Bajaj Finance - here)

Bajaj Finance does the job of also relating it to financial statements.

1 Like

In that case, if you see the ALM for amounts greater than 5 years, its more than 70k crores for both inflows and outflows. Certainly something else has been factored in this because of which a reconciliation with the reported numbers does not look possible here.

1 Like