An insight into how piramal HR works https://m.timesofindia.com/business/india-business/annual-bonuses-in-bfsi-can-lead-to-short-term-thinking/articleshow/66252537.cms

Piramal has approx 22k crore listed as non current investments in balance sheet. That is almost a staggering 40%,any one scanned the annual report recently to see where this money is?

If you analyse the balance sheet of a share holder friendly management reputed for corporate governance, you will find a lot of hidden wealth. Hence the investments in PEL balance sheet should not be a surprise. On the contrary the balance sheet of a fraudulent management, will have a lot of cockroaches and hidden liabilities.

The return on equity of the real estate financing business of PEL is close to 20% as per management statement. However the ROE of the whole business is around 9%. Hence the ROE of the pharma business could not be more than say 5%. In the previous concall Ajay Piramal had informed that he intends to sell off a part of the pharma business which are not performing. Hence I welcome the sale of poor ROE generating pharma business. I believe that the main hindrance for the demerger is the poor ROE of the pharma business. As and when this is corrected demerger should take place. Hence the sale of parts of the pharma business was highly overdue and a step in the right direction. If the sale goes through, Piramal will have plenty of funds to deploy at more than 20% ROE in a collapsing real estate market, gasping for finance, where he will be the lone savior, minting money from the opportunity at very high ROAs. The collapse of the real estate market has already been predicted by the Piramal Management several times, and only the top 10% real estate developers are expected the survive. We need to trust and believe in the genius of Ajay Piramal to do the right things to enhance shareholder value.

Disclosure: Invested

6 Likes

Significant upcoming term debt repayment: PEL has term debt repayment of about Rs 4,424 crore in fiscal 2019 and Rs 2,208 crore in fiscal 2020 (for the non-financial business), which will require part-refinancing as cash generation from operations and available unutilised bank limit may not be adequate. Nevertheless, PEL’s management has demonstrated its ability to arrange for refinancing of debt obligation in a timely manner, and is expected to continue to do so.

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Piramal_Enterprises_Limited_September_17_2018_RR.html

1 Like

Maybe now the decision to sell the contract pharma manufacturing business appears more logical? A lot of that debt would be denominated in foreign currency since it was taken to finance the overseas acquisitions.

Hi

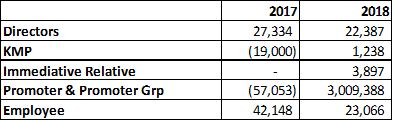

I think we might be inferring at a first level. Looking at it more granularly we come across this data( Jan 2017 onwards till now).

This is the acquisition of shares each category has done.

In 2017 the CFO who has been getting ESOPs for a long time seems to have sold in the market ie 19,000 shares He owns ~200K+ shares still as per AR.

In 2017 the promoter group except the Piramal Corporate Services Ltd Trustee of the Piramal Welfare Trust rest of the txns seem to be exchange of hands. This welfare trust actually over the years has been a major acquirer of stocks (32 crs acq vs 8 crs disp).

Out of all the individuals (outside the promoter group) there has been only 1 employee who sold shares - 500 of them, I think he still holds 7500 shares.

So calling it manipulated might not be the right thing to say imho basis this data.

Rgds

6 Likes

Hi Deepak,

My claim that its manipulated isn’t from this particular data. The inference from the data in the post is just that there has been continuous selling by insiders.

As for my claim of manipulation, it comes from technicals. For that, i have to go back to my early research in this post and then a follow up in another post in the same thread.

Based on these two charts, it looked likely to me that a false breakout was coming as pointed in the post above.

and that is what transpired

This is solely based on the price/action I observed during those weeks in August. This is the time there were rumours in the media of demerger and then AP appeared on CNBC giving interviews just after the false breakout. I have noticed this sort of thing is very manipulated and happens from time to time in all sorts of stocks. VIP is a recent example that comes to mind. This is solely from my experience observing how the markets function skeptically and how stories are spun. This is why I made the claim that the price-action in August/early Sept was very manipulated. The same thing happened in March last year when PEL was in the news regularly and the activity in this thread was on a high (usual red flags for me). Just thought I should clarify.

Regards,

7 Likes

Blockquote

Piramal has approx 22k crore listed as non current investments in balance sheet. That is almost a staggering 40%,any one scanned the annual report recently to see where this money is?

Answering my own question , significant part of the 22k crore investments include subsidiaries and ShriRam Group Investments

After first glance of the Annual report at this price the company is looking severely undervalued unless the numbers are false at the current prices. I am not sure Mr Ajay Piramal would risk his reputation to do a satyam. The price fall is beyond comprehension.

Edit: Just realized i missed the debt !44000 crores of debt!

Total Assets: 72000

Debt:50000

Net: 22000 Assets , so more fall on the way as its market cap is at 34k?

The whole annual report is full of details , but drowned me in data. However too many subsidiaries and related party transactions

3 Likes

I am not sure how exactly CCDs work, so i may be wrong. Ccds worth 5000cr should be added to networth in April 2019 at ~2700 per share

Based on this, the stock at CMP could be trading at 1.3 times april 2019 book value.

Disclosure : invested (partly), will be looking to increase allocation as i gain understanding of the businesses.

Word of Caution here - Lately data like P/B ratio, RoE are readily available on websites that so often a lot of individual investors (including myself) dont make the effort the calculate from detailed accounts.

Piramal is a Serial Acquirer. As a result, a lot of the assets on the balance sheet have been paid for at more than the original book value. As a result, there is an element of Goodwill in the Balance Sheet which needs to be taken into account while calculating RoE and P/B. My first glance at the Consolidated Accounts for FY18 shows there is goodwill of roughly Rs 5600 crores. Thats 20% of your book value which is actually not ‘Book value’ of the Loan assets. Another Rs. 4200 are Deferred Tax Assets which are not going to generate any income, but will be offset to reduce Tax expense. There are other fairly large investments which are accounted under Fair Value method (due to which the book value inflates in a rising market and conversely, the book value would fall in a falling market).

I feel all of these have to be accounted for while one applies a growth % on book value - What is the component of book that would actually grow at 15-20% and what is the component that would not.

Secondly, whenever there is a debt to equity conversion, the number of shares also go up. The book value (which is a historical value) per share decreases. However, the future earnings (which is a future value) available per share also decreases. That is why market values companies that dont dilute (For eg: Gruh) higher than companies that fund their loan assets through additional equity.

Thirdly, Piramals lending business is in its initial few years and although there has been income recognition on loan assets, there seems to be virtually no provisioning made to account for credit costs. A lot of RE Wholesale and Corporate Loans have an initial Moratorium in which there are virtually no repayment obligations for the Customer but the Lender recognizes interest Income on accrual basis. Once the moratorium ends, the true colour and risk of the loan book gets reflected.

I have posted my concerns in the past on this thread about how credit costs need to be accounted for while calculating expected growth in the future.

Disc: Was holding earlier, but exited at 2900 when better sense prevailed. Not thinking about entering any time soon.

21 Likes

Blockquote

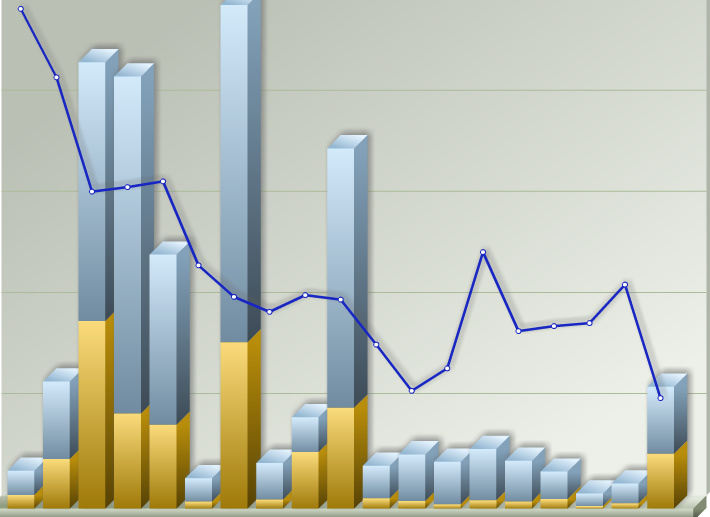

The stock is correcting significantly from the start of trading window closure on 18 Oct . Only 25% deliveries are seen,The window opens only after 27 Oct… Any insights…

I don’t think so. Infact the falls have been correlated with increase in total volume trades and delivery percentage. Infact the rises have been assosciated with poor volumes and deliveries. Attached last one month volume,delivery and price action

The long term record of Mr. Piramal was in pharma sector so extending its implication for the real estate investments itself was not correct. Now he wants to sell part of pharma for whatever reasons which was supposed to generate long term annuity type returns. My question is

Despite his legendary management ability, why did he fail to turn around the biz if is really not yielding good returns?

What changed in the market place for him to dispose an asset in which he created massive wealth in the past?

IMO, the business of buying and selling assets will hit a major speed bump someday. People compare him with warren buffet of India who created wealth by running acquired businesses profitably. I think Mr. AP is showing all the signs of a normal hedge fund manager who is constantly trying to optimise the portfolio. He sees folks making money in financialization so he plans full fledged financial play. He finds ARCs making lots of money so he plans an ARC play and so no. How many folks in the world created massive wealth in the real estate sector?

1 Like

In 2008 melt down, piramal enterprise fell ~55% and bajaj finance fell 88% (44/- to 5/- iirc) from top. Of course, not exactly a like to like comparison and a bit silly of me but still worth mentioning i thought.

4 Likes

Piramal’s exposure to real estate is a concern

Ladies & Gentlemen,

Piramal Enterprises Limited has today issued a press release that refutes all baseless rumours of any sort/form that have been floating around with respect to its real estate loan portfolio companies.

Please find below the press release -

Piramal Enterprises categorically Refutes Baseless Rumours on Real Estate Lending Portfolio

Mumbai, 21st October 2018: Piramal Enterprises Limited (‘PEL’, NSE: PEL, BSE: 500302) today strongly refutes all baseless rumours of any sort/form that have been floating around with respect to its real estate loan portfolio companies. Among others the rumours relate to loan defaults to PEL/Piramal Capital & Housing Finance Limited (PCHFL) by real estate developers such as Lodha, Omkar, Vatika, Embassy, Radius, Nahar, Aristo, Supertech, etc.

PCHFL, the wholly owned subsidiary of Piramal Enterprises, provides various financing solutions in the real estate sector such as early stage private equity, structured debt, senior secured debt, construction finance, flexi lease rental discounting and housing finance.

Piramal Enterprises would categorically like to state that we have an extremely robust loan processing and recovery process including risk management and asset monitoring system. Developers like Lodha, Omkar, Vatika and Embassy referred to in the rumours are part of our lending portfolio but have never defaulted on any interest or repayment obligation to PEL/PCHFL.

Additionally, contrary to rumours, PCHFL has not extended any loan to developers like Aristo, Nahar, Supertech, Radius and Amrapali. Therefore, there is no question of any default on loan repayments by these developers.

We have scheduled an earnings call post our Board Meeting for adoption of Quarterly Results at 6pm IST on October 25, 2018 when we would be happy to share a lot more granular details on the health of our lending portfolio and our healthy liquidity status.

Piramal Enterprises would also like to state that the National Housing Board (NHB) carries out an annual inspection of all housing finance companies. PCHF received the housing finance license in end August, 2017 and accordingly, NHB has now initiated their annual inspection of PCHFL. This is purely routine and procedural in nature.

This Press release is also being released to the stock exchanges.

For any further clarification, please contact us at investor.relations@piramal.com

8 Likes

IF Vatika default, they will take over the project and get it completed, is what Mr.Primal and Mr. Jignaa stated in their respective interview. They do not specially mentioned vatika but for the overall default scenario.

1 Like

Not as per this:

https://www.99acres.com/property-rates-and-price-trends-in-delhi-ncr

It seems to be an avg 10% rise or 4/5% cagr and being up from lows doesn’t mean much. On the contrary, on ground discussions with people will tell you that most of NCR seems to be reeling under extreme stress with no revival in sight whatsoever.

2 Likes

not true about your contention. one can see property sales slowly increasing in pockets. in mumbai’s dahisar west along the proposed metro route, the price of a 2BHK measuring 600 sq ft is now Rs 1.30 cr and transactions are happening. There are even investors who expect further appreciation once the metro becomes operational in two years’ time. I am seeing this kind of activity after three-four years.

in fact I am surprised how piramal has priced the piramal Aranya project. Rs 3.3 cr for a 2 BHK measuring 750 sq ft. the project is at byculla close to south mumbai. those holding one flat in borivli dahisar and looking to invest in another can easily move into piramal aranya which promises a better proposition. wonder what’s the catch here, though

disclosure: holding piramal enterprises.

Mumbai is a different kind of market. Rules of auction market apply here rather than any logical valuation. In big cities of India and China homes are ticket to a decent survival rather than the purpose of being just another home. It allows you to fufill your dreams and a means to have good enough lifestyle. This is what I gather after talking to few who continue to buy the same. Particularly in Mumbai a large of celebrity population need to have a base here. Ofcourse these are overvalued but one can’t use traditional method to say normalisation is nearby.

1 Like