this report covers the DRG business in depth

disclosure: holding

shiv kumar

this report covers the DRG business in depth

disclosure: holding

shiv kumar

@rohitc99 - In “Equity Method” of accounting for inter-corporate investments, dividends don’t pass through P&L, but are only deducted from the investment line-item. Any share of gains or losses of investment passes through P&L.

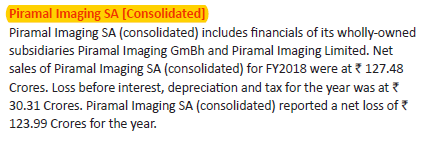

It seems like their Imaging business is consolidated as per it’s description on page 142 (and not accounted per equity method) on FY2018 annual report. Below is the screenshot. So this means all revenues, expenses, assets and liabilities would be consolidated/merged.

Per page 272 of annual report, Piramal Imaging SA had negative networth of 489.15cr. I have limited understanding of what accounting implications would be on disposal of subsidiary which had negative equity. Below are some of the questions that I have. Will appreciate if any accounting expert can educate me here:

My understanding is that if assets and liabilities of Imaging business will no longer be merged started next quarter, then the consolidated equity will go up in this case as Imaging business had negative equity.

All views/comments invited.

Disc: invested

Annual share of losses should have been passed through p&L to create the negative networth. If they are booking more loss in the P&L then wouldnt that mean that they have exited it at a further loss than what was already accounted for?

In the name of diversification , it is known as diworsification . Flashnet deal is High Alarm event for the existing investors. People claiming that it gave 30% CAGR . But from Piramal past price chart we saw that stock give 8% cagr from 2004 to 2012 and then finally break out happened after Abott deal .My question is How many of us that patience to be get FD return from Stock market when no brainer HDFC Bank /Gruh give sure shot 20% cagr for next many years? What is the guarantee that Abott like situation will happen in 8 years or after 16 years. Honestly I don’t have that patience

I did some further digging. Imaging business was acquired around April 2012. Below is what Mr. Piramal wrote in his chairman’s letter for FY2013 annual report.

It’s numbers were provided starting annual report of FY2014. I see negative equity balance of 89.85cr with annual loss of 67.51 (surprising to see negative equity in early years). My guess is that PEL would have paid a premium as this business achieved significant milestones with USFDA and EMA and all this premium would be recorded as Goodwill on PEL’s balancesheet.

The purchase of imaging business was done on making progress in it’s ongoing research and come up with a commercial drug for Alzheimer’s disease. In short - burn cash until any success of drug approval. This is the reason why it would have generated huge research expenses every year making losses and making bigger negative equity balance every year. While in the subsidiary books’ equity turns negative (which is consolidated), goodwill in parent’s balancesheet stays in-tact.

My guess is this write-off of 452cr towards Imaging assets is writing-off the goodwill it paid during acquisition in 2012. On top of this this business has burnt around Rs. 800cr in annual losses between 2012-2018.

If my guess is correct then with this sale negative equity (more liabilities than assets) of Imaging business will not be recorded on b/s anymore and reduction in Goodwill shall offset any decrease in liabilities with not much change to overall equity/book value.

All views/comments invited. Thanks.

That sounds logical.

Considering the fundamentals and losses they have generated till now, they should have impaired the asset, not sure how they managed to continue without impairment. I am just wondering if they have more assets which should be written down but they are showing them at book value.

Even the current announcement should have been better and explain what they brought it for, how much they further invested in the business and how much they lost more on the sale of the business. As opposed to saying its a one-off item; and clearly avoiding more information on it.

I am fine with them making business mistakes. If you try 10 things you can go wrong in 2-3 of them. But the mistakes shouldn’t be big and the company should be quick in cutting losses. But what I personally don’t like is that they are not forthcoming in sharing details of mistakes and try to hide them while discussing 30 yr track record etc

Disclaimer: Invested with a small position

Great analysis @rupaniamit - thank you for digging up on facts and putting them up. I think your guesses are correct.

No response from management to phone to queries on this. As I understand, given the current challenges, it may take much longer, if at all they plan to do so.

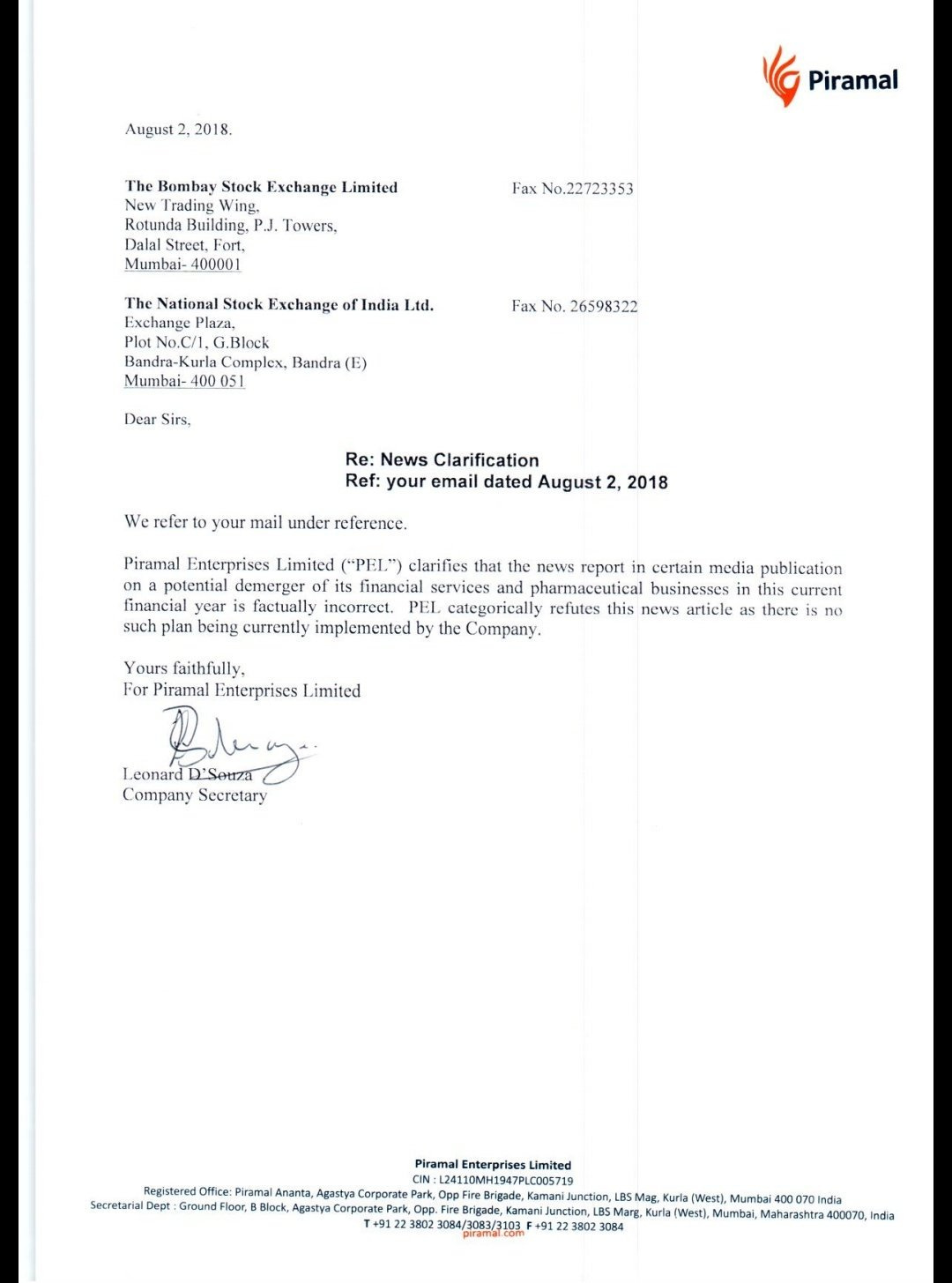

The Exchange has sought clarification from Piramal Enterprises Ltd on August 02, 2018 with reference to news appeared on : www.business-standard.com dated August 02, 2018 quoting “Piramal set to demerge pharma, finance arms, and list them on stock exchange”.

The reply is awaited.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=3b1c6639-6f7d-4d2c-a064-56075c18636e

Company clarified. It’s all rumours.

I won’t set much store by the denial issued by Piramal. The demerger has been on the anvil for the past few years. The news report speaks indepth about valuations done on the finance and pharma sectors, it could be that the Piramal family and board are weighing the pros and cons of the whole exercise.

disclosure:holding

If you read the clarification carefully, it seems the demerger plan is for next financial year. They are refuting that no such plan is currently being implemented and hence potential demerger in this financial year is factually incorrect !

Agree with you on using acquisition method for subsidiaries. Not so sure about goodwill on acquisition - did not find any numbers in FY13/14 annual report even though for other acquisitions they have given goodwill figures.

My guess is that since retained earnings of Piramal Imaging will no longer be consolidated with the parent, the negative retained earnings of PI will have to be removed from consolidated level. Consequently the whole loss reported in the past (which had accumulated on the balance sheet at consolidated level), will now be reported in the P&L as a one time loss. Retained earnings at consolidated level will of course be same both before and after sale. Makes sense?

I agree that looking at current GNPA numbers on a loan book that’s growing very fast is misleading. But at what time period should one draw the line - to illustrate the case in point (using current NPA in crores and loan book figures in past)

1 yr lagged GNPA - 141/28648 ~ 0.5%

2 yr lagged GNPA - 141/15998 ~ 0.88%

3 yr lagged GNPA - 141/7611 ~ 1.85%

4 yr lagged GNPA - 141/3193 ~ 4.4%!!

PNB Housing Finance for example quoted 2 year lagged GNPAs at 0.7% - they have a similarly fast growing loan book.

PEL didn’t publicly disclose the acquisition amount so they would not share in annual report. Here is the link confirming that acquisition amount was not disclosed. PEL bought intellectual property (patents + trademarks + know-how) worldwide development, marketing and distribution rights of lead compound florbetaben as well as other clinical and pre-clinical assets of Bayer. Given all these advantages, I don’t see a reason why Bayer would sell it’s imaging business to PEL at or below book value. There are good odds PEL paid premium and recorded goodwill for FY2013 for this purchase. Also I see goodwill going up from 587cr in FY12 to 4004cr in FY13 which may include goodwill for this specific purchase.

My friend @kanwalpreet18, in consolidation method all revenue, expenses, assets, and liabilities of subsidiary are merged/consolidated. Portion of profit/loss and equity that is not owned by the parent is recorded as minority interest in both P&L and B/S equity. With all due respect - your comment about merging retained earnings of Piramal Imaging in PEL books does not make sense.

When you say “negative retained earnings of PI will have to be removed from consolidated level” - in other words I feel what you are saying is that all losses incurred by PI so far have to be removed and instead replaced by a single line-item with “grand total loss / write-off”. I don’t think this is prescribed method according to accounting standards and it doesn’t make any sense to undo all small losses and replace with a single big loss. Each annual losses of PI have already been consolidated (reducing parent’s equity every year) and it cannot be undone when you sell your loss making subsidiary. Prior multiple losses just cannot be removed in this case and replaced with single big loss.

Below is what management stated about write-off in their presentation:

Management is writing-off Imaging business assets, I feel its nothing but goodwill which remained untouched all these years on PEL’s books while Imaging business made losses and increased it’s negative net-worth. When I try to connect all the dots, write-off of Goodwill sounds logical to me.

With all due respect - I’d prefer to not waste the precious VP real-estate by further beating this dead horse. But happy to discuss further on this “write-off” topic offline. Please feel free to IM me. Cheers!

something wrong with screener showing PE of piramal at 10 ?

Nothing wrong. this is due to tax adjusted PAT declaration post financial structure realignment. The tax saving part which they had explained in Q4. Frankly, I could not understand much into that but the 10 PE is due to that reason I believe