Both Sintex and Omkar have released results of resultant co. Demerged co results are pending. SEBI should make it compulsory to release both earnings on same day to avoid unnecessary panic and confusion.

Operating result looks decent. Almost 40% kind of jump in profits if you ignore one time charge due to demerger. GM is gone up by 2.8% and EBIDTA margin for last fiscal is gone up by 2.5% Vis a Vis FY2015-16. The WC situation looks improved (because of lower receivables and higher Trade payable). Resulting in higher cash level at the end of the fiscal. The cash from operations may also be positive this year due to this. The WC situation will improve significantly if they can maintain this discipline throughout the current year.

On the flip side the total debt is gone up by 9.9%.

It will be interesting to see if they managed to increase the contribution from the exports and higher margin intermediates and products in the overall revenue basket. One of the key thesis is that the Specialty chemical division has come up with new high margin products and over the period of time the contribution from these products (some have 60-80% GM) should alter margin profile of this business meaningfully over a period of time. Anyway they have already reduced the contribution of low gross margin Iodine derivatives over last 2-3 years. This is key monitotarable in this stock along with WC and debt situation.

10 Likes

Analysis by Dr.Vijay Malik , do check out

6 Likes

It is a very frank analysis of the company. The only thing I could point a finger at… if one could call it that is that the reduction in freight charges is a known. It is because Selenium and Iodine were imported from Chile all these years. Last year, the supplier setup a warehouse in Nhava Sheva I believe and that would be the reason for reduced freight costs and it will also impact their need to keep higher inventory since the transit time before the supplier setup storage used to be 2 plus months and thus they needed higher inventory to de-risk unavailability.

Yes that could be the reason, but why is the consumption of crude Iodine decline could be? for 88cr sale consumed 82cr and 118cr sales consumed 4cr isnt that a big difference? @valuestudent

This report is good but all history. I think we all know this regarding the WC issues, Debt, Excessive Capex etc.

Why we have bought it because the market is not capturing LASA valuations at the moment.

Vijay Malik himself gave a note that the transfer of assets to LASA has been done on generous terms in favour of LASA and market will like this.

It was all about Lasa and continues to remain all about LASA.

As Malik said WC days are 122 in Omkar standalone. Well, the same is 25 days in LASA.

Lasa is a significantly a better business than Omkar in my opinion…and if im correct, Lasa could have a valuation of something on the lines of 400cr itself.

4 Likes

This is just crude iodine. Check out the work in progress inventories of iodine compounds and calculate the stock in trade of iodine compounds.

Vijay sir is comparing the sale of iodine compounds with the consumption of crude iodine.

@admins : If I have overstepped, please do let me know…

@Hocuspocus32 @SecretInvestor @giridesh3

I am going to be frank here.

- I would like to request our own Girish Deshpande to get on the conf-call if it is possible for him to find time. We really need to grill Mr. Pravin. He should know he is like a 21 year old with a credit card that he thinks his father will pay the bills for. His father’s being “us” the investors.

Girish had at one point clearly said that the CFO is weak. I did not agree with him then but as time rolled along I understood Girish is right and I was wrong. It is obvious that only one of two things is true… a. the CFO is incompetent or b. the CFO is overruled. We need to make sure Pravin Herlekar understands his stock will become a 1 rupee penny stock if he keeps messing around with his father’s (our) trust. Either he needs to replace the CFO or he needs to listen to his CFO. Whatever the case is.

Pravin and OSCL is so deep in debt that he cannot afford to spend a penny more. I do not know if he knows “how close” he is to becoming another Suzlon. His company’s primary objective can now only be to totally remove debt even if that means tapering growth to 20 to 25%. It will be healthy and they already have the capacity to continue to achieve that growth.

-

I honestly did not know that the dividend is being paid with debt. Although hard to believe, I would not find myself able to argue with Dr. Vijay Malik. I would like for us to ask this in the conf-call.

-

I don’t know if this is appropriate or allowed to say here, but I am in all probability going to sell the oscl stock on the day of the record date and keep the lasa shares. Have you guys seen the funny photo of our new wholetime director Rishikesh in the 2016 annual report? Also, he had nothing to add in the executive directors message. He seems like charlie chaplin with his hands out! Is he singing or something? I am not going to be able to remain invested with a guy like that in charge. I do have a feeling that he might only be proxy and his father will continue to run the day to day of oscl. So if that looks like the case there is still great juice in oscl if the debt starts reducing “every quarter without fail” Even in the past I had discounted rishikesh (charlie chaplin) as I understood… boss… he is his son… let him pay him some lacs a year pocket money and let him play director director… but he has no experience or business running oscl. If daddy continues to run it, it makes sense… else… bye bye rishikesh…

Secretinvestor is right. The play is Lasa. The Play is Omkar Herlekar. It will be a good play.

Disc - I have changed my mind as I have seen facts change but only bought more and not sold anything yet. I could change my mind again and keep oscl. Who knows.

2 Likes

Let me add one more thought after further mental exercise. I don’t think there is downside risk for average price holders up to 175 ish per share when you consider both oscl and lasa. That is most important is it not? Protecting the downside. Let the upside take care if itself.

Very well put. Can some bullish investor/trader/analyst shed some light on the fact why promoters kept on selling their stake while repeatedly during con-calls said they won’t dilute their equity further. De-pledging is one thing but lying on minority investors interactions many times is another. Now its upto anybody’s comfort on the promoters. Lasa is good no doubt, however even a Aston Martin on a German track cant run well with a bad driver and accidents are probable to occur.

Discl. Invested earlier but sold after management Q&As

Why the promoters sold is clearly analysed by Dr Vijay Malik, CRISIL has rated them down and thats why they didnt have access to any funds from Banks, for this the management told that its because of delays of approval of loans from bank of baroda which seems false. They had no other option other than to sell stake to proceed with the demerger. I highly doubt its because of Lasa clubbed in this OSCL is still trading at these range.

I am gonna email all these questions to them today, so If anyone wants to include there questions do send me, I will add that too. Hope we get a satisfying reply.

1 Like

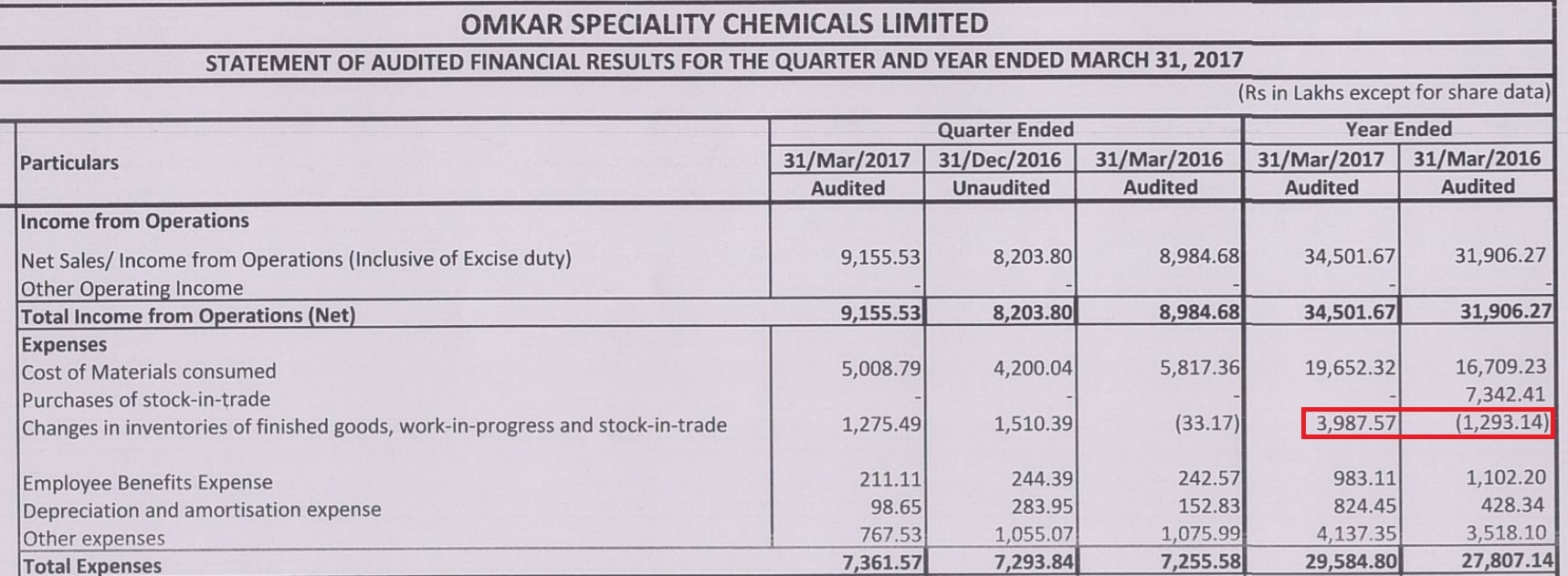

![]()

There is a significant drop in Depreciation and amortisation expenses from Q3 17 to Q4 17 . Does anyone know if there was any plant which was under OSCL ( OSCL stand alone assets and not consolidated ) that got transferred to Lasa ? If that is the case , there is a reason for low D&A going forward . Does it also mean that they have taken some debt burden from Lasa and waived it off by booking an exceptional items (and hence reducing reserves and increase debts in OSCL balance sheet) into the PnL ?

I have been told (by Bridge IR team) that Lasa would not announce anything till it gets listed and whatever number we have got is all we can work with.

As someone pointed out early in this thread , 5.91 EPS (except exceptional items) for standalone entity is improbable and the disclosure is all the more confusing…

Press Release just out on the performance of the quarter for oscl.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/44796bdb-88a2-4331-acb2-76a238c33b15.pdf

Pravin Herlekar seems to be trying to communicate that he has understood the price of debt and is openly saying he will moderate. That a watchable but a good sign. Also, It is signed by him and not Rishikesh (Charlie) so that’s a pointer.

1 Like

so here you go the response

Dear Shareholder,

As discussed, PFA herewith press release on the financial performance of the Company for the Quarter and year ended March 31, 2017 for your reference.

For any other query request you to attend Conference Call to be held on Wednesday, May 24, 2017, at 04:00 pm. (Ph.: +91 22 3960 0547)

Thanks & Best Regards,

Sunny Pagare

(Company Secretary Dept.)

Omkar Speciality Chemicals Ltd.

B-34, M.I.D.C., Badlapur (East),

Thane, Maharashtra, India – 421 503.

Questions asked was

- What is the promoter holding % inclusive of the shares pledged as of Today.

- How much % of promoter shareholding is pledged.

- Why has the freight charges Declined for the company with increasing sales?

Sales increased from 265cr in FY2015 to 413cr in FY2016, the freight and transportation expense at consolidated level has declined from ?1.71 cr. in FY2015 to ?1.70 cr. in FY2016

4.Increased sales of Iodine and Selenium derivatives, but decreased consumption of Crude Iodine and Selenium metal in FY2016. Why is that?

As per the annual report for FY2016, page 118, the sales of Iodine compounds increased from ?88 cr. in FY2015 to ?118 cr. in FY2016. The sales of Selenium compounds increased from ?16 cr. in FY2015 to ?22 cr. in FY2016:

The consumption of crude Iodine at consolidated level declined sharply from ?82 cr. in FY2015 to ?4 cr. in FY2016. The consumption of Selenium metal powder declined from ?7 cr. in FY2015 to ?5 cr. in FY2016

5.Unit 5 : Status?

As per the annual report for FY2016, page 47, the company received the environment approval for the unit in January 2016.despite the receipt of clear directions/steps to be taken by the company to meet the compliance requirements, the commencement of unit 5 is not yet started why is it?

- Operating Capacity Mentioned Vs Rated Capacity ? Why is there a difference? why dont we use rated capacity as its the one which makes more sense?

- What is the plan to bring promoter stake up? Will they bring the holding back to 65+% ? What is the plan ?

- What is the status on Working Capital loans ? Have we gotten the working capital loan sanctioned ?

- When are we expected to exhaust the capacity ( assuming Unit V won’t start for sometime )

2 Likes

Conference Call Updates

Lasa Unaudited Standalone

31 Mar 2017

Topline 200 Cr up from 136 Cr

EBITDA: 22%

Scheme of Arrangement

Awaiting update from SEBI for listing date for Lasa

Management expects listing of Lasa before end of June 2017. “Knowing OSCL I would discount and say they should list at-least by August 2017”.

OSCL

Growth guidance at 15-17%. “They seem to now being conservative. Good sign”.

Being Prudent with Further Business

No More Shares Will be Sold. De-pedging will happen but no more shares will be sold.

We are committed to increasing our shareholding. Will update after board meeting.

Management is confident of holding margins.

Girish Deshpande was also on the line. Await his opinion as well.

My opinion: I am positive on OSCL & LASA going forward.

Disc - Invested.

4 Likes

Anything about unit-5?

It looked more of a session where people were asking questions raised in Dr. Vijay Malik analyses.

I do not recall anyone asking about Unit 5 status. Any thoughts by any fellow members?

Also, i was not able to understand the management trying to answer exceptional item of 63 Cr. The networth comes down due to revaluation but at the same time, 63Cr hit is taken in P&L account. So why such a large hit? Management answers didnt seem convincing

If any experienced/accounting background fellow members can update here please?

Very small amount (about4-5 Cr) remains unpledged it is? Then what are they waiting for? If the topline n EBIT growth is good, can this small ‘headache’ not be cleared?

Disc:Invested

They have said so many times that further promoter shares will not be sold that now Noone will believe it until they unpledge the entire remaining stake.

It is also more difficult to believe that they will be able to list last before June 2017.

1 Like

No Akhil. No one asked about it. But as we last know, the unit is ready to begin operations and it was the new regulation for effluent treatment that held it back. They will not be able to comment on when they will be able to start till they get the approval, the govt. has to send them a notification.

@sumitg04 You are right on the pledging but now it is a unsubstantial amount and not one that puts the company at risk if the NBFC was to have sold the promoters pledged holding if the share prices fell with a market or any other correction and they could not put up the margin money. That was the main worry. The promoter shares would have just landed in the open market leaving it open to anything from takeover or so many more other outcomes. That issue is now de-risked. It’s ok now since they have de-pledged the majority and it is a small, safe and manageable percentage that remains.