Why should you even track this and bother about it, if you are long term investor.

May be HDFC Bank where FII holding levels had come down to 73%. Cap is 74%.

Why should you even track this and bother about it, if you are long term investor.

May be HDFC Bank where FII holding levels had come down to 73%. Cap is 74%.

Dear @nav_1996

I just wanted to apologize for my preconditioned response to anyone who gives interviews etc… have just stopped watching and listening because of the garbage that I have heard 99 of 100 times.

You are right, if one keeps an open mind, one will learn more.

Now after having used some strong words on hero worship etc… ![]() I want to say sorry and thank you.

I want to say sorry and thank you.

Sorry to Mr Kenneth for the language I used and thank you to you for posting that video and introducing me to a person with such fine thinking.

I saw the video now, I learned a lot, and every word he said made me think I am listening to Benjamin Graham. Both would have been pleased to meet each other and chat. I could sit and listen to this gentleman talk for hours and days ![]()

He is a very humble, articulate and value driven investor and obviously a wonderful human being.

When will I ever reach these levels of sensibility and humility.

I am exactly doing that for last 3 days. This was the first time I listened to Mr. Andrade for the first time on this thread only and now I have devoured whatever is accessible on YouTube.

This argument about high PE and low PE stocks creeps into valuations discussions very often.

We often see many businesses quoting at seemingly high multiples forever and stay away from them while it is also true that many businesses always seem to be quoting at low multiples making them attractive. Businesses also get re-rated suddenly and their PE just shoots up and vica versa.

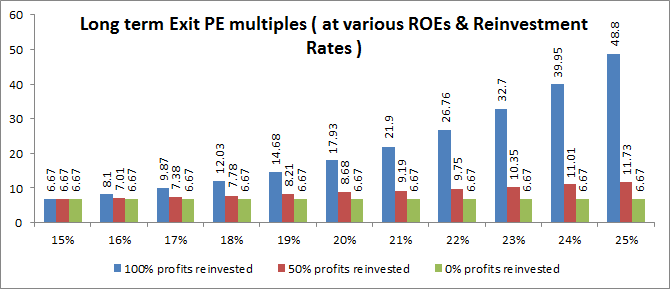

From a shareholder value perspective a company has only two jobs to do - First - increase the gap between Return on Equity and Cost of Equity & second - keep finding reinvestment opportunities for a long period of time. If the marketplace believes that it can do both successfully - the market rewards it by assigning it a high multiple. There are few companies that continue to do that and we know their names by heart by now.

Following is the chart of the long term exit PE multiples at various ROE’s and Reinvestment rates. The vertical axis is the exit PE & the horizontal axis is the ROE. The bars represent reinvestment rates.

If your ROE is equal to your cost of equity (15%) over a long period of time - the exit multiple is 6.67 no matter how much the company reinvests. The PAT growth for companies which invest 100% of their profits is 15% under such business economics - a good growth rate by any means - but you cannot give more than a 6.67 exit multiple. Many very good companies in growing sectors with plenty of reinvestment opportunities are in this situation and seem to trade at ok multiples for this reason.

However, when the business increases this gap ( ROE & COE ) , the exit multiple improves rapidly. In fact if the marketplace believes that the company can keep reinvesting all its profits at higher & higher ROE’s, the valuations become irrational and the exit multiple at 25% ROE & 100% profits reinvested can reach crazy levels. In the long run, no company can keep on doing that but in the short run many can. These 50%-60-70%% falls that we see from the peak are when the marketplace realizes that its not possible and the multiples drop rapidly.

If the reinvestment opportunities go down or the ROE’s drop , multiples come down with a vengeance. Its rational for them to do that. Whats irrational is investors extrapolating good times to infinity and believing in them

This often happens when great companies come down a notch and become good. Its still a good company no doubt - but its no longer awesome. The difference between awesome and good is thin but its a graveyard.

A company that generates a 20% ROE and is able to reinvest 50% of its profits a good company but deserves an exit multiple of ~9. A great company which generates an ROE of 25% and is able to reinvest 100% of its profits for a very very long time deserves an exit multiple of ~49. The difference in multiples is huge.

Over time, I think one should look at incremental ROE’s improvements and reinvestment rates to spot companies where the market has not rerated it a lot. The opposite is also true and if incremental ROEs drop ( like they always do ) and companies run out of reinvesting opportunities - one should not blame the marketplace for acting they way it does.

What i do quickly sometimes to get a rough gauge of valuations is multiply the exit multiple by 2 under my normalized ROE and reinvestment assumptions. Examples

Colgate : ROE - 50% , reinvestment : 30% thus exit multiple is 21 so steady state PE is 42

Mahanagar Gas - ROE- 20% , reinvestment : 50%, thus exit of 9 so steady state multiple of 18

Dmart - ROE : 25%, reinvestment : 100%, thus exit of 49 and a steady state multiple of 98

Avanti : ROE : 18%, reinvestment : 80%, thus exit of 9.59 and steady state at 20

Page : ROE : 40%, reinvestment : 50%, thus exit of 35 and steady state of 70

REC : ROE : 15%, reinvestment : 70%, thus exit of 6.67 and steady state of 13

Views invited

Bheeshma

Btw, Google IPO was at 65 PE. And it has delivered fantastic returns from that.

PE of Amazon, Netflix etc remain super high. Profits are almost absent in these 2 companies.

PE is never the right criteria to value any company!

Dear @Vijayk,

Valuation of companies isn’t my strong suit. If my understanding is flawed, my apologies.

To me it seems that there’s isn’t any one correct manner to evaluate the investment worthiness of a company. Even the term fair value is loaded with ambiguity.

In my opinion, fair value is the price of entry that will allow maximum capital appreciation, depending on the investor’s expectations.

An investor who’s willing to stay invested in a business for 40 years may be willing to pay even 100 times earnings. To others it may seem laughable.

An investor who’s a believer of the Greater Fool Theory may be willing to pay even 300 times earnings. We saw that happening in the Mississipi Company bubble. Unfortunately, the end wasn’t very appealing.

Some investors swear by low PE investing while some swear by DCF.

At the end of the day, what each one of us is seeking is capital appreciation. We should adopt the path we’re most comfortable with in reaching the destination. Frankly, I don’t think there can ever be one right strategy for investing.

Cost of Equity of 15% across businesses is not a good assumption. E.g. If own a solid franchise like Nestle or Marico, I would like to treat that at par with a high quality bond and will not assume more than 10% as cost of equity.

Cost of equity is basically my return expectations as a shareholder. One can take any number one is comfortable with. I like 15% and find it neither too optimistic or pessimistic.

True. Here’s what Munger says on this subject.

Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6 per cent on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6 per cent return - even if you originally buy it at a huge discount. Conversely, if a business earns 18 per cent on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with one hell of a result. - Charlie Munger

Not really. A business may make 30% return on capital with zero growth for 20 years… Will make you zero money or even negative returns over 20 years.

On the other hand, a bank making much less return on capital will make you return due to equity dilution at higher book multiple and growth because of leverage.

So, in addition to ROCE, growth is very very important. Without growth, stock is worse than a bond. And with growth, stock is infinitely more valuable than a bond.

IMO, the only way this would be possible is if the entire profits of the business is distributed to the shareholders.

Not if you take the hefty dividends into account.

Not at all. Dividend yield is a function of market price. So, an expensive stock with 30 pe even if distributes most of its profits as a dividend…the investor will get very low yield on his/her investment. Because investor is not buying the stock at book value, but a lot more than that.

Over 20 yrs, as stock will not show any growth, the PE would come down…translating into capital loss…though dividend yield will move up…which would still be low vs cost of capital…

overall investor made loss over 20 yrs holding a 30% ROCE stock (compared to cost of capital)

A fixed deposit with 8% interest (dividend) every year with no growth and no capital loss would have fared better.

Last time in Jan when the PE ratio as suggested in NSE website touched 27.81 and then corrected after a week of touching that figure.

Market is at 27.60 today.

Not sure if the examples reflect the right numbers.

If you look at Colgate, while ROE is around 50% ( or i think a little less ), this has been under constant decline YOY. Colgate’s ROE was more than 100% till 2013/2014. They would need to outperform significantly on the bottomline in FY 19/20 to retain a ROE of 50%. Also, considering that they pay approx. 25% of book as dividend, why is reinvestment just 30%. Is the rest royalty to the parent?

Coming to DMart, ROE is 18%. Infact, just to maintain this 18% next year, they will have to cross 1K Cr in profitability in FY19. Thus, a more rational PE for DMart is 25-30 in my opinion.

Hi @sandeep17

These are future roe assumptions which could differ from people to people. Dmart at 25pe is in the realm of possibility if something drastic happens but highly unlikely if its business as usual.

Not future ROE - DMart’s FY18 ROE is 18% and I don’t see how it can go up to 25% in the near future. We cannot assign a arbitrary ROE number to justify current PE multiples - should be the other way round.

While this is not a thread on dmart and dmart valuations- in general though, i think one needs to have a view about how the future will unfold for a co and what would be its expected margin profile, topline, bottomline, return ratios etc going forward depending upon what stage it is in its growth cycle. Dmart is growing agressively and is posting fantastic numbers. Every year its ebitda margins expand. I think not only will it reach 25% roe but exceed it while expanding rapidly. If it does 7% pat margin and turns equity 4-5 times - 25% becomes a very conservative number. Similarly, i have views about other cos which may or may not pan out but i wouldnt call them arbitrary.

Not able to understand the mathematical equation between ROE, COE and % age reinvested. Would you please elaborate

That’s true. But the investor will also NOT be selling at book value. A business that’s able to consistently generate a high ROE will always command a high valuation

Unless the business was growing at a high rate before you purchased the stock, and the growth later stops, I don’t see why the stock would command a lower PE. Since the statement by Munger was about ROEs, I think it is fair to assume the condition of “Ceteris Paribus” (ie.) assuming growth to remain the same throughout the 20 year period.

Interesting post!

Can you please share the equations used to arrive at the relationship between Return on Equity, Cost of Equity, Reinvestment rates and exit PE multiples.

~Thanks!