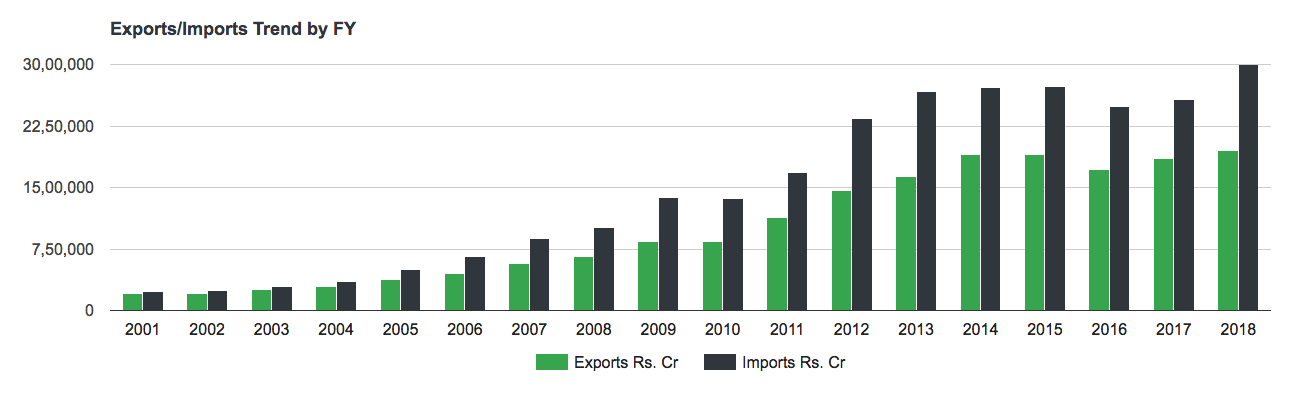

Few posts above, I had posted the exports data and how things were improving. Well, I got around to getting imports data as well and doing some more analysis and this is how the story has evolved.

Seen along with imports, the chart looks like this.

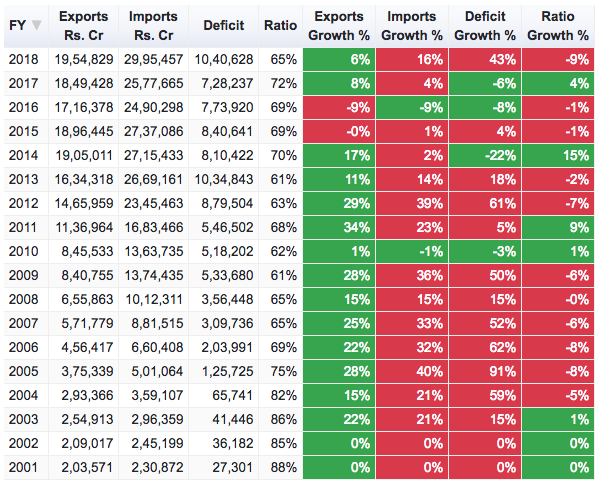

Although exports are improving, the imports have hit an all-time high and the deficit (difference between exports and imports) that we as a country owe the world has risen drastically and is at a high last seen in FY13.

The Deficit has grown 43% in FY18 thanks to crude. You can also see how good FY15 and FY16 were for us when crude was low. Although our exports by value declined, our deficit was so much under control. This is the time we built great dollar reserves as well.

Also interesting is seeing how the ratio of Exports/Imports has evolved over the years - From high 80%s in early 2000s to the high 60%s now. All that development (or mis-management and corruption) is costing us dearly as we are not able to give back enough in terms of exports. Spending energy and building cars and spending fuel to run them is not really being productive although it contributes well to the GDP. The great Indian consumption story will hit a speed bump if its driven by dependence on crude.

Its also clear how this deficit figure is correlated with the fall in Rupee. In Aug '13 Rupee hit Rs.68 to the dollar and after that it has hit Rs.68 now - Both times our deficit crossed 10 lakh crores.

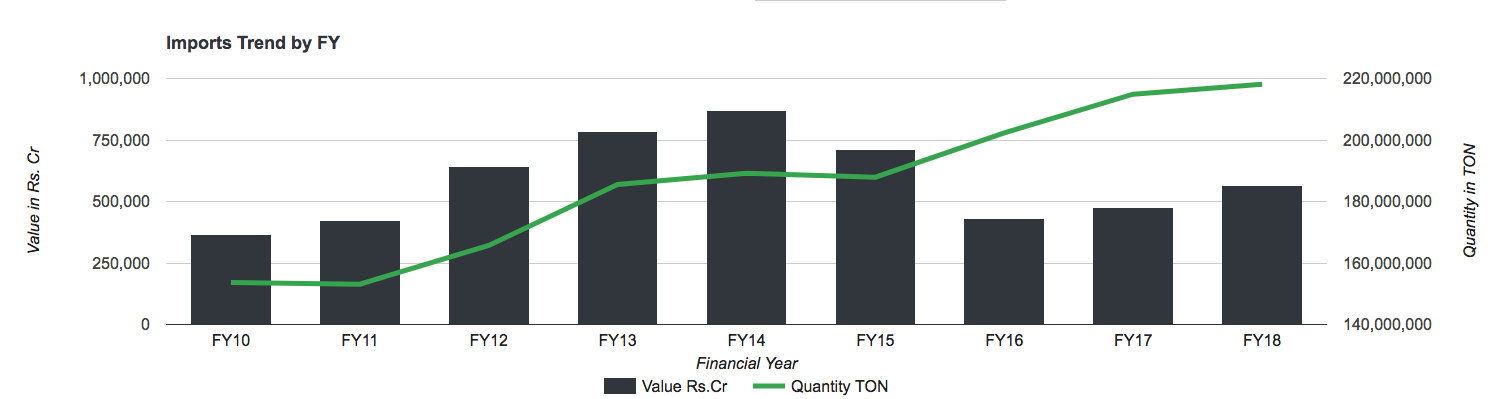

This is the chart for Crude imports.

Compared to FY13, the amount of crude we are importing has increased from 185m to 218m - Almost 20% higher, so any further increase in price of crude is going to hurt us very, very badly due to the multiplier effect.

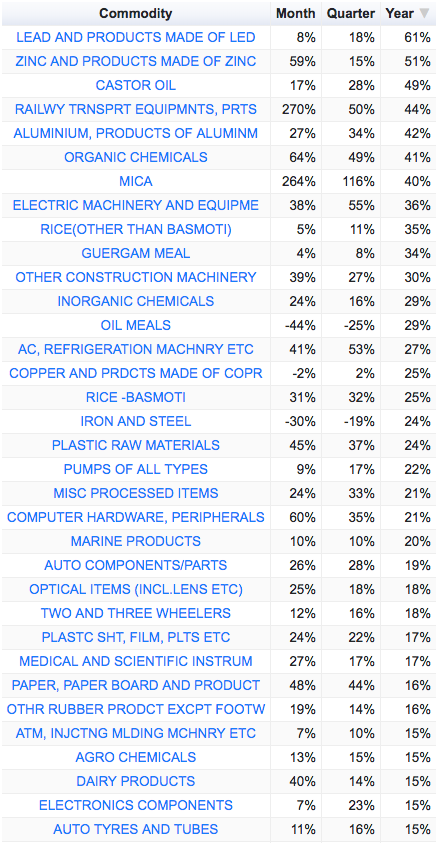

I think the consumption story will hit a speed-bump if things go along this way. The way forward as long as crude stays high and with it the deficits and along with it a weak rupee, the play might be exports.

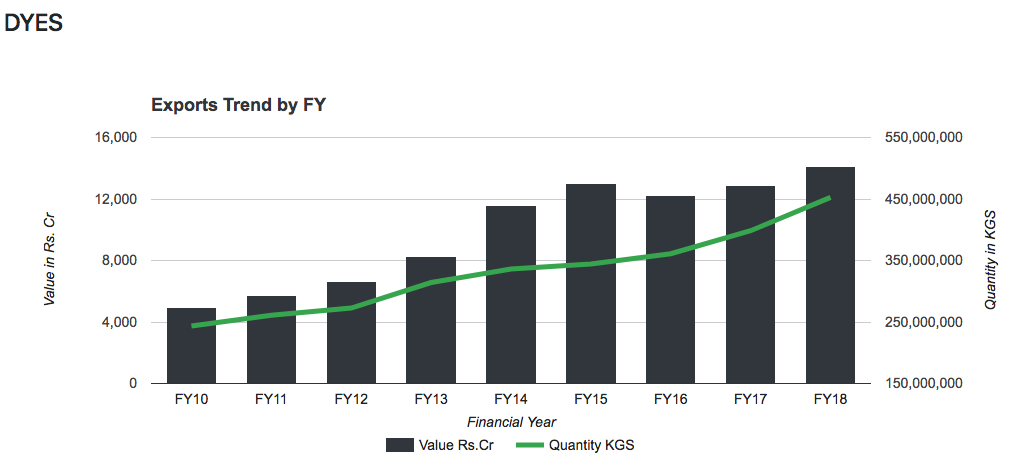

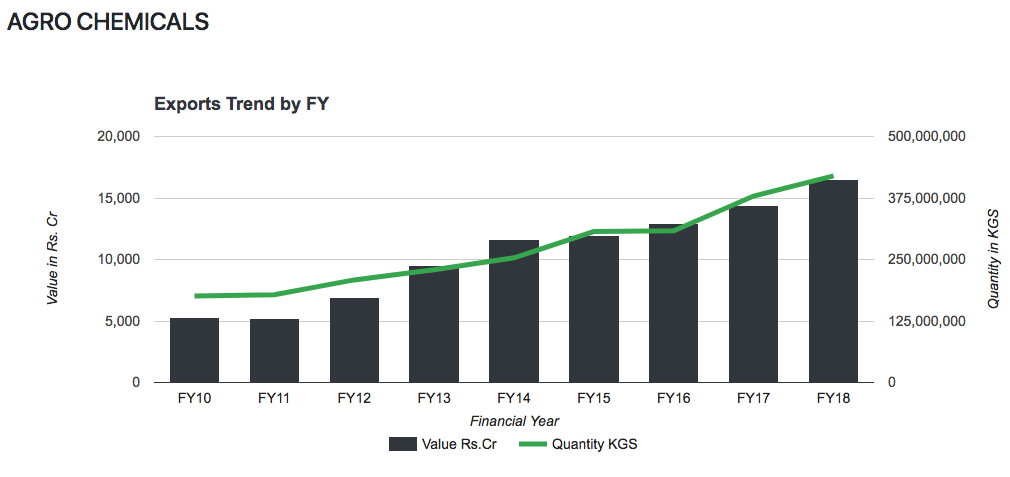

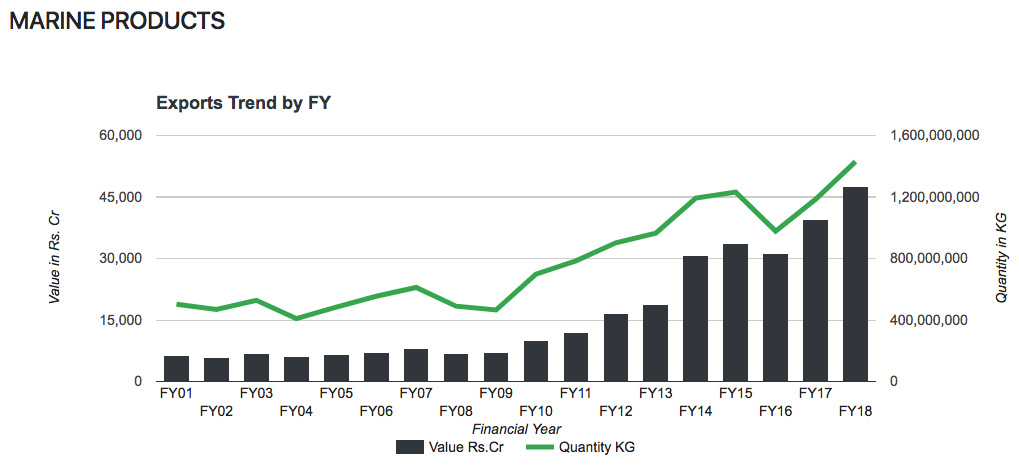

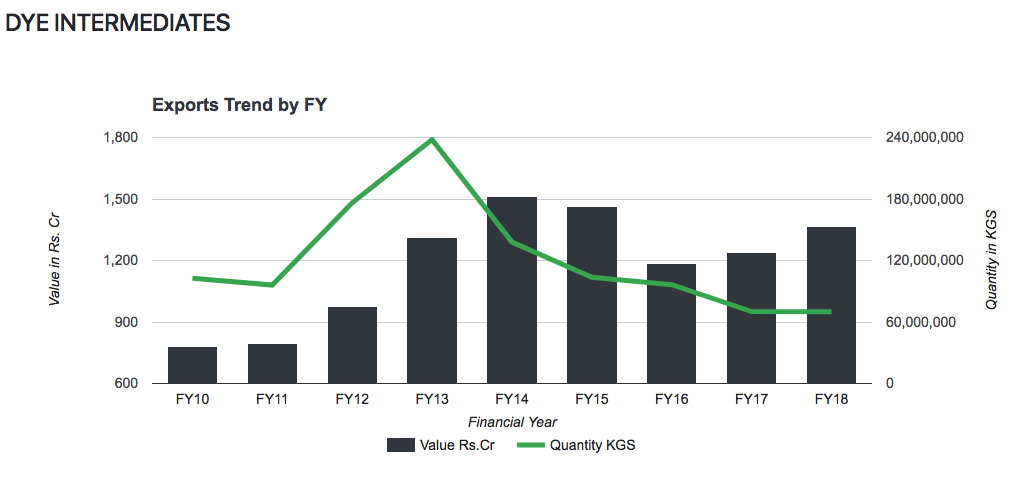

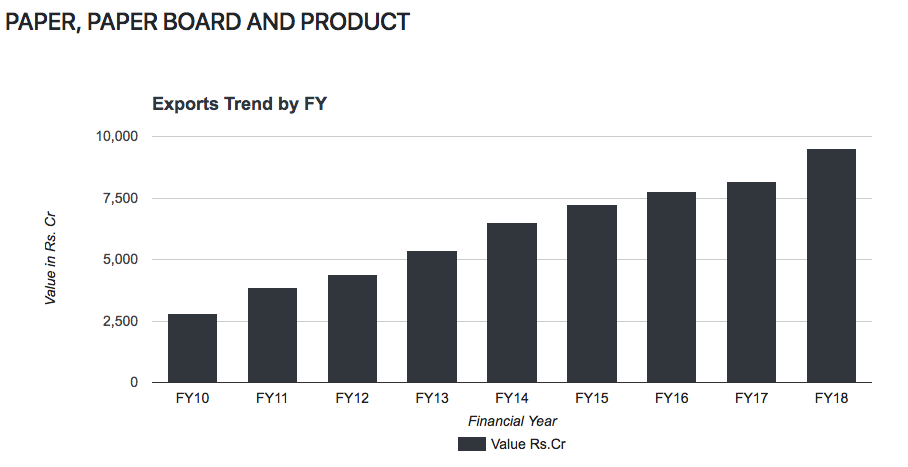

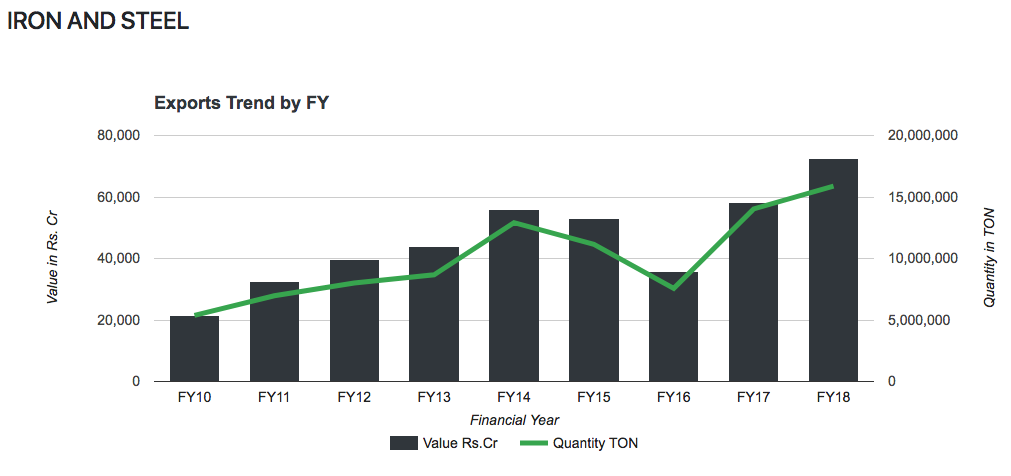

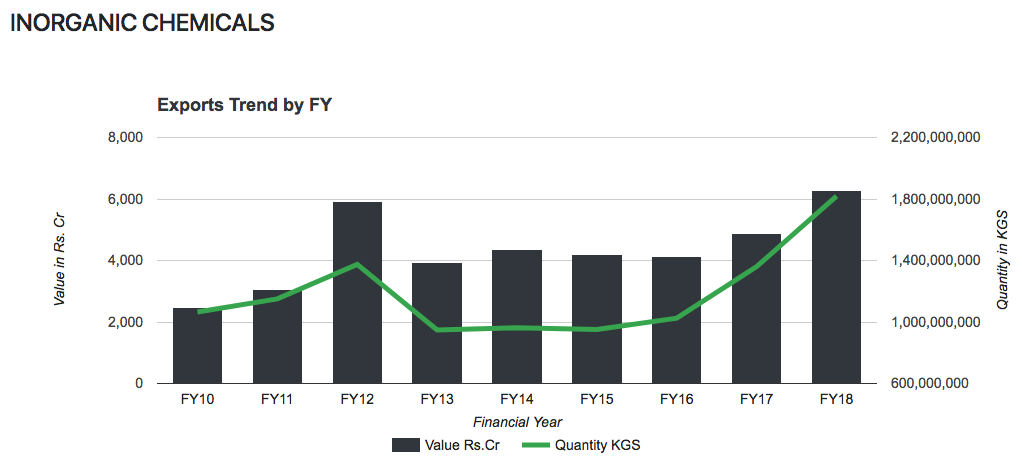

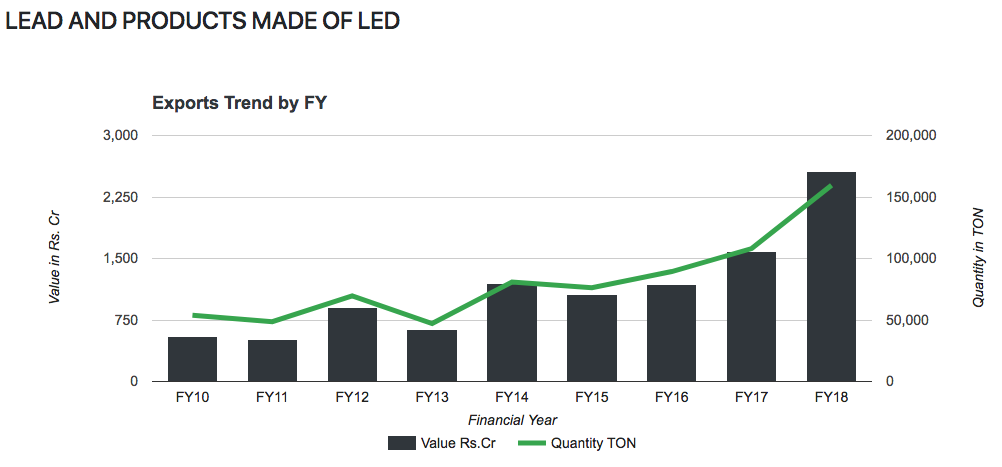

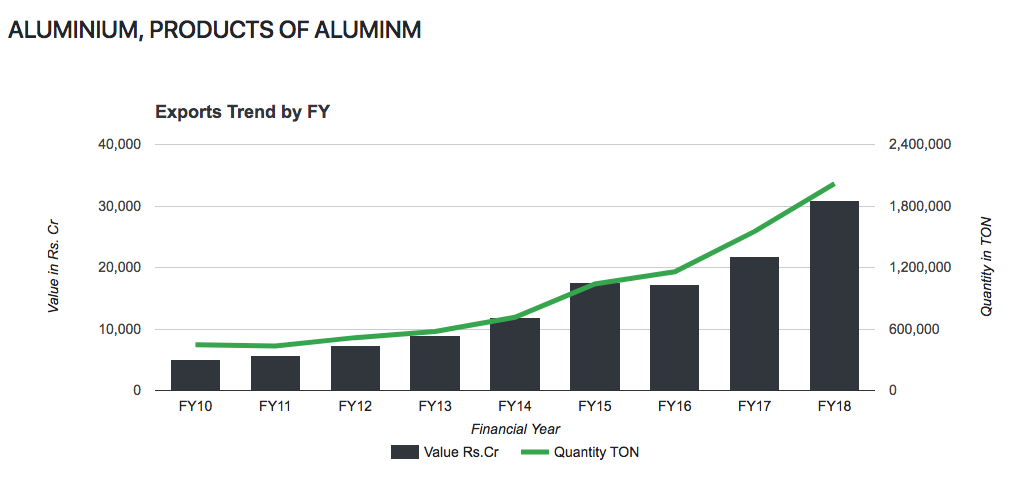

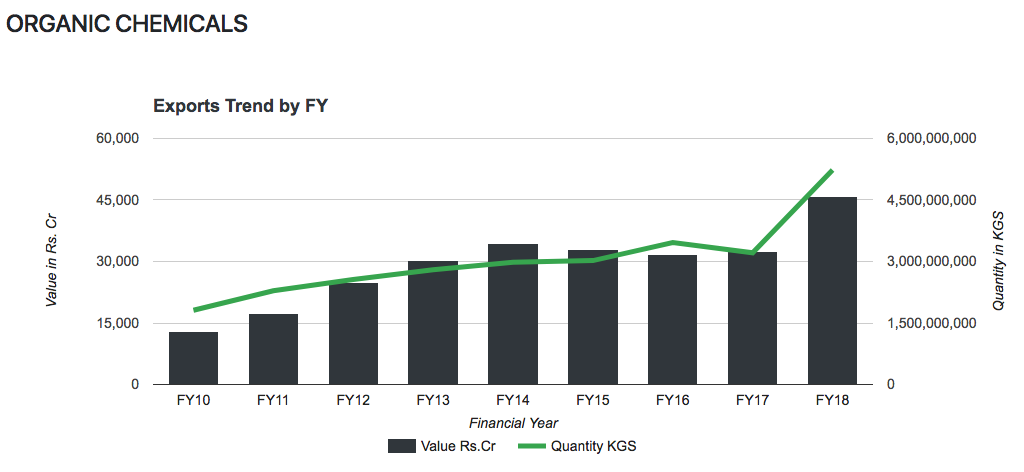

And with that, here is a list of some sectors which seem to be doing well in exports.

As I finish this post, I realise it might be a bit off-topic in this thread. The macro side of the story does correlate with valuations, as it affects the currency and interest rates, so I hope its not totally off-topic.

Note: The exports data doesn’t include service exports and is only for commodities.