Sir, how can we calculate the %ge of reinvestment. Is it the earnings - divident ?.

Pls explain, thanks in advance

Hi joseph

(Ending equity - beginning equity)/sum all the profits for the period.

You could also google “greg spiecher reinvestment” for a better explanation.

Best

Bheeshma

2 Likes

Would it be OK to add a lump sum amount into selected stocks at this elevated value of Nifty PE or should I be waiting for a lower PE on the Nifty.

Thanks

@sarthakkumar19_ Kindly refrain from asking same question in multiple threads. Also, intent of forum is to brainstorm investment philosophies and ideas but not to seek any kind of investment advice

3 Likes

Link not working. Any other alternative link

This post is fantastic. To be read along with that of Mr. Bheeshma.

If there is decent RoE and if the company is growing consistently , say, at above 15%, it is highly unlikely that the market price/demand will come down substantially just because of valuations.

All those who are scared of P/E being high, please do let me know a couple of examples in the Indian context in the last 15-20 years where a business, growing consistently at 15%+, having high P/E earlier, has come down drastically wrt market price.

Wipro’s market cap in the peak of 2000 was close to Rs 2 Lakh crores. You can check its market cap today.

It took HUL almost close to 11 years to surpass the high of 2000.

Between the high of 1992 and the low of 2004, ITC gave an absolute return of 50%. Thats a CAGR of 3% over a period of 12 years.

These have been high ROE companies all along.

5 Likes

why there is this type of huge variations in the PE of nifty small caps. thers happens during the turn of quarters. is it simply due to variations in earnings. But by this much huge variations. Can anybody enlighten me.

They usually change the composition of the index and suddenly PE number changes.

Story has been crystal clear since 2017. Cash out from Smallcap first.

But people have been too worried about Nifty50 PE while holding on to exorbitantly expensive smallcap hope trades.

You are right that High RoE is not enough, Sir. Growth in Profit > 15% and Sales > (GDP / Inflation) is also a must.

1 Like

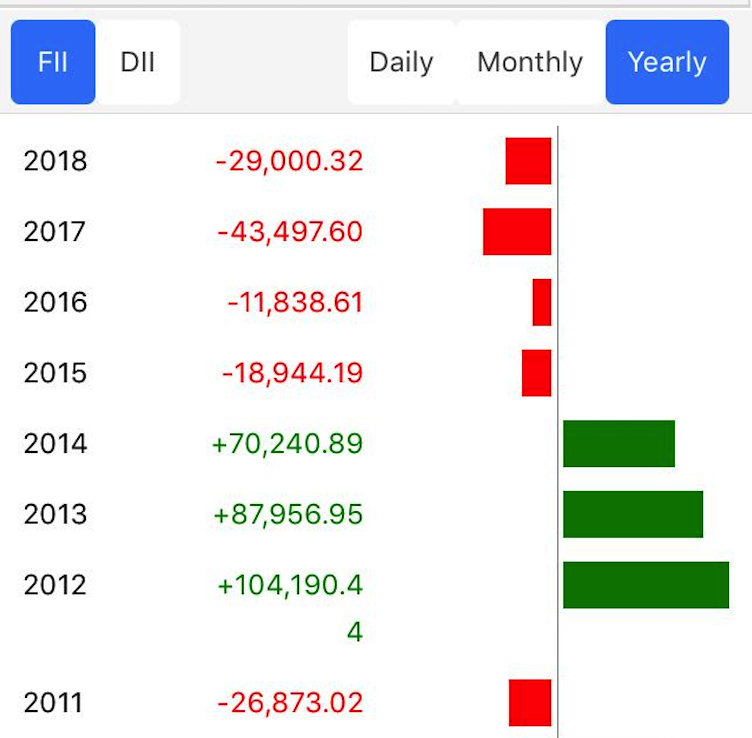

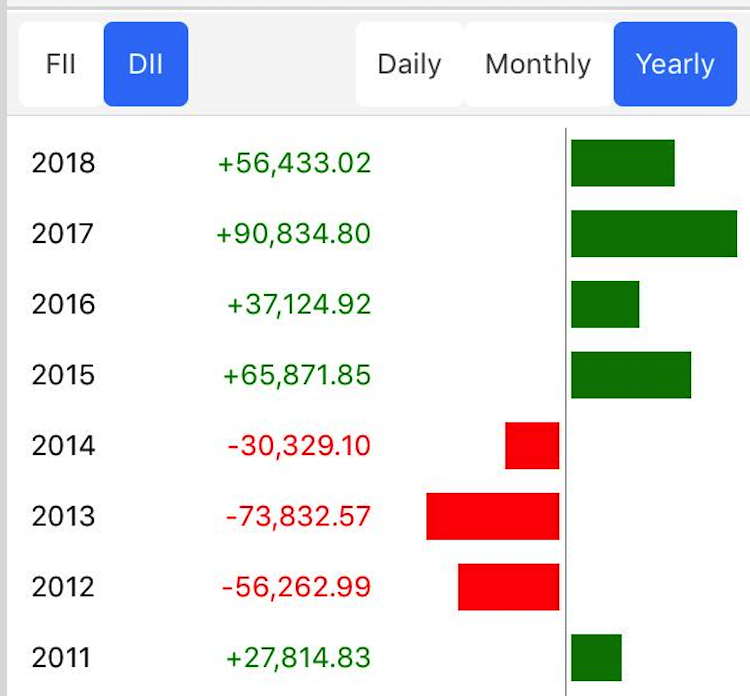

Which one is smart money…?

Who is doing classic Buy Low, sell high…? ![]()

FII bought stocks during 2012-14 very aggressively for almost 2.5 lac crore, and during 2015-18 they have been consistently selling to DII/Retail, almost sold around 1lc crore, still, they are continuously selling.

if this post is off the topic please delete it, I just thought of posting it for discussion.

Disclosure: I am short on nifty with 15% of PF, Just trying Long + short for risk balancing, as don’t want to exit the market.

5 Likes

This type of confused strategy guarantees mediocre returns. Instead, equity + debt balancing is the right strategy. See Pattu’s research in this thread above.

1 Like

Hi sir,

Have seen this post earlier. today gave a second read. I feel not only the interest rates but the quantity of debt should also be considered. If the quantity of debt is high even if the interest rates are low, it will put heavy burden on the companies. So i feel a debt to equity ratio is also to be considered while deciding the PE multiple is expensive or cheap. Am I missing something???

The “Earnings” part already accounts for the Debt burden (Interest). It’s also assumed that while Pricing the stock, the market considers D/E Ratio (Thinking along the lines of CAPM). So no, I don’t think a company’s P/E is independent of its D/E.

1 Like

From midcap mania of six months back, now the pendulum has swung to the opposite end and people are flocking to take refuge in quality like Bajaj Finance and HUL at any cost.

I hope time does not repeat itself.

4 Likes

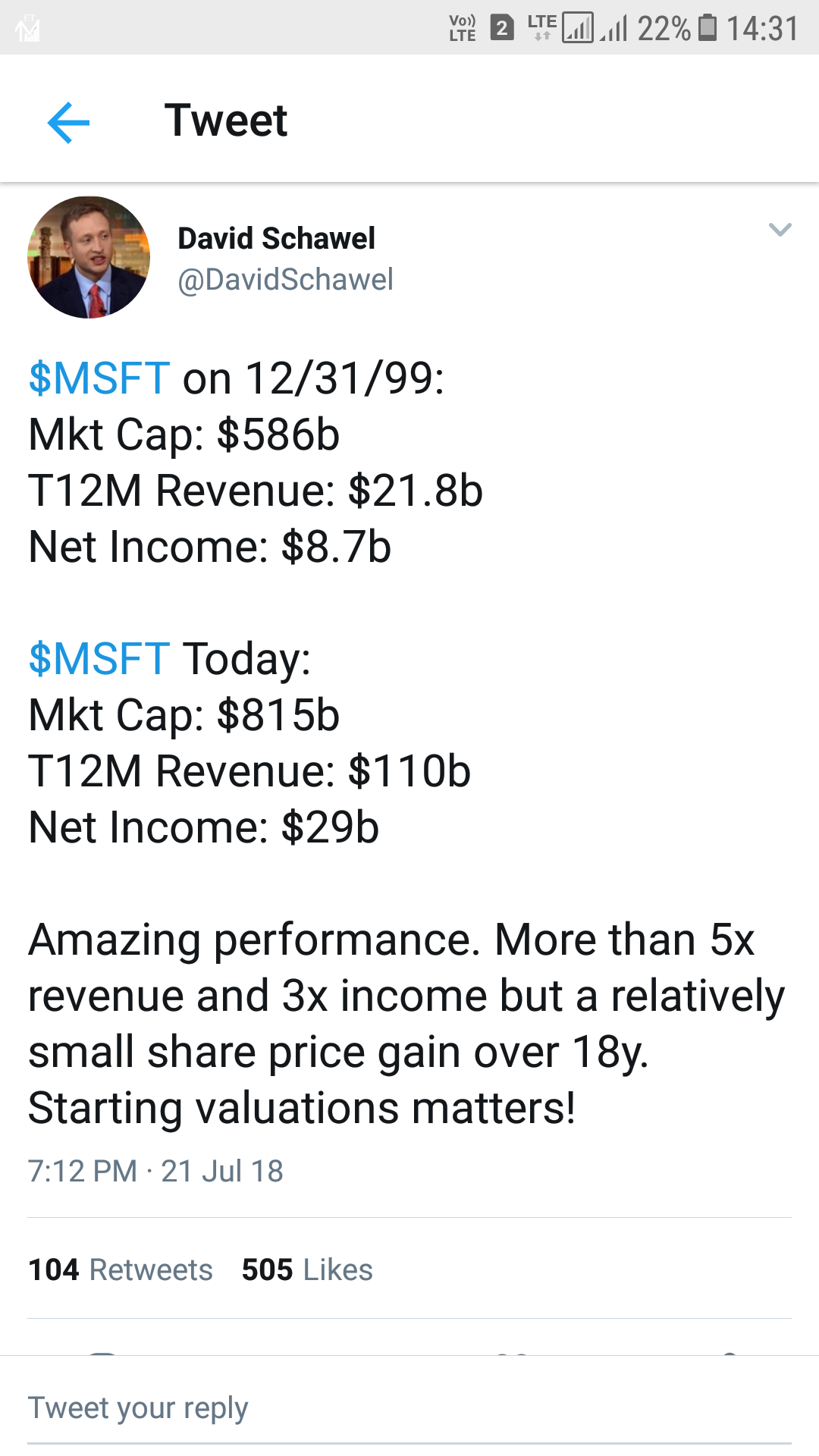

I don’t understand why MSFTs price was taken starting 1999? It was the peak of the dot com bubble. Numbers will tell a different story if you consider the market cap of MSFT just 10 months afterwards i.e around Oct 2000. It was not a bottom. But the euphoria had died down.

It crosses 28 after a period of a very long time today. Euphoria all around. People are rushing to buy HDFC, Maruti, Bajaj fin, Reliance, BOB, SBI, and every other stock they can grab as long term multibaggers. Newspaper front page celebrates record highs. My dhobi has applied for HDFC AMC IPO.

Hinting at anything?

9 Likes