Would you be happy with 1% return on your capital?

Did you see AMFI promoting Mutual Fund products on mass media 5 years back the way they do now?

The economy which has been on the verge of a breakout for last 10 years but never did, isn’t it sitting on potentially the best inflection point in many years?

I feel re-rating is on. The high PE may limit the upside (till earnings growth arrives) but the market would need very strong triggers to turn bearish, and high valuations may just not be enough. I saw several MFs (esp. small & mid cap ones) closing their subscription and sitting on cash in early part of 2017 as they couldn’t find value bets and they were in anticipation of a correction which never arrived. Some of them are repenting as their schemes’ performance dwindled. They corrected themselves and made necessary fund reallocation soon. (for eg. Vinit Sambre - managing DSPBR Micro Cap Fund)

I agree with @Yogesh_s that a very necessary condition for a sharp correction is a sharp upmove where the market peaks out like the tip of a mountain. A 15-20 percent correction cannot be ruled out in any market but for more than that, the market would wait for some tell tale signs.

Contrarion bets (although rewarding) are very risky and a very small percentage succeed. Not many swimmers can swim against the tide in anticipation of the winds changing direction (esp. when you know that there are no better oceans to swim in other than volatile equities). Its good to be flexible in stock market. Being a part of herd mentality gets rewarded with minimal risk. If and when the market turns, good swimmers know how to change course because the are both flexible and they respect the tide.

You have completely missed the point. Why do you expect RoE to be 18.5% when FD rates are falling. Just as a saver shoule be happy to make inflation + 1 or 2%, why should the same not apply to equity owners that they also earn a little over FD rates. Where is it written that RoE should always be 20%? In fact, you will hear many business owners say that why would I do business for 7% returns when I can make that in FD. So if FD rates are down from 7% to 5%, RoE of 10% should make anyone more than happy. And that;s exactly why even with moderate earnings growth and not so great RoE, these multiples are holding.

This business of turning charts upside down is a bit amusing. It can perhaps be an indicator of momentum (steepness of the rise/fall) but one must consider the fact that one end is finite (downside) while the upside is infinite, at least theoretically.

Can you please explain how have I missed the point? In my opinion, this is the point that I am making.

As inflation declines, so do returns - on equity and debt (interest rate). So, we should not compare the return on equity from a high inflation regime with that from a low inflation regime. When we adjust for inflation, there is very little earnings recovery to be expected.

I mentioned about the unrealistic expectation of earnings recovery, the numerator in discounting the Cashflows. That does not mean that inflation does not affect the denominator - discount rate. A decline in inflation will reduce both - the discount rate and the earnings. So, I reiterate that it is not wise to think that the discount rate would remain low but the earnings will recover to the extent that we saw during periods of higher inflation. Hence, the expectation of earnings recovery of ~30% over and above the normal 10% to 12% earnings growth per annum may be unrealistic at the present moment. It appears to me that there is a significant section of the market that is invoking the large expected earnings recovery hypothesis to justify the valuations. So, the realization of very low earnings recovery, whenever it sets in, may affect the valuations.

If we look at what appears to be most rewarding right now and invest, then we may end up investing in the wrong places at the wrong time. I would rather look at how things may play out, that is, a somewhat longer horizon.

Return on capital for what risk? Real returns are related to the risk taken by the investor. Those who do not want to take risks and invest in FD should not compare their returns with the returns on the risky assets class - the equity. They should be happy with a nominal positive real return on capital on a pre-tax basis. It appears that these peculiar FD investors become risk-taking when they see people making money on their risky investments and want to shift from FD to equity. These investors seem to forget that the equity investors go through periods of negative returns while FDs always get paid their fixed coupon. These FD investors could be a good example of investors prone to jealousy / herd mentality.

If I would be unhappy with 1% return on my capital while investing in FDs then I would be terribly unhappy with -2% return on capital. At the cost of being repetitive, I would not follow an investor who invests in a riskfree asset (FD) and is happy with -2% but unhappy with +1% return on capital if others are making money on their risky investments.

I guess that I have been underestimating the power of groupthink. Valupickr is a good place to learn. But, I think that I have been overdoing it. I will try to limit the frequency of my posts on this forum.

Its your perception that people were happy with -2% returns. Probably they were not aware of alternate means or open to the risks of equity investments. But with aggressive MF promotions, people are opening up to it now and with the returns they are getting in MFs,they feel unhappy with 1% returns on fd.

I agree with you on this. It had not crossed my mind. There could be a segment amongst the FD investors who were not informed that they could invest in equity without much inconvenience. I would not call them peculiar. They are just better informed now. I hope that they would be fine with the risks of equity investing and stay the course.

Pardon me for being little upfront but I don’t think any of us are adding further value to debate . I think there are two sides of thought process which has clearly been highlighted and both are sticking to it. One side says you can’t have a recession after 10 years of single digit growth when policy measures have been launched , GDP to market cap looks ok, return on equity is at low , profit margins at at low ,demonetization effect on numbers etc ,so, now because there is a hope before it happened valuations are stretched and if it does not happen that stretch will revert to mean which means a 15-20 percent correction but not recession. The other side is telling look whenever NIFTY has crossed 26-27, it has led to a big sell off and hence we should exit . I think this is pretty clear. This final message is being given in multiple ways. If i am missing any new insight then sorry but I don’t think beyond being rigid , we are going anywhere . Personally, I would be interested to see any data point across the world in last 50 years which violates claim made by 1st group briefly summarized by Yogesh. On 2nd point, the contrary point is whenever PE has gone 26-27 , was it euphoric time or was it a 5-8 years of low growth. If all ,20-30 occurances across world were euphoric times then using the same arguement on situation 1 , I would rather wait to see. At the end, none of groups deny on approx 20 percent correction but the divide is on is it time to sell everything n go home like market will correct 50 percent , Is it time for recession. ? This is my last post for sure as I won’t add any value . I belong to group 1 and expect for a 20 percent correction which would be healthy n make stock picking easier (though every market always gives value opportunity for long time, can’t say if buying would lead to gains in 2-3 years but on a 5 year CAGR basis). Now, would not visit this thread but watch what happens in next 2 years. Right or wrong does not matter, till we are open to learn n time is sometimes best teacher I am really sorry if I have hurt anyone’s sentiments

My Two Bits on Markets. For Last Couple of Years the Macros Were Favourable the Micros ( Corp Earning) unfavourable. Now for the last 6 Months micros showing signs of improvement all across. Corp Debt has stagnated for last 3 years. ROEs beginning to improve. So interesting times where focus would shift from Liquidity to Corporate Earnings.

In my opinion, strategy in this situation should be different for each person depends on his investment plans/goals. For example, my present investments are very less compared to what I plan to invest over next 5-10 years through salary/savings. I would be happy if the market corrects 30% and stay there for 3 years, so that I can get better returns over long term. On the other hand if someone has huge investments compared to his income, the situation is different. If I am in that position I would keep at least 50% cash.

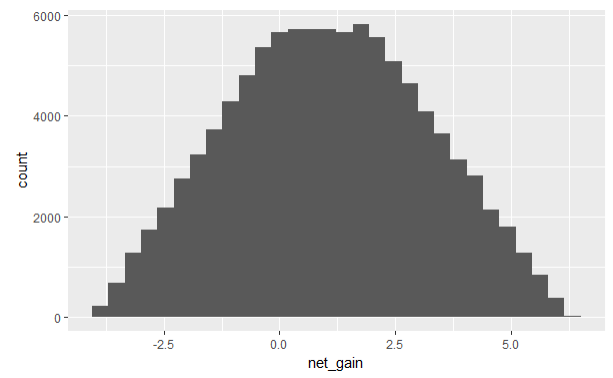

As a purely theoretical exercise, if we were to do a statistical experiment assuming an expected appreciation in the range of (20%,25%) and an expected fall in the range of (15%,20%) over the next year, you get the following:

Mean return is 1.06%

Probability of gaining more than 6% gain is 0.1 % and probability of loss is 33%

Max gain is 6.22% and max loss is 3.98%.

The above is based on 100,000 random values generated in the above range.

Here is the distribution of net gain:

As mentioned in the beginning, it is only a theoretical exercise, and can yield very different results based on the range of gain and loss.

But as the profits are increasing everyday people are adding more and that’s what must be happening in last phase of bubble ,never experienced recession ,and not interested in recession in just 1 year of investing career

Negative interest rates, jobless growth and just the numbers of participants on this thread mean that this may be in the intermediate new normal. We may be the earliest state-sponsored gamblers. So how long can this game go on? Just ask yourself how many times you heard the term “trillion” in the recent past vs even 10 years ago.

For time being the roller coaster has turned to musical chair. Enjoy the music and keep guessing when will the music stop, better have a chair to hang on to.

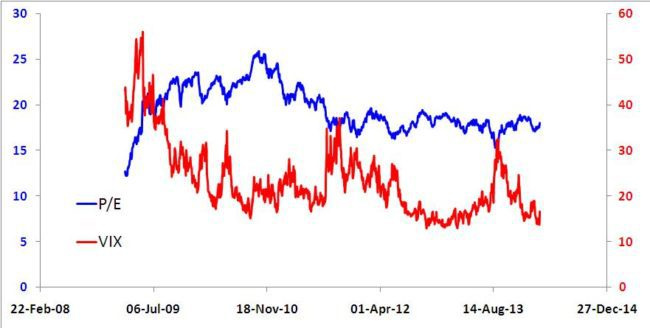

Lets consider this PE and Volatility chart. The volatility in index is seriously not for the less informed. Equity investment comes with a price, you should have substantial amount of time at your disposal to invest in equities. You should be able to research companies, keep track of cycles. I think personally you should have time, intellect, analytical abilities to invest in equities or you can hire adviser (getting a good adviser is not easy either) who do that on your behalf but still you cannot escape volatility. One year the portfolio have x value other year x/y and next year x*z. And then the year when your portfolio falls x percent that year inflation would have reduced it by x-7%

Business cycles are getting shorter and shorter, to keep up to that you need lot of reading. Most people in this forums are looking for multibaggers and have nothing to do with business. They are just trying to catch on the cycles and make money. FD investing comes with peace of mind and mind the fact that inflation arbitrage was not so bad for FD investing until 2008 when things start changing across the world.

As Kumar Saurabh put it my also last post will check this again at End of 2018.

There is talk of taxing LTCG. Last year I distinctly remember the market throwing a hissy fit before the budget just at the thought of that. This year it looks more and more like becoming a reality. If LTCG is moved from 1 year to 3 years, I think average holding period of equity may go up even if there are near-term corrections. Let’s see how it plays out.

I don’t think the LTCG is possible this time due to the upcoming elections in 2019. Surely FM won’t take such decisions before elections. If he does, we can see a healthy correction. IMHO, next year there’s a high possibility of correction and could be a tiny black swan event if BJP loses. Otherwise, the only trigger for bear is earnings disappointment (this is purely my opinion).

I am also a reader of IREF, a forum on real estate. During 2010 till 2013, one thread that had max discussion and constant buzz was RE bubble and correction. And it did happen. 4 years since , I find participants reduced to 1/10. Looks like a barren street in curfew. Also even now discussions range from equity, to politics to music & everything other than RE.

I see similar buzz in this thread, no doubt we are in high valuation, melt up or pre bubble zone. However timing of that is beyond my capability to predict but sooner than later correction seems impending.

I am really sorry if I have hurt anyone’s sentiments

I am really sorry if I have hurt anyone’s sentiments