However, you probably mean that inspite of these expensive valuations when I decide to buy, the market will turn bearish because bear markets start when last bear turns to bull. I hear ya!

Nevertheless, it would be a pity if I forget about how important the buying price is for success as a long term investor. Abysmally pitiful, I’d say.

When facts change , I change opinion . But still not here to bore but just adding some latest data of last 30 days to substantiate the fight between hope and reality . One by one , all leading indicators of economy improving . However, they are not all numbers and this is just one month of data. Need more indicators with more months of data to stabilish n fuel continuation of hope and ultimately all this has to turn into EPS . However, with points highlighted by group 1 accroding to previous post of mine , I would stick with growth or stagnation but not a downfall in EPS which reitrates same thing . 10-20 percent correction healthy. But of before pessimism takes over, if optimism turns into reality , who knows . So, still avoiding completely timing market n going beyond 20 percent cash with a hope to ve 15-20 percent healthy correction for easy pickings. Now, tracking leading indicators of economy is critical for next few months

On the other side rising interest rate, crude price, inflation and eidening fiscal deficit are concerns which market is giving a pass due to bullish sentiment and sooner or later they will have an impact

Judging by the plethora of similar posts, this thread runs the risk of becoming increasingly bi-polar, isn’t it? Felt tempted to introduce some fresh thoughts

What I have learnt over the last 7-8 years, Investing is NOT a science, its an ART form. Each time patterns may be similar, but are also contextually different - to place that context into perspective is very important. E.g. No single input is a sufficient condition - its important not to get fixated on any one view. Not to choose extreme positions. Try and position oneself slightly flexibly. For bull market peaks, many things have to happen together, isn’t it. But as always, there are a few conditions that move the needle the most - senior practitioners like to remain extremely alert to these.

Here’s what our senior pros feel about the stage of our markets currently. Copying the gist form my recent post in the Portfolio Restructuring thread

Good to always consult folks who have endured at least 2-3 bull market peaks/secular crashes, before hardening informed positions. I always do (I remember only 2008 and my helpless condition, then!)

Donald , saw your post in other thread on current marketing sentiment. I think some of views in this thread and your thread ,more or less seems to be inline.

Yup. Just thought to highlight the 3 pre-conditions for bubble peaks as Seniors read it. That perspective was important to include in decision modeling.

How much I am going to lose in terms of percentage of my portfolio in crash/recession/bear market

Suppose its 75% loss

Then if I invest 100 Rs in bull market and my pf becomes 3x = 300 and then 75% loss means in hand I will have 75rs

So even I make 3x my pf will be minus 25%

So need to make an least 4x ie 400 Rs for break even

Or I need to make more than 4x or more than 400 to get in profitable position after the crash

You never lose 75% overnight. Keep your loss limited to say 25% and exit markets completely when it hits 25% mark. In this way, even if you make 1.5 times in your bull market, you would end up with having better returns than FD.

The point of this discussion is not if you should completely exit. The point is that new entrants should not invest now in the markets. And that the old portfolio holders may reconsider booking some profits.

I read a thread on a possible melt up & subsequent crash. I with due permission want to copy & share the post in this thread as its quite relevant to this thread. @ kashif_1461…Hope you don’t mind sharing your post

Author has analysed previous bubbles and noticed that an acceleration of index by approx 60% in 21 months prevails before a hard crash landing. Which in sensex terms means approx 41000 by later half of 2018.

In this article, Mr. Grantham first starts by pointing out the elevated levels of US stock markets. Whatever parameters you use, there is no denying the fact that markets are exceptionally high at this stage and have been for some time now. In fact Jeremy Grantham is not the first investor to warn about the exceptionally high levels of the stock indexes. Many other equally distinguished investors have been sounding the alarm as well. Howard Marks also sounded the alarm about the elevated risk levels and gave his advice to be cautious going ahead in his quarterly memo – There they go again… again9. Some other very distinguished investors like Seth Klarman, Paul Singer, John Hussman, Bill Gross etc. have been quite outspoken about the risks in todays economy including the policies of central bankers around the world, China, Trump, etc.

But does the high levels of the stock market suggests that we are in a bubble which is going to burst? In the article referred to above, Jeremy Grantham explains that – “Price alone seems to me now to be by no means a sufficient sign of an impending bubble break.” Stock market bubbles are characterized by exceptionally high prices alongside signs of excesses and euphoria among the market participants. Many experts including Howard Marks, Jeremy Granthan and Robert Shiller agree that although while the current prices are high but the current stock market rally lacks the psychological, touchy feely elements of euphoria. Hence, we are not yet in the bubble territory although there are early signs that the bubble is beginning to form. One of the most important indicator of the euphoria and the resulting formation of bubble apart from price is “acceleration of price.” This has been observed in each of the previous bubbles wherein there is a final acceleration of price which takes the index to levels of ~60% higher within an average time of 21 months. And we can see early signs of this acceleration of price and hence formation of the bubble.

Other than acceleration, there are two other historically reliable indicators of the formation of the bubble. These are: - Concentration and Outperformance of quality and low beta stocks. These are related – concentration refers to the obsession of the investors with a few stocks such as Nifty50 in the 1960s, and Cisco and Microsoft in 1999 and FANGs in the current period. The second factor is pretty much self-explanatory.

The current rally in stock markets in India has been going on for a long time now. As a result, the valuations have become stretched and most of the stocks of quality companies are trading at exceptionally high valuations. The retail investors have poured back into stocks after getting hurt and staying out of the markets after the 2008 crash. All this has made the value investors very nervous and rightfully so. But as we have seen overvaluation is not the only trigger for a crash. For a bubble to burst, it has to form first. And in India as well, the bubble has not fully formed yet because we have yet not seen the second most reliable indicator of the bubble – acceleration. The Sensex has gone up by ~28% during calendar year 2017. While it increased by 16% during the first half, the growth decelerated to 10% during the second half of the year.

The current rally started in December 2016 and has been going on more or less uninterrupted for the whole of last year. Just to get a flavor of where we can go from here. As we saw, historically the price has increased by an average of 60% over the last 21 months in the previous bubbles. We already had an increase of 28% during the last 12 months in Sensex. Which means that the price should increase by another 25% during the next 9 months. This will take the Sensex to 41,600 by September 2018. We can construct various scenarios but the bottom line is this – we should see a final acceleration starting soon for a bubble to form.

Except for crappy stocks, all stocks that fell 50-60-70% in 2008 recovered in a year or two so I don’t see how you can make that devastating 70-80% loss. You are confused between risk and volatility.

Thanks @Donald for this intervention. I think this thread was going nowhere. You have rightly said that it is important not to get fixated on one view but remain flexible.

No two bull markets are the same, nor will two crashes be the same either. My policy is always to hope for the best, but be prepared for the worst.

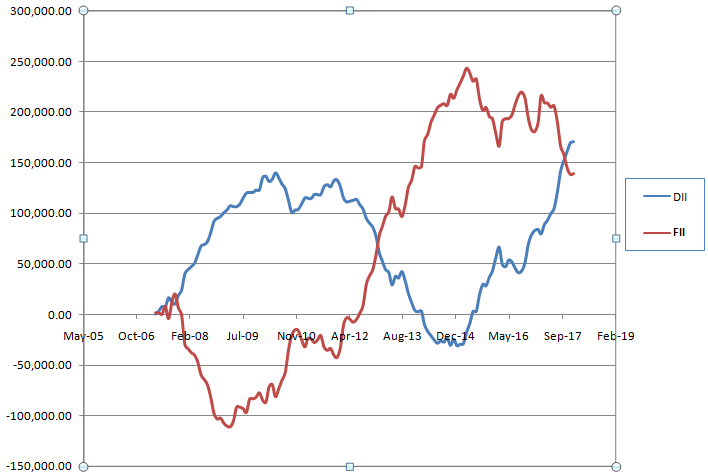

Due to the following reasons, the retail Stock Market investors (DII) are in for a perfect storm.

Liquidity, Sentiment and Fundamentals, as rightly said, are the base of any rally. Allow me to provide my view on each.

Liquidity:

USA has made clear her intentions to absorb liquidity back into the US economy from world over, and this figure is touted to be, not in paltry millions or billions, but in trillions.

Therefore, FIIs are net sellers and are hence in need for enthused buyers who are blinded enough by greed to suspense all logic and continue the buying spree even at highest valuations.

Source:

In summary,

FII activity in 2017 -44,108.85

FII activity in 2016 -14,356.01

FII activity in 2015 -20,373.69

FED is increasing the interest rates and hence their corporations need to plough their dollars out from our markets and into their stocks and bonds. If they do it haphazardly, they are only going to get a few cents on a dollar. So they have to be strategic about it. They have to set-up a solid buyer to absorb their trillions. A fund house or two wont cut it, they need an entire nation to participate in the madness. Here come in the innocent lambs, the sentimental beings: The DIIs.

Sentiment

DII is a sentimental herd. They leave the dreary job of research and study of fundamentals to the professionals. Hence, we see DII recklessly buying, left right and center, at current ungodly valuations.

All thanks to the media, the sentiment is made and maintained bullish. Modi government coming in with its promises also helps. Modiji is the new face of “Vikas”. He will get there, but it will take a good part of the decade.

I believe, when the purpose is sufficiently served, when the FIIs have sold a meaningful quantity, they will pull the plug on their payments to the media and let nature take its own course.

Consequently, without the Media fed dosage of news of bullishness, within a week the retailers will be falling on each other on the way out, causing lower circuits day after day. Cuz when DII turn sellers, there will be no buyers.

In conclusion, I think Liquidity and Sentiment are the same thing. Once sentiment turns, liquidity will too.

Fundamentals

Fundamentals are downright poor. No doubt about that either.

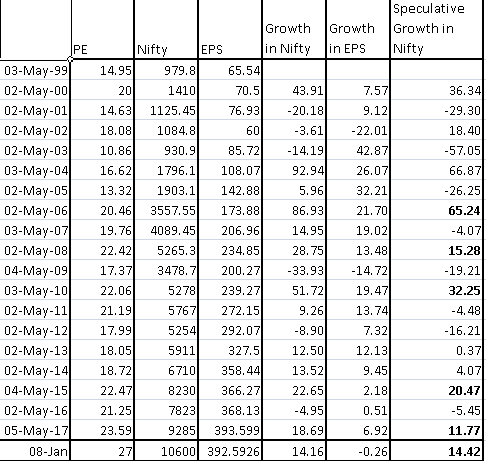

In last six month the EPS growth of Nifty 50 has been a negative. It may improve but not substantially and anytime soon. To make matters worse, Crude prices and GST are not helping.

Finally, we are left with nothing substantial to depend on for supporting the market. Liquidity and sentiment are two sides of the same coin, which is in the pocket of the media, which surely gets paid handsomely to dedicate their expensive air time to bullish news. Once the purpose is served, they will turn. With poor fundamentals and absence of FII led buying, things are likely to get from bad to worse very quickly.

PS: I will continue to bitterly cry “Bear” until I too get paid.

But still not here to bore but just adding some latest data of last 30 days to substantiate the fight between hope and reality . One by one , all leading indicators of economy improving . However, they are not all numbers and this is just one month of data. Need more indicators with more months of data to stabilish n fuel continuation of hope and ultimately all this has to turn into EPS . However, with points highlighted by group 1 accroding to previous post of mine , I would stick with growth or stagnation but not a downfall in EPS which reitrates same thing . 10-20 percent correction healthy. But of before pessimism takes over, if optimism turns into reality , who knows . So, still avoiding completely timing market n going beyond 20 percent cash with a hope to ve 15-20 percent healthy correction for easy pickings. Now, tracking leading indicators of economy is critical for next few months

But still not here to bore but just adding some latest data of last 30 days to substantiate the fight between hope and reality . One by one , all leading indicators of economy improving . However, they are not all numbers and this is just one month of data. Need more indicators with more months of data to stabilish n fuel continuation of hope and ultimately all this has to turn into EPS . However, with points highlighted by group 1 accroding to previous post of mine , I would stick with growth or stagnation but not a downfall in EPS which reitrates same thing . 10-20 percent correction healthy. But of before pessimism takes over, if optimism turns into reality , who knows . So, still avoiding completely timing market n going beyond 20 percent cash with a hope to ve 15-20 percent healthy correction for easy pickings. Now, tracking leading indicators of economy is critical for next few months