I attended the concall (missed the last part though due to disconnection), my rough notes:

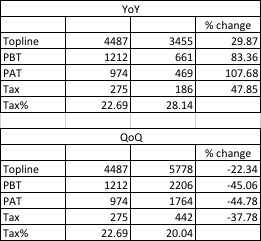

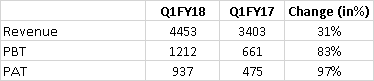

Consolidated revenue 448 (30% growth)

NPAT - 93.7(97% growth)

EPS - 5.58

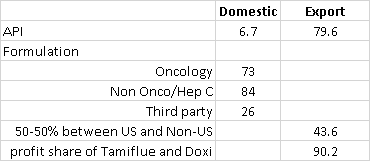

Segments API - total 86 cr, domestic 6.7 and exports 79 cr

Formulations - Domestic 182 cr(oncology 73 cr, branded 84, 3rd party 24 cr)

Exports - 43.6 and 133 cr (Tamiflu 72 cr, Doxil 8.5 cr minimal sales, next quarter will be more meaningful) other exports 43 crores

question/answers

Copaxone - management still tight lipped, expecting an outcome this FY

Domestic - few niche launches and many first generics

R&D spend 6-6.5% of sales (more India focussed than US)

Tamiflu suspension - no other filers so far

Hep C - 100 crore revenue in India (price erosion stabilised, consolidation of competitiors, only 4 firms now competing, sales approx 40 crores/month)

Hep C exports 3.7 crores, sale in 12 countries, approval sought in total 30 countries

Debt - 156 crores, Cash 209 crores

Capex for this year in India - 400 crores, 86 crores spent so far (India focussed)

ANDA - will be selective from now on, focus on profitable products, aim 4-5 filings this year

American business very competitive, several players. Hence focus will be on India and other markets such as canada, brazil, singapore and philippines

Oncology growth > Hep C

Azacitidine will be launched this year in US, not expecting much profit since many players already present

Pomalidomide - 18 crores sale or profit in India, doing well

15-20 niche launches in India this year.

Disconnected…