@nasarma - yes its correct that there was a mention of gOseltamivir suspension filling. In fact, the patent + pediatric exclusivity expired for 6 mg on Feb 2017 and for 12 mg will end on June 2017.

However, as we know, Influenza has a strong seasonality component involved. This years Flu season is over in state side and for next year flue season who all will be competing can be a guess work to the best. In fact NESHER has already got approval on tablets.

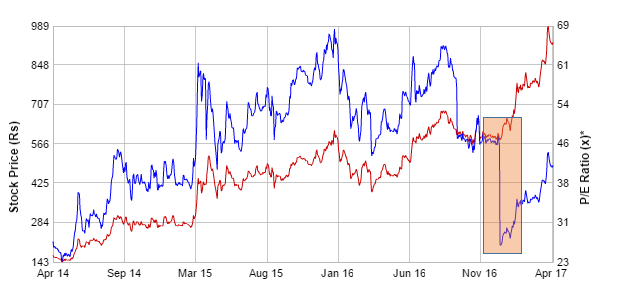

My reference to the lower PE is for the fact that Q3 improved earning had this one time OR one season per year earning component. Spreading across this to full year financials, the EPS will not sustain this high (unless other opportunities start kicking-in - which btw is a possibility). Thats why I used the word ‘optical low PE’

Please see the attached chat, prices are driving crazy since this seemingly low PE started appearing on charts.

If you really want to track it, then key watchable are:

Sofosbuvir+Ledipasvir growth in India and ROW. in India they are now in almost pole position. Spreading to Rest of the word (they mentioned Egypt as second biggest HepC market) and couple of other European offices came up recently.

near future launch (indicated in above post) in US.

retaining expending ~30% market share in targeted Onco therapies.

Thanks Tarun. Your pointers on key watchable are useful. I was waiting for an entry point for long and took the plunge with an initial position when I noticed the PE drop.

They have mentioned that Credit Suisse had expected Momenta Sandoz to be the first to launch a generic Copaxone. However, because of FDA observations at the Pfizer facility which is involved in manufacture of Copaxone for Momenta, the launch is now definitely delayed, like we already discussed above. Pfizer is working on the observations, but will need some time. This article states that now because of this, Mylan may the forerunner to launch the gCopaxone, if it manages to get approval for it.

So I guess, next few months will be interesting to watch what happens next, in the Copaxone race.

In yet another move to strengthen market dominance in thriving Hep C, Natco has launched another version of sofosbuvir 400 mg +velpatasvir 100 by the name of velpanet. If I recall correctly, few days back this same velpanet was launched in Nepal.

@T11, you are correct, Velpanat was launched some time back in Nepal.

Since there is a lot of competition, let’s see how it unfolds. Natco will definitely have a pricing advantage.

Gilead has licensed it to more than 20 companies in India, for distribution to about 101 developing nations:

CIpla and Cadila have already launched some combination a year ago. There are various combinations of Sofosbuvir; I haven’t gone into details about them, but this present one which Natco launched is one of the more popular combinations.

Also, here I wish to state that, Hepatitis C is being increasingly more diagnosed, but within next 5 to 7 years, we may see a fair slow down in numbers of new cases coming. This is because, most of those cases being diagnosed now are the ones who may have got infected many years ago and now coming into view, due to symptom. Because of increased understanding and screening methods, Hepatitis C transmission will slowly fall and over time, lesser cases will be diagnosed, once next five to ten years are gone. So the maximum money that is to be made from Hepatitis C would be next several years. (To make readers understand, Hepatitis C is unlike cancer which is rising like a wild fire and we can only see a massive rise over next decade, and scope of cancer drugs will only keep rising till humans are alive).

Pomalidomide is an oral agent, used in treatment of Multiple Myeloma. It’s brother - Lenalidomide (Revlimid) - is one of the first line therapy. When it fails, Pomalidomide is used. Tarun (@T11) has given a wonderful analysis of Revlimid, for those who want to read on its potential. One can also read the following article to have an idea of the market share of this drug. As of now, Natco is the only one licensed for India.

Notes from Mylan Concall yesterday (10th May, 2017):

Turning to Copaxone, we have a target action date for both the 20-milligram and 40-milligram for next month. We see no reason that these dates cannot be met. We believe that all scientific questions have been resolved to FDA satisfaction and we also believe that there are no facility GMP issues that should be a barrier to approval of this ANDA.

And one more:

Question: And on Copaxone, just describe your readiness to launch that product, both the 20-milligram and the 40-milligram, if you actually get the approval at the action date next month.

Rajiv Malik - Mylan NV: So let me take the easy one first, which is Copaxone, and just talk about our readiness. Yes, you will expect us to be in a state of readiness from the manufacturing point of view – from commercial manufacturing point of view in anticipation of the target action dates.

Pomalidomide is going to provide a decent and growing earning stream for Natco. Almost equivalent to lenalidomide in efficacy but usually reserved until after lenalidomide failure in myeloma patients.

Another legal development (adverse) on Natco’s aspiration for gNexavar (Sorafenib Tosylate):

Backgound: Back in 2012, Natco was able to secure first and only Compulsory licence so far in India pharma sector from Bayer. The medicine was for the kidney cancer treatment drug Nexavar (Sorafenib Tosylate). Natcos challenging stance was on the fact that Bayer was artificial keeping the medicine beyond reach by way of unreasonable pricing. This compulsory licencing enabled Natco to launch generic Nexavar in Indian market at ~3% of the price offered by Bayer.

On a side note, what I also gather is that this revolutionary Compulsory Licencing concept met with a defiant nip in the bud approach by way of heavy handed lobbying and decline to launch second generation (improvised) drugs (in some cases) in India market by powerful Pharma group.

Current Development: The battle is far from over between Bayer and Natco. Natco intends to have its ground work (clinical study, data dossier etc.) ready for generic launch of gNexavar outside India as well, upon expiry of exclusivity (Nov/2020). For the filling purpose they need to carry out global experiments. Natco was exporting the API Ingredient/doses of sorafenib tosylate to China to run bioequivalence and bioavailability studies (to prove their product is similar to the innovator product) for regulatory approval in China. However, since 2014 Natco and Bayer are in legal tangle to establish if Natco has right to export APIs/finished doses outside or carry out clinical trials outside India under the purview of compulsory licence…

Delhi High court issued a verdict in March 2017 in favor of Natco under section 107A establishing that export of API for the purpose of clinical study/experiment is non infringement.

However, yesterday another Delhi HC bench revisited this matter again upon appeal by Bayer and have put the API/formulation export by Natco on hold till September. Bayers objection is based on the argument that Natco is exporting finished doses not the APIs.

Two key statements from the media coverage:

The bench said there was “a world of difference” between exporting for licence approvals, as claimed by Natco, and exporting for commercial purposes.

“What you cannot do directly, you cannot do indirectly,” the bench said.

Silver line here is that within yesterdays verdict, Delhi HC has indicated that company need to file separate applications for experimentation purpose and for licence application purpose. And approval can be considered for a specified quantity and for specified purpose only.

Dont see much of an immediate material impact for Natco. Appears to be more of technical/regulatory issues towards future launch prospects.

Innovator: Innovator for the RLD is JANSSEN RESEARCH LLC Market size: As per IMS TTM sales for brand and generic was ~$200 M. Competition: Limited competition. Back in 2012 SUN got a compulsory licence for Lipodox due to acute shortage of approved drug. This was a stop-gap arrangement. Not sure if this is in force as of date. Else this will be just two player market between innovator and DRL+ Natco.

I found this an excellent read on Dioxil. The above being its generic version approval. Its a bit old but gives growth prospects. Apologies if someone has already posted it

I attended the con call. My rough notes as follows:

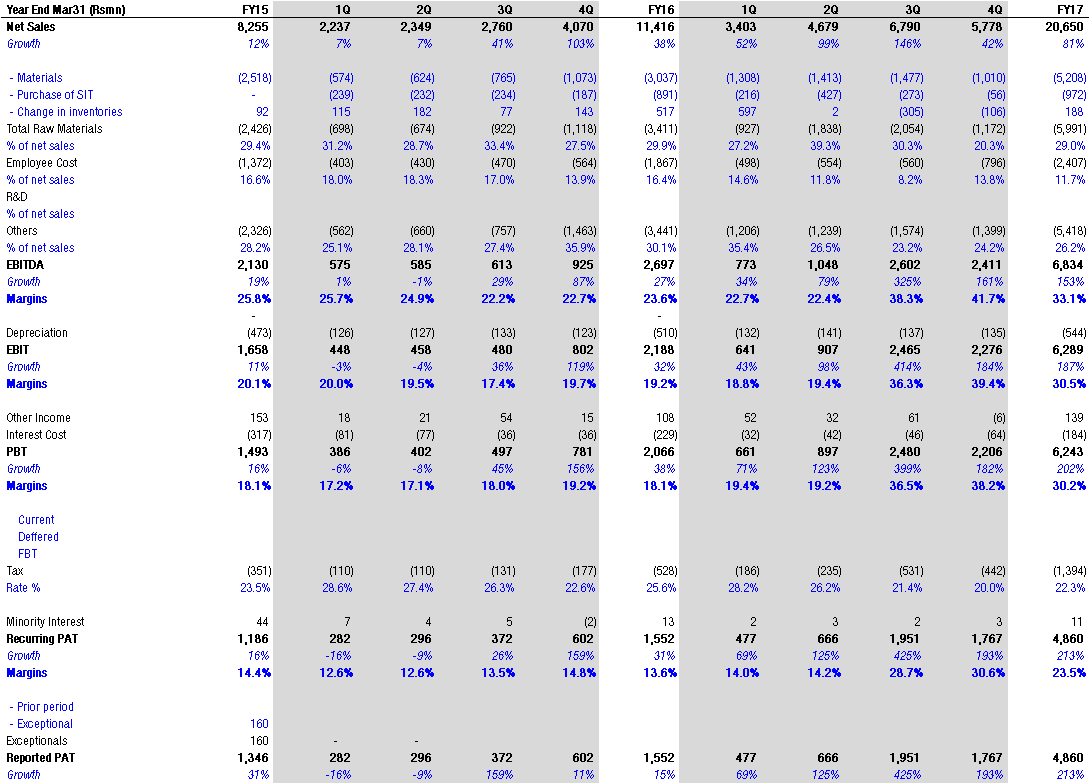

Tamiflu revenue - 705 crores

Profit from tamiflu - 412 crores (management expects the profit from Tamiflu next year to be 50 crores, variables are fresh filings and tamiflu syrup sales, competition difficult to predict). Management expectation from Tamiflu is low but…)

Copaxone - management said they can’t comment because of agreement with Mylan - big opportunity 4 billion market.

Regarding american generic business - they said competition is tough and company has got out of certain contracts and booked loss due to competition. Profitable growth is what they are looking for. R&D expenses will be more towards India (from current US 60% and India 40%). R&D spend was 123 crores last year

Management was bullish on India, growth in India expected to be 20% in the medium term, 7-10% from fresh filings and 7-10% from existing products

Hep C sales in India 510 crores approx (240 crores last year) - forecast is 20% growth

Onco sales in India 330 crores

50% of drug portfolio in India come under price control, but despite price control drugs are profitable

Focussing on Onco, Gastro, Cardio and diabetes (last 2 new launches - there was nothing much said about this aspect of business)

Forecast provided by the management is Revenues 1700-1900 crores and profit 400-420 crores (excluding new launches!)

Natco paid a bonus (one month salary) to the staff last year. ESOP of 133000 shares (non cash)

Capex of 350 crores this year

R&D of 123 crores (next year almost same).

Good summary @stockcollector. I also attended the call. Will summarize my notes in some time. Few top of the head:

They are considering base business (excluding Tamiflu, copaxone etc) projection at 1700 Cr and guidance of 20% growth by conservative estimates for FY18…

Other projects will add to top line however not be included in base business at this moment for all prudent reasons.

gOseltamivir to be looked at a one time opportunity for the time being. Will depend on new players coming in by next flue season.

Glatimer Acitate (Copaxone) - PTAP hearing scheduled for June. VERY VERY tight liped and candidly refused to answer. Whatever analyst could extract was…20 MG and 40 MG approval in a shorter span of time is possible, Sandoz/Pfizar has approval for 20 however in middle of regulatory issues. DRL also in race, so the market need to shape up. Evidently move will depend on Mylan’s discretion.

5.Expected to have ~50 Cr added to bottom line from Doxil (Lipsomal). Sun is also there. J&J were discontinued for some time. Coming back. Still limited competition.

Some extraordinary expenses/write-off took place this fiscal (since had windfall cash from Oseltamivir). a) Venezuela write off ( this was explained in Q3 call as well), b) penalty payment for exiting some contracts where management felt prudent to get out due to changed business rational and c) 1 month special bonus to employees. Personally, liked the aspects of sub points b and c above.

Capex of ~350 Cr (i need to verify this number). New line to be added for tables at Guwahati and Utrakahand units.

One lady from ShareKhan had question around NEML and impact thereof for Natco. Sofosbuvir falls under NEML list. Also, broadly 50% of domestic business falls under NEML however thats non issue for management. Per them, Natco is always known to price the drugs very competitively. Any new addition to the NEML list ( since they are into Onco, Diabetic etc.) may be a non-even, per management commentary.

Hepatitis C - outside India they are also expending to certain new regions. Viatnam is one of those, few other names were mentioned. combination drug Sofosbuvir+Ledipasvir, and Daclatasvirin has made things interesting since now patent will prefer single doses instead of having two tablets separately. Approx treatment cost is ~18K per month for three months.

@stockcollector - Thank you for your quick summary. I think they mentioned some exact date for Copaxone PTEB hearing, I missed due to poor audio. were you able to get the exact date? They mentioned something about gTracleer (Bosentan) and gEntocart as well. I missed to capture that. Do you recall?

These were few top of the head things that I was able to capture while doing multi tasking. I will get back after referring my notes, there were few interesting numbers (domestic segment wise), Global base business + addition etc.

@T11@stockcollector

Thanks for the detailed updates from the con call. I could hear only a small part of it, as was busy with a commitment. They usually upload the transcript on their website within a couple of days. Looking forward to read that in detail and then maybe have a discussion here.

As for Copaxone, I have been trying to gather as much info as I can. Of what I know is, the earliest to file would have been Momenta. But because of USFDA observation at the Pfizer facility, Momenta is presently out of the race and most analysts feel it may take up to 6 months to clear those observations. The closest to finishing line now is Mylan, if it gets FDA clearance as well. From Mylan concall transcripts earlier this month, they did seem confident of the FDA approval, saying all things are in place; but of course, let’s see what happens. Also, one more point is, a few brokerages have upgraded Mylan saying, it has a good chance of getting Copaxone approval. Me and Tarun are trying to locate the date of PTAB hearing from the official website and will update if we get any info.

I am looking forward to dissecting a little more after I read the concall transcript.

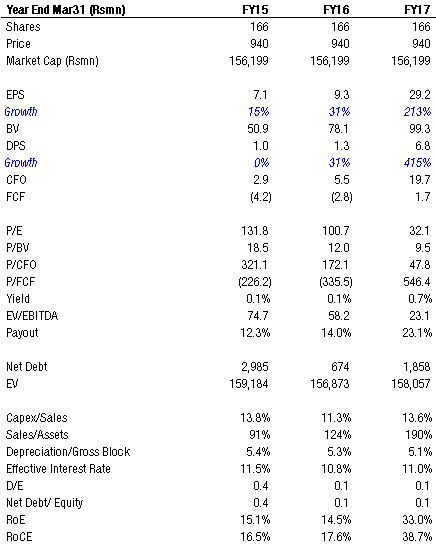

Asset side of the balance sheet consist of too many fixed assets and ever increasing capital work in progress. I wonder what they are capitalizing for so long?

Sharp jump in receivables, unusual for a company with an exclusivity.

Cash and investments are too little for a company with long record of profitability.

Assuming Tamiflu is one time exclusivity windfall, ROE is low. This is perhaps the biggest warning sign.

Operating cashflow is consistently lower than net profits. Given the sharp rise in receivables (and a drop in payables) operating cashflow will be low this year too despite a windfall gains.

Huge capex over several years. This funded by financing cashflow because of poor operating cashflow.

financing cashflow is mainly from issue of shares thus regular dilution of equity holders. If even a windfall gain could not improve cashflows then what can?

My suggestion is to get hold of a ICICI direct report published on 01st June. Great read on NATCO. I am not sure if it is allowed to put research on public website -hence not doing so. This is from ICICI direct

According to an US broker -expects gCopaxone launch in June from Mylan. The others who have filed for 40mg applications , as you are aware are , Amneal , Biocon/Apotex , Dr.Reddy , Synthon (in partnership with Pfizer) & Sandoz/Momenta (delayed as you have mentioned).

They expect gAdvair from Mylan around Mid 2018.