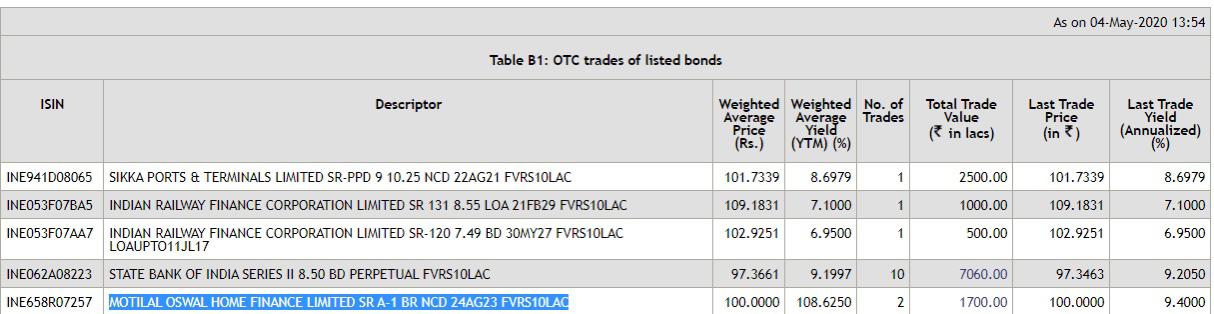

Motilal Oswal Home Finance’s Bons yesterday traded at YTM of 106% which indicates extremely grave problems for the company

2 Likes

That is completely ridiculous and desperation of high order. MOSL has enough cash and they are deploying in buy back as well. Even their NBFC is not growing the book at this time so they might not need fresh cash. This is mostly about lack of liquidity and risk aversion in the bond market which makes it difficult to evaluate risk of individual debt securities looking at ‘spread’ as the only factor.

How does the upfront fees in MF compare to the trail (even if industry has moved to trail fees model)

I wanted to understand even if Net inflows are same how does the mix of Gross inflows and outflows from the existing book impact the commissions payments. Suppose gross inflow is 100k and outflow is 75k v/s a 30k gross inflow and a 5k outflow; in both cases the Net inflow is same 25k but the dynamics of commissions would differ, right?

And I’m assuming this differential that would a smaller part in Motilal’s as compared to HDFC’s as later would have a older/legacy book where redemption can come from as compared to Motilal.

Or is the difference so small (in overall state of play) that it’s not worth thinking out this point.

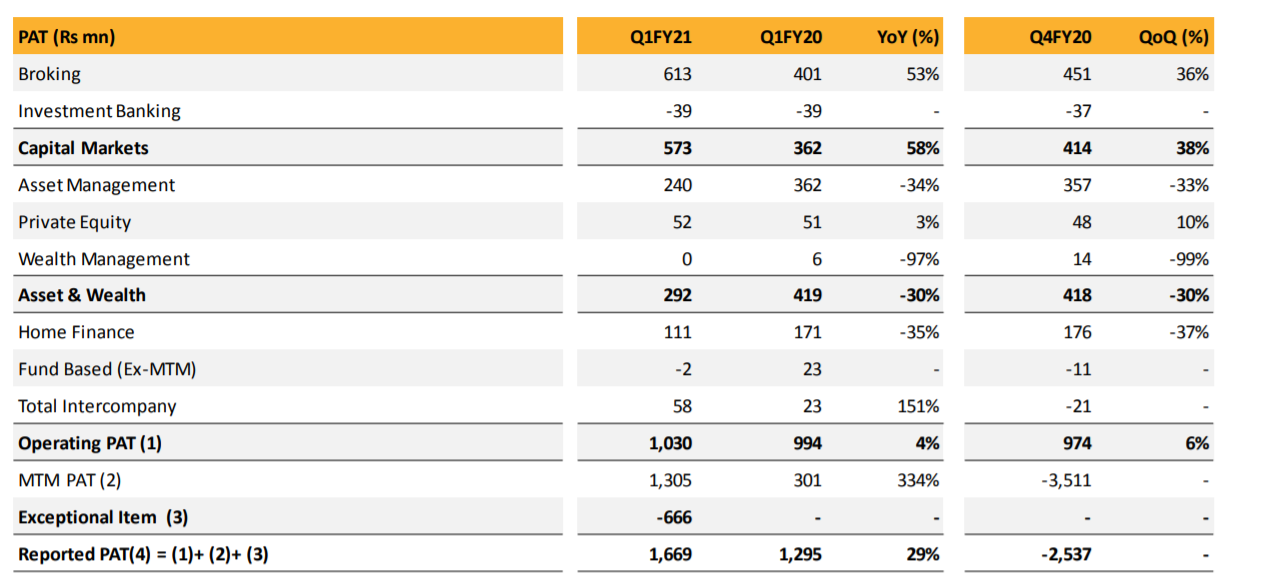

Overall decent results. As expected Broking business outperformed and Asset Management underperformed. Home Finance was understandably muted with disbursements of only Rs. 238 mn during the quarter. How diversification into segments (specially capital markets and wealth) reduces the volatility/cyclicality in performance is beautifully evident in the results. With brokers like ICICI Securities, 9 Paisa etc are doing great in the current market, AMCs like Nippon and HDFC are trading at close to 52-week lows. Funnily, MOFS is trading at almost the average of 52-week low and high. This makes MOFS better from investment perspective, rather than trading.

Disclosure: Invested in MOFS

Regards

SJ

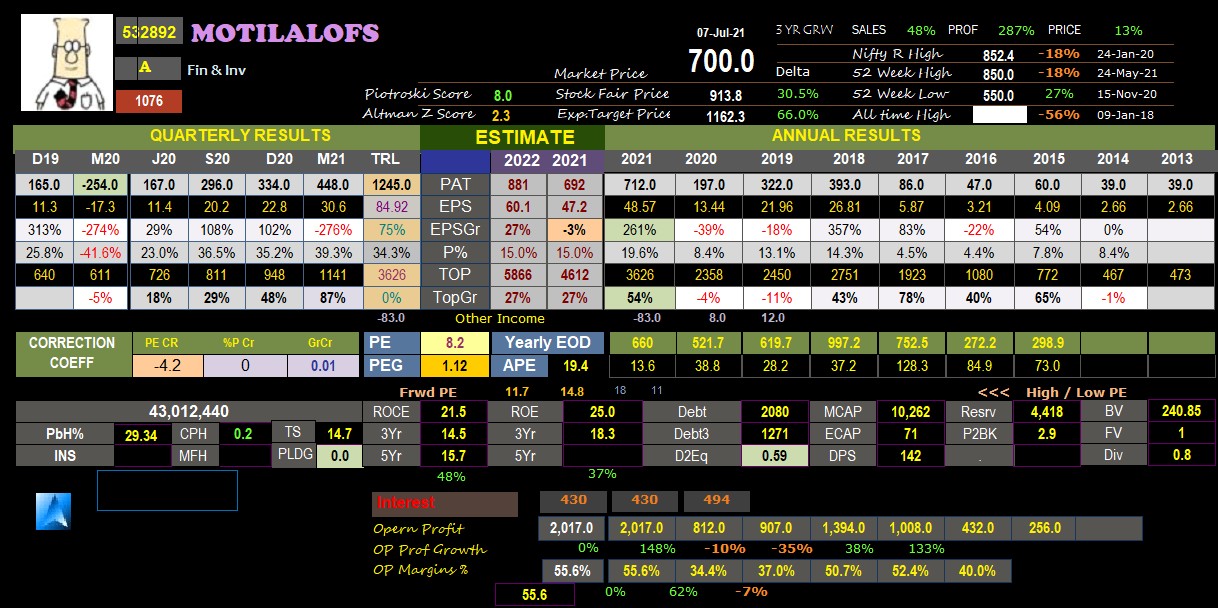

Results are out and there is multifold improvement in EPS

2 Likes

Q3 Net Profit at Rs. 333.87 crore in December 2020 up 101.81% from Rs. 165.44 crore in December 2019.

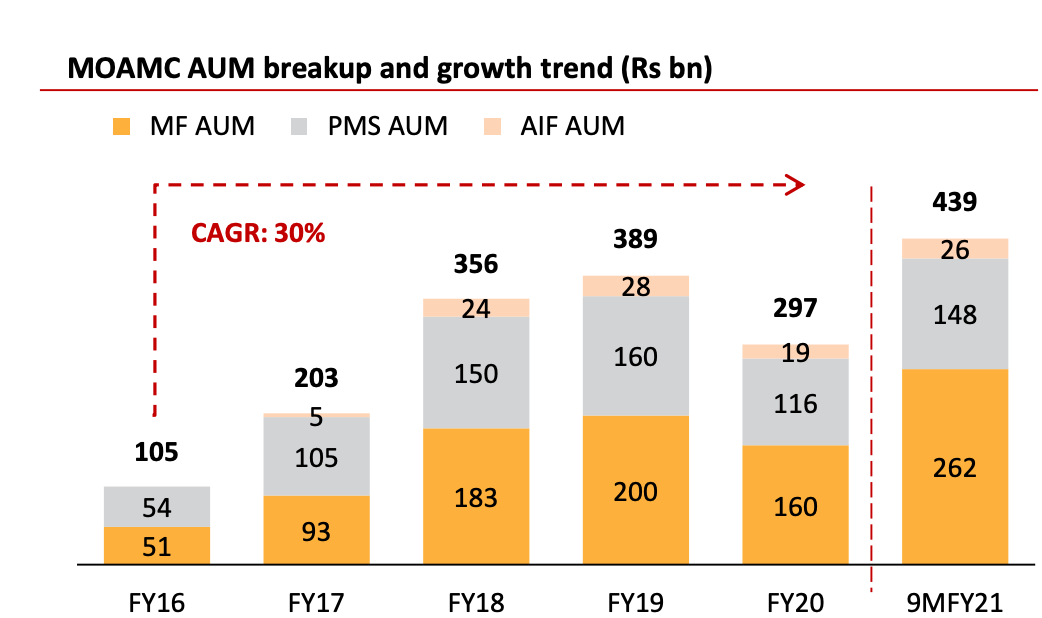

MOSL’s AMC business is what had got me interested in it a few years ago. The business has two verticals - MF and PMS/AIF. While the MF has done quite well to build its AUM (up 30% over FY19), underperformance of their flagship PMS schemes has dented their brand with HNIs. The PMS/AIF AUM is flat since FY2019 even as Nifty is up 20%. Clearly HNI money has gone chasing better returns with the launch of several new players like Marcellus. Building back their reputation is going to require at least 3 years of alpha generation during which time both growth and margins will be muted for the AMC business.

The MF has also been an average performer - slighty lagging the benchmarks - but the strength of the brand has enabled them to attract AUM even without outperformance.

The stellar performance of the broking business as well as the profits from their proprietary investments have offset the poor performance of the PMS business.

Disc: Invested

6 Likes

What’s your view on their home finance business? Is it out of the woods or has worsened now because of covid situation?

Linking technical view shared on another thread…

1 Like

Looks like the current run in the markets as well as increased time with people working at home has drastically increased market activity.

Motilal Oswal’s last results were a good indication of this - even if we don’t consider gains in investment portfolio - the growth in consumer base, revenues and profits from brokerage were very encouraging. This period could very well be a pivot for increased market activity in India - with people having so much time to research stocks, understand basics and learning being easily available on excellent online forums and some good YouTube channels.

I do understand the excitement about discount brokerages, but conversations with extended family and friends usually reveal how ‘safety’ and ‘brand’ is equally important. So I am a full believer in the potential of a Zerodha, but it does not mean a Motilal or a Sharekhan is going to suffer. With our savings rate and participation levels, the story is probably just starting for these guys too.

Motilals offerings in the PMS, booking and AMC businesses are strong - as well as they have reputable well recognised promoters - and they understand the markets and marketing - I feel their ads on business channels as well as thier offerings (Nasdaq ETF) for example - get the gyst of the consumer mindset well.

Scuttlebutt for the industry was relatively easy to do - just had to speak to a few brokers - not even Motilal. Trading activity has really risen, with several new customer additions, and also several ‘dormant’ customers being active. The recent run has ensured these people are also relatively confident and richer than they were a year back. Should reflect positively for an integrated financial services player - be it selling PMS, mutual funds or broking.

Discl : Invested from lower levels, added recently, might add more if story continues to play out

2 Likes

Further scuttlebutt with a few brokers

- Trading volumes continue to be at highs for the industry this quarter

- New account openings continue with strong inflows into MFs, Equity and PMS

- Previously dormant accounts continue to be active with renewed interest in the markets

Looks like Q1 results (April to June) could again be a large positive - especially over a largely subdued base of last year.

Question remains on how long euphoria continues in the market (and all of the above points are strong indicators of euphoria) - that is anybody’s guess but regular investors should stay in markets in the future + a percentage of the stronger hands acquired during this period

Brings me to a point by Peter Lynch in his books - where in how it is a fallacy to seldom focus on areas that are within core competence rather than look for industries in which our expertise is lower. Is the broking/investing industry growth ongoing fully recognised yet in the investment community?

Discl : Invested

1 Like

8 years of non performance. 4 years of Boom. 2 years of Crash and then a probable Turn Around. Its leap of faith to bet for long term. At best a short term momentum pick.

2 Likes

May Month Volume was highest in last 14 years. and in current month in first 10 days volume are about to cross may month volume with breakout. If I understand it correctly then a big buying has happened and it would not for short term. It seems it will go all time high very soon and then uncharted territory.

Disclosure: I have invested in this stock.

1 Like

The retail investment is at all time high. Clear sign of market frenzy. Every dip will be bought into by retail investors. No matter what FDI or DII does. Its a conducive environment for top equity brokers in the country. Its a good investment as long as euphoria continues.

This will increase their brokerage/fees revenue in coming years. They just started this so good scope for growth of this service.

1 Like

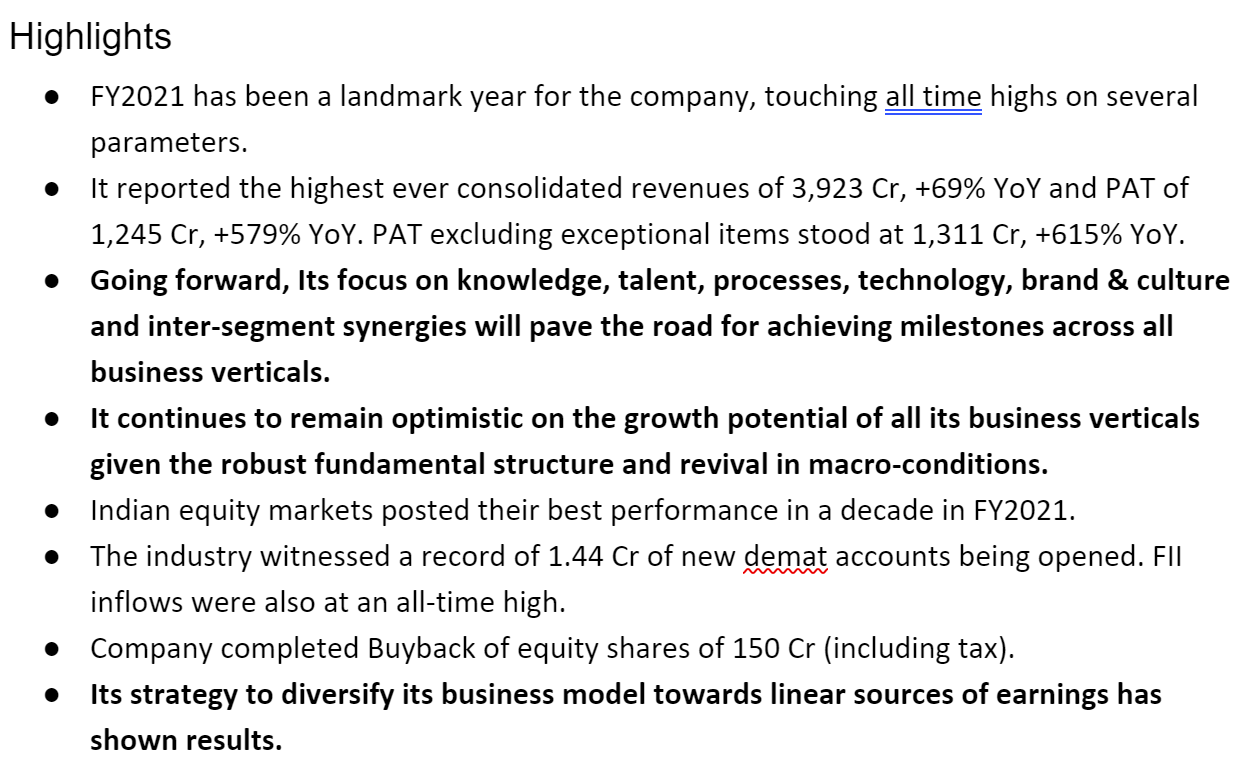

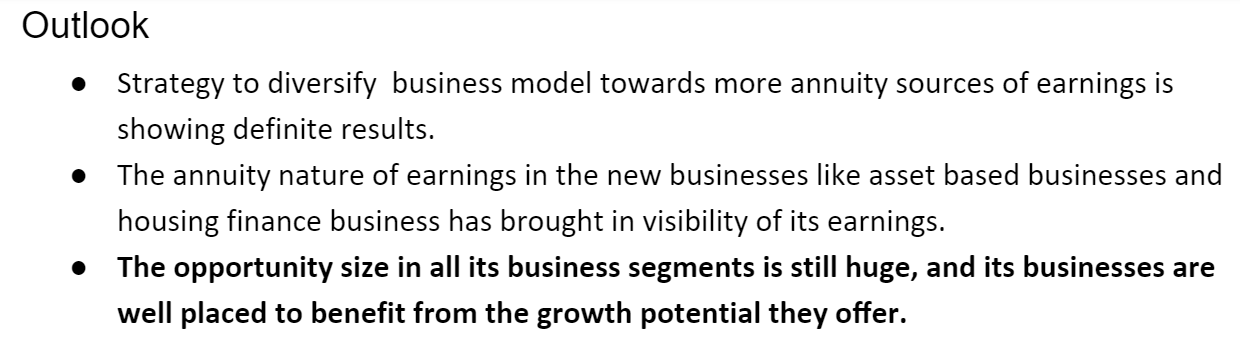

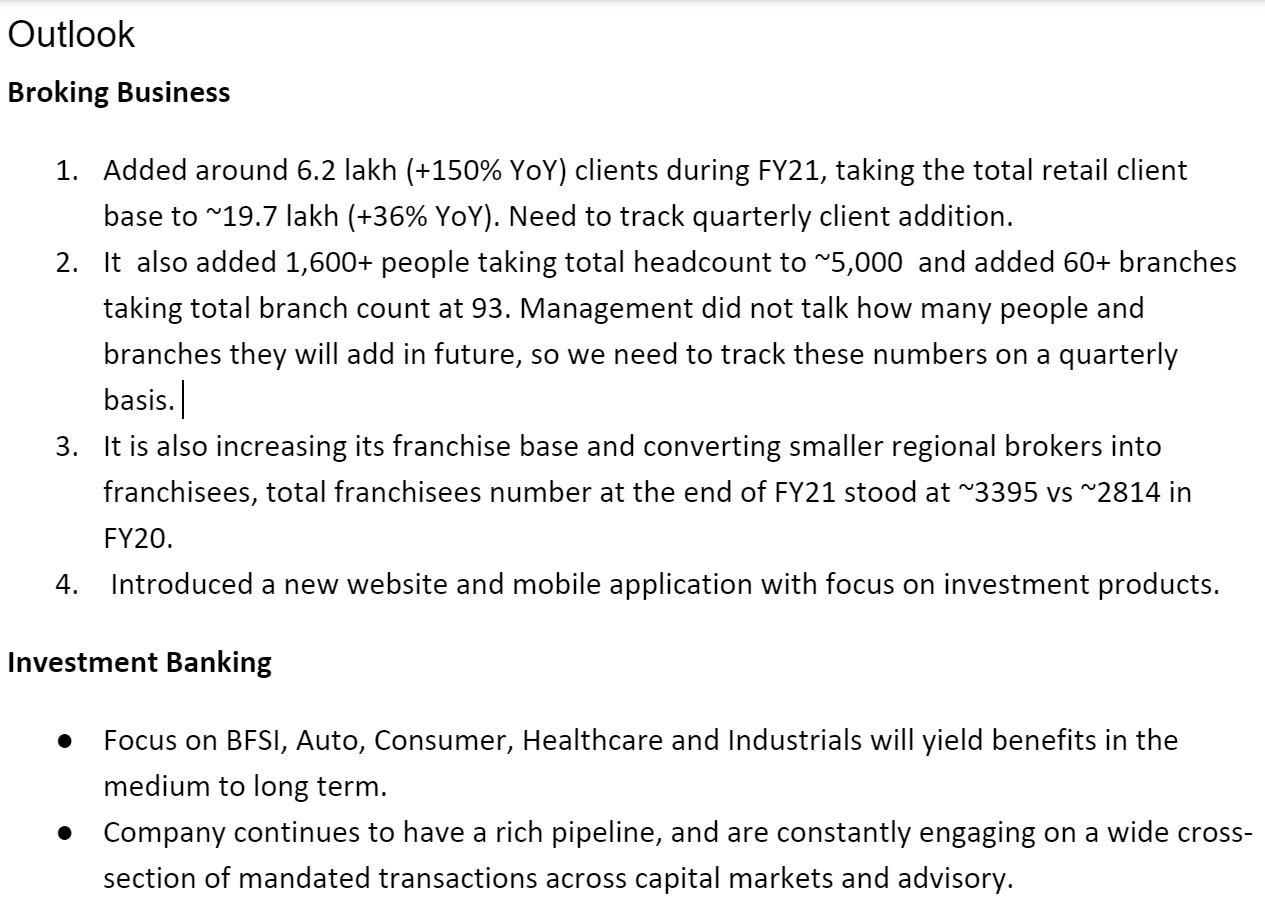

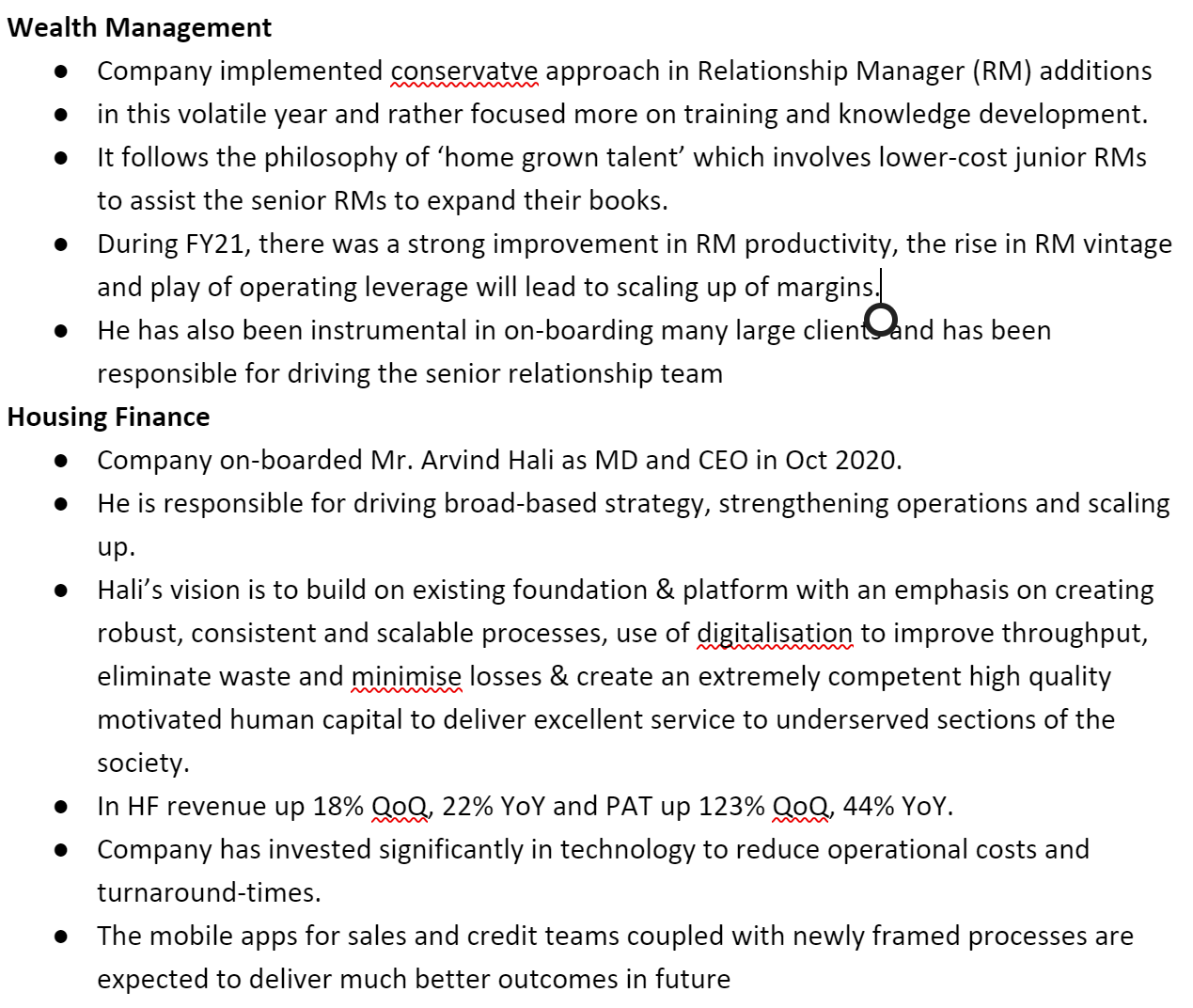

Motilal Oswal AR Notes!

Future looks great for the company! Not many forward looking statement given though… need to track quarterly performance…

Disclaimer: Invested

5 Likes

Tried segregating different business vertical pardon my ignorance if I missed something

Can someone please explain what does Net Gain on fair value and did it have effect while evaluating the company

2 Likes

MOFL is in similar business to that of Angel One. Revenues/Profits are comparable whereas there is a large disparity in the valuations. Any pointers on this, what Market is thinking. One I could think is that Angel one is carrying the ‘FinTech’ Tag? Anything else?