Bad news

Quite expected… MOSL suffers from weak corporate control amply shown by the fiasco at HFC biz as well. I entered and realised that weaknesses around management and process was not to be ignored. Exited with small loss and deployed in Edel. Its retail brokerage, AMC and Wealth Management will do really well though.

What percent is their ‘commodities broking’ business a part of their overall revenue?

The broking business is around 34%

post withdrawn as this is already posted

34% must be the entire broking business majoirty of which would be equity broking

. This news pertains only to commodity business. Please recheck before providing such information

1 Like

Good report.

2 Likes

could not find the link on the BSE but it seems another promoter entity (Passionate inv…) bought the same as per the screenshot posted by you.

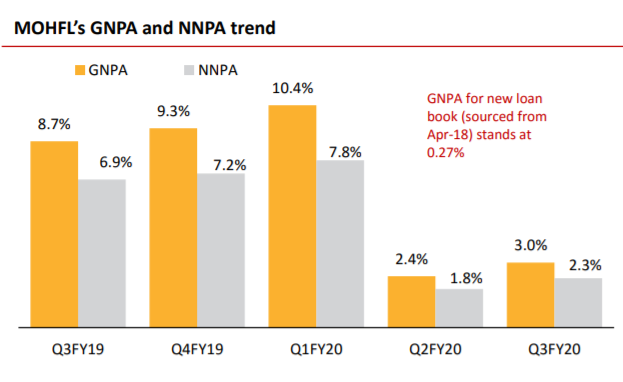

Motilal Oswal Financial’s arm Motilal Oswal Home Finance Limited (MOHFL) has sold pool of NPAs of Rs. 540 crores (having Net Outstanding book value of Rs. 345 crores) and realized cash consideration of Rs. 260 crores from Phoenix ARC Trust. This has resulted in significant reduction of the Gross NPA (GNPA) & Net NPA (NNPA) ratios of MOHFL to 1.95% and 1.51% respectively

4db4b564-3cfb-4a0b-9166-3c5797346002.pdf (710.8 KB)

1 Like

I like to take a storyboard approach to such businesses. Let us understand the story first and then see how to value such a business

Part A - Understanding the story

Phase I - Promoters start the business as a broking entity, put in the hard work and scale to a respectable level. Ride the industry tailwind during 2003-08 and become a household name

Phase II - As Phase I started to result in success, promoters decide to get into the investing game, obviously they had a lot of incumbent knowledge base due to the in house research skills. They started with the PMS offering which did very well and scaled to be a Top 5 player

Phase III - Lull post 2008 which brought to light the cyclical nature of a capital market trading business, annuity revenue is the name of the game for any smart promoter. While broking continued to be the mainstay, the launch wealth management (just a way of leveraging the business connects they already have by managing portfolios for a fee), Private Equity & AIF (HNI product push) and Mutual Fund (retail push) in an effort to reduce reliance on market sentiments

Phase IV - As all these engines start doing well and throwing cash, the quest for more predictable annuity income leads them to a lending business where the risks can be managed. The strategic thinking behind the HFC was right since mortgages are the lowest risk lending segment, affordable housing as a theme was new where incumbent HFC’s would take time to enter that segment.

Phase IV is where the story started going astray for the following reasons -

-

As a capital markets player and as a money manager one takes minimal balance sheet risk. As a lender however balance sheet risk management is the key, culturally there is a mismatch

-

Of the two promoters the person who is more adept at managing operations for some reason took a backseat initially and let the person with the investing mindset run the show. I have noticed that investors usually have a different mindset than operating managers, they lack some skills that are needed to run a tight ship operationally

-

The first CEO of HFC was hired from DHFL, all sales and no credit/underwriting skills. Their ramp up of disbursal was very steep in 2016 and 2017. Affordable housing customers are a different breed, they earn in cash and can easily walk away without caring too much as compared to salaried professionals who are unlikely to default

2018 and 2019 have been years of consolidation where MO has personally taken charge and relegated RA to an non executive role when it comes to operating businesses. HFC book has been cleaned up to a good extent, after the sales to ARC Net NPA is now < 2% of the book. Net worth of the HFC is approx 830 Cr while the capital infused so far is 850 Cr, which means they were better off parking funds in a liquid fund ![]() But then, pace of disbursal has slowed down, hopefully quality of underwriting is far better too.

But then, pace of disbursal has slowed down, hopefully quality of underwriting is far better too.

16 Likes

Part B - How would I value the business

This looks like a classical Sum of the Parts Valuation case, each business has a different quality to it.

- Broking & Distribution - Top 5 equity broker in the country, not into discount broking yet. Broking is a pure operating leverage play beyond a scale where one can have good, average or bad years based on volumes. The distribution part however brings in some stability to the business and is a pure cross sell play. If anything this increases the operating leverage part while bringing down cyclicality to some extent - as distribution AUM grows and revenue share within the segment starts crossing 35%, the cyclicality will start getting smoothened out.

Valuation - Take the FY19 PAT number and give it a reasonable multiple which I evaluate to be in the range of 12-15 TTM PE

- Asset Management including MF, PMS and AIF - My views on the AMC business are well elaborated in the PPT I’d made for the VP 2019 meet, one can see that here - VP Chintan Baithak Goa 2019 - Sector: Asset Management & Wealth Management

Valuation - At 45,000 Cr which is all equity the business will be more cyclical compared to an HDFC AMC which has a debt/equity combination. However this also means that Yield to AUM and profit will be markedly higher since the margins in equity fund management are way higher.

Once again take the FY19/FY20 PAT number and assign a conservative PE to it. I would go with 30 TTM PE since Nippon AMC is at 40 and HDFC AMC is at 50+

-

Wealth Management - A marginal business actually, just take a valuation of 2.5% of AUM or a PE of 18-20 on FY19 PAT. IIFL Wealth Management trades at a PE of 25-30

-

Fund Book - This is nothing but the company’s own money invested into own funds. Valued at 1500-1600 Cr as of Sep 2019. This is pure bottom line play since there is no cost associated with the valuation gains if any. I would not take a PAT approach to this, on a conservative value this purely at market value as of date

-

Home Finance Business - Net Worth of 830 Cr as of Sep 30, 2019 (clarified in yesterday’s conference call). I do not understand lending businesses all that well, given the history of mismanagement, I would probably just value this at book and go with it

What is most important -

All numbers I have used to value are conservative multiples

Other than HFC all others are pure operating leverage businesses with minimal balance sheet risk. Any increase in revenue straightaway flows to PAT

Other than HFC all other businesses are asset light, they do not need external capital at all. The debt ex HFC is backed by 1.2X of that investment into debt mutual funds

Motilal Oswal Financial Services may well be a capital markets powerhouse masquerading as a lending business in the average investor’s eyes. If and when the equity markets deliver a double digit growth rate, all businesses other than HFC should do very well and throw a lot of cash. If one’s call is that the HFC business has seen the worst days behind it and can only get better going forward, this might start looking interesting at current valuation.

Please come to your own conclusions based on your evaluation of the various aspects. This is not a BUY/SELL recommendation or investment advice. This just presents my perspective on how I view this business at this point of time based on my risk profile & requirements

Disclosure: Invested (not a large position) and tracking closely, may add more based on market conditions. I am SEBI registered IA

17 Likes

2 Likes

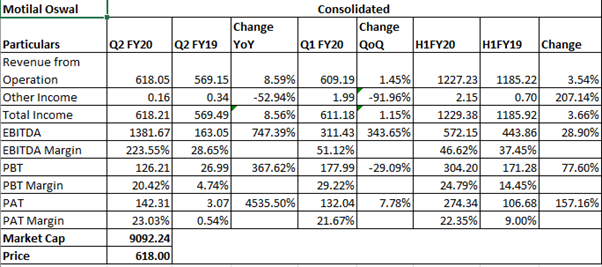

Motilal Oswal Q2 Results!

ROE:

Concall:

Some of the key things that impacted the profit in the current quarter included mark-to-market gains compared to mark-to-market loss in the same quarter last year. We also had an impact of ARC transaction during the current quarter, the adverse impact of that is reflected in the numbers. Also, there were write backs due to change in the tax rate which is a positive impact. So, there is a negative impact of ARC transaction, positive impact of the tax rate and the positive impact of mark-to-market gain compared to the loss in the same quarter last year.

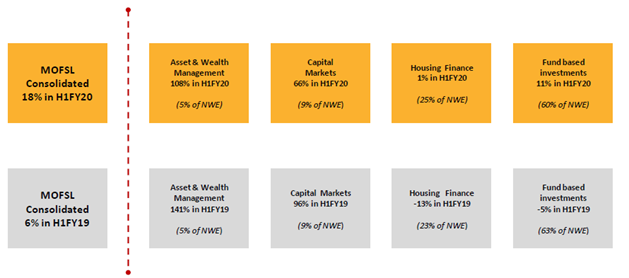

Our overall gearing is at 1.4x while that of ex Motilal Oswal Home Finance, the number is 0.4x. The groups consolidated ROE for the first half is about 18%.

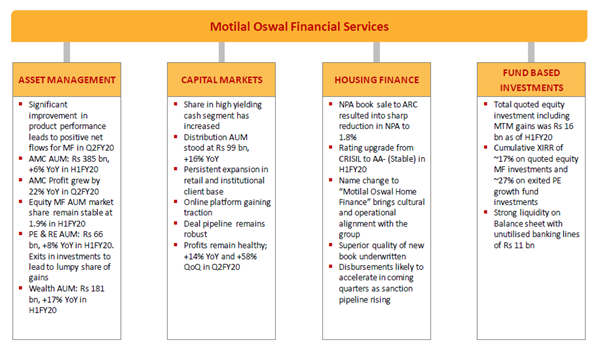

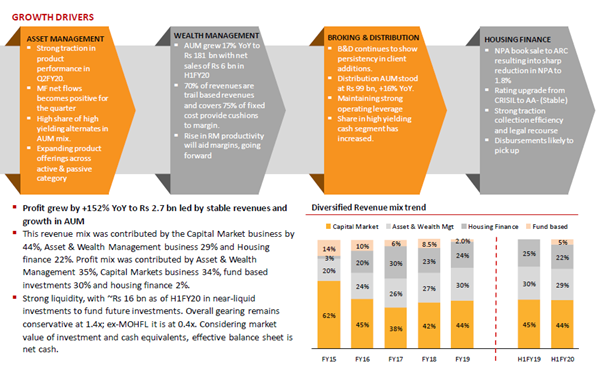

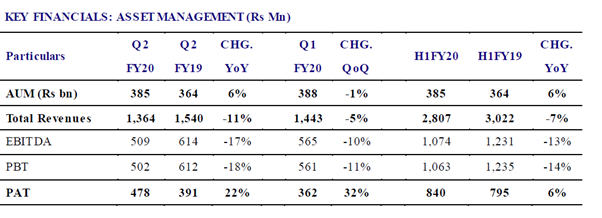

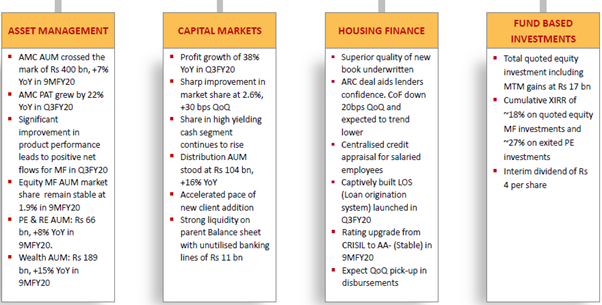

During the second quarter the wealth AUM is up by 17% year-on-year at Rs. 181 billion, the distribution AUM is up by 16% year-on-year at Rs. 99 billion, the private equity and real estate AUM is up by 8% year-on-year at Rs. 66 billion. AMC AUM is up by 6% year-on-year at Rs. 385 billion. We have seen a significant improvement in the performance of all our products on the mutual fund platform and that has led to positive mutual fund net inflows for the second quarter of the year. The home finance business has undergone a name change to Motilal Oswal Home Finance. CRISIL has upgraded the long-term rating of Motilal Oswal Home Finance to AA- stable from A+ earlier. Motilal Oswal Home Finance’s sale of NPA pool to ARC has resulted in net NPAs of 1.8%.

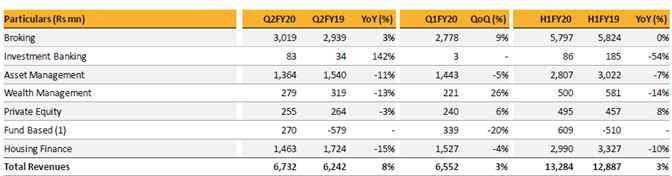

The Asset Management business across mutual fund, PMS and AIF the AUM stood at Rs. 385 billion up by 6% year-on-year. Our AMC ranks number 12 by total equity assets and our PMS ranks numbers one. Revenues and profits for the quarter stood at Rs 1.4 billion and Rs. 478 million (+22% year-on-year) respectively. Our equity mutual fund AUM of Rs 199 billion is 1.9% of the industry AUM of Rs. 10.3 trillion. Our SIP AUM is growing qualitatively and profitably. Our share of alternate assets comprising of PMS and AIF is highest among AMC at 48% and it will continue to rise.

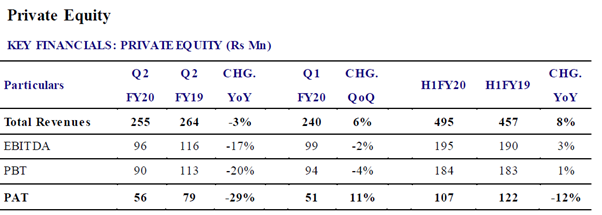

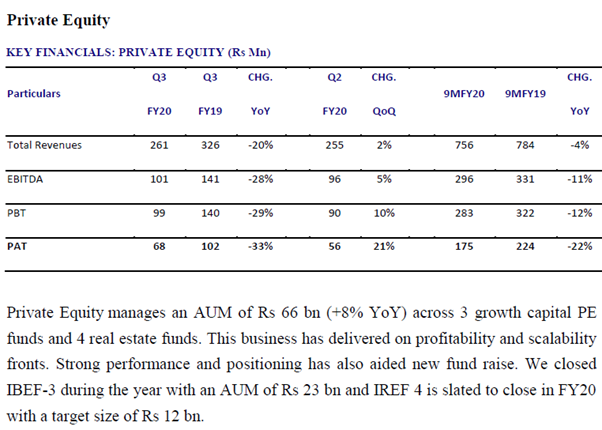

Private Equity manages an AUM of Rs 66 bn (+8% YoY) across 3 growth capital PE funds and 4 real estate funds. This business has delivered on profitability and scalability fronts. Strong performance and positioning has also aided new fund raise. We closed IBEF-3 during the year with an AUM of Rs 23 bn and IREF 4 is slated to close in FY20 with a target size of Rs. 12 billion.

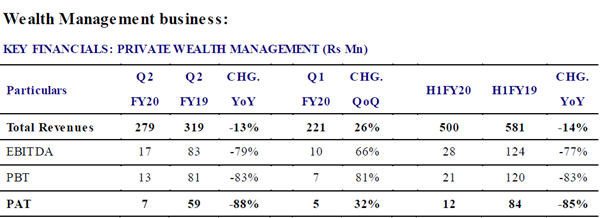

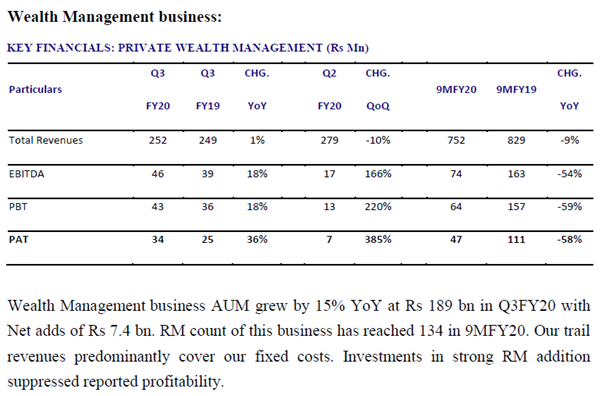

Wealth Management business AUM grew by 18% YoY at Rs 181 bn in Q2FY20 with Net adds of Rs 6.1 bn. RM count of this business has reached 129 in H1FY20. Our trail revenues predominantly cover our fixed costs. Investments in strong RM addition suppressed reported profitability. However, as the ratio of new adds to opening RM’s falls and the vintage of RM’s improve, both productivity and profitability of the business will scale up.

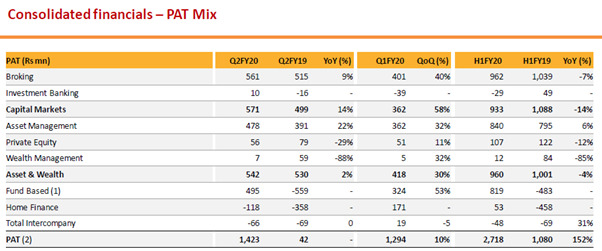

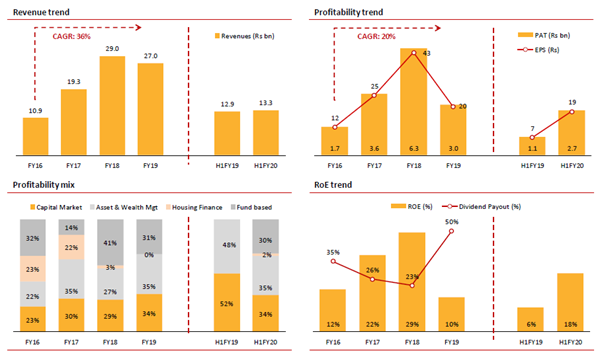

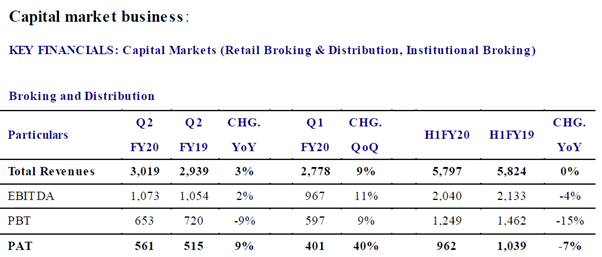

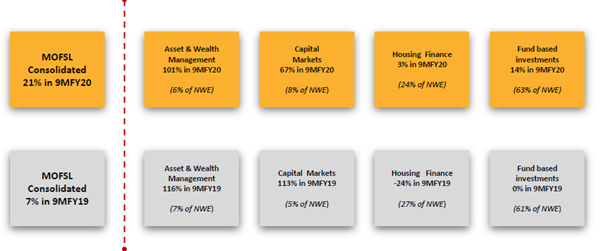

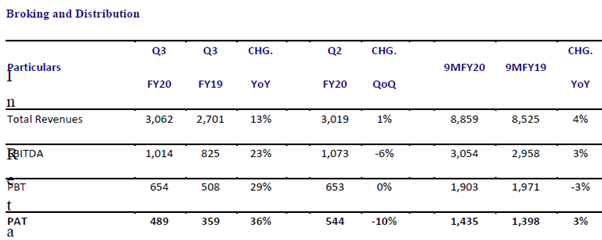

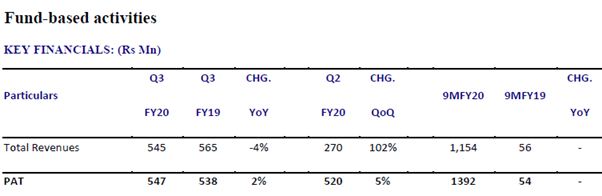

Capital markets comprises of Retail Broking, Institutional Equities and Investment Banking business. Revenues for this segment were Rs 5.9 bn in H1FY20 and contributed ~44% of Cons revenues. Profits were Rs 933 mn in H1FY20 and contributed ~34% of cons PAT. Broking and distribution business profit stood at Rs 962 mn in H1FY20.

In Retail Broking & Distribution, our Market share in high-yield cash segment continues to rise. Our overall market share stood at 2.3% (ex-prop) in H1FY20 due to rising F&O volumes in market.

Our strategy to bring in linearity through the trail-based distribution business is showing results. Distribution AUM was Rs.99 billion, +16% YoY. With only 17% of the near million client base tapped, we expect continued increase in AUM and fee income as number of clients to whom we have cross sold and number of products per client cross sold rises.

In the institutional broking business ranking with existing clients improved, domestic institutions, contribution improved, and new client additions were encouraging. Most of the assets of the business including research, sales, trading, etc., are being strengthened. Business has been adversely impacted by lower yields although tailwinds for well managed local firm remain strong.

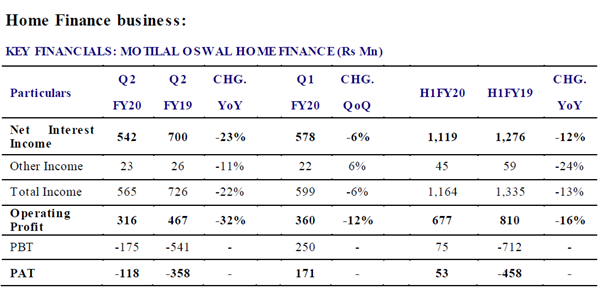

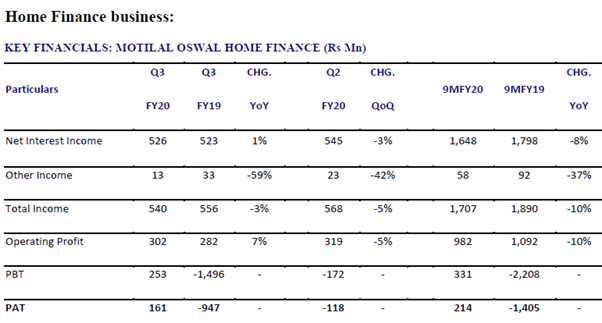

Motilal Oswal Home Finance (MOHFL) reported profit of Rs 53mn in H1FY20 against loss in a same period last year.

During the quarter, MOHFL has sold pool of NPA’s of Rs 5.4 bn (having Net Outstanding book value of Rs 3.45bn) to Phoenix ARC Private Ltd and realised full cash consideration of Rs 2.6 bn. This has resulted in significant reduction of the GNPA & NNPA ratios to 2.39% and 1.82% respectively. This lower NPL’s will help us in further adding to lenders’ confidence and bringing down incremental cost of funds. MOHFL has received credit rating upgrade amid challenging environment based on several positive changes undertaken including name change. CRISIL has upgraded MOHFL’s rating to AA- (stable outlook) from earlier A+ (stable). This will further benefit MOHFL in bringing down cost of funds and improve spreads.

Name change to “Motilal Oswal Home Finance” is expected to yield multiple benefits like reduction in cost of funds, leveraging on brand, group level synergy across functions, locations and business associates. Loan book stood at Rs 38.5 bn as of H1FY20. Disbursements in H1FY20 were Rs 850 mn. New book sourced from April’18 has encouraging performance, with only 6 cases in NPA out of ~4000 loan cases.

Margins remained stable at 5.1% in H1FY20, on account of improvement in yield coupled with equity infusion in CY19. Our spreads have remained stable in an environment of higher cost of funds. Strong traction in legal recourse coupled with improvement in collection efficiency will result in faster resolution of delinquent cases. With likely pick-up in disbursements coupled with improved collection efficiency, augur well for future asset quality and profitability outlook. Strong support from parent continues with capital infusion of Rs 2 bn in CY19 taking total capital infusion to Rs 8.5 bn. Gearing remains conservative at 3.9x. Limited borrowing repayments till March 2020, strong undrawn borrowing lines and ALM place us in comfortable liquidity situation.

Outlook: Home Finance business legacy issues are now behind, and incremental focus will be on profitable growth. We believe that our portfolio businesses are well positioned to capitalize on the entire positive created by financialization of savings and other macro trends. A brand is very well recognized in each of our businesses and we remain exited of how the headroom to grow and generate free cash flows from each of our existing businesses and are going to be sharply focused on deepening our positioning in each of them.

3 Likes

Good numbers posted by MOFSL, mainly led a robust show by AUM and broking business. The NPA cycle in the housing finance is behind us after a painful 15-month period. Hope the company has learnt its lessons after burning its hands in the HFC business. Looking healthier as a business.

3 Likes

Had a quick look into the stock but valuations don’t provide safety.

The problem is that they are not able to scale up the business. Many positives present in a mediocre business but seemed too pricey.

-

Mutual Funds AuM’s are up only because of increase increase in market valuation. On a contrary they are witnessing Net Outflows of 300-400 cr YTD on a AuM of ~20,000 cr. It seems that the biggies/winners (HDFC etc) are gaining the incremental flows. The company has been quite honest though in their disclosures vs. what competitors disclose.

-

AiF and PMS is doing good which together is approx same size as Mutual Funds AuM now. Will be interesting to see how the change in regulations from 25L to 50L affects MOSL. Management seems confident though as in the past also PMS size was increased from 2L to 25L and the players survived.

-

Broking business might be having the best numbers currently. Competition from zero discount brokers and traditional peers will make it tough to increase profits from these levels.

-

Real Estate and Private Equity business has shown good growth in business and profitability.

-

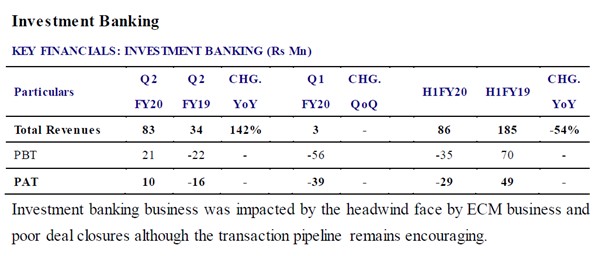

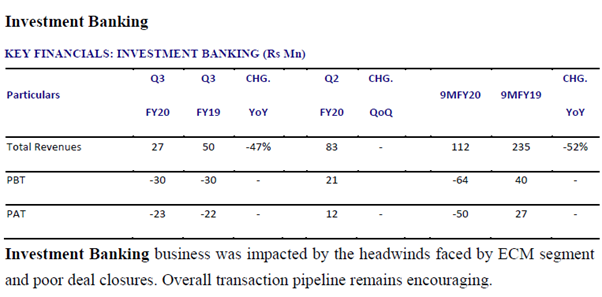

Investment Banking seems to be sub-par.

-

Now the Home Finance business, which the Street is perceiving to have turned around, can be a joker in the pack. Management admits that their Home Finance business is not a blue-chip and just a mediocre one. Lots of changes though have happened from top management changes to bottom-down culture. Low leverage at 3.5x (as it sold substantial part of loans to ARC which also was the reason for fall in GNPAs). Btw disbursements have fallen significantly as the company seems to be preserving cash.

-

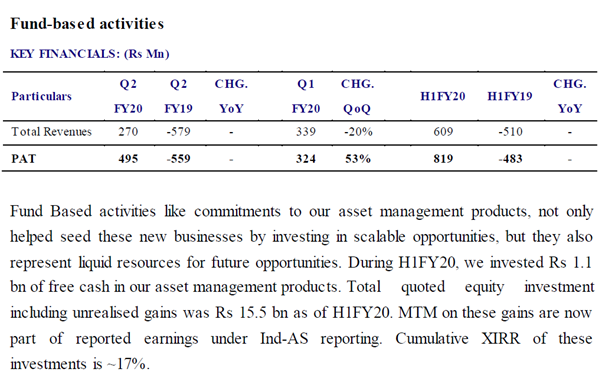

Propitiatory capital investments have been good as investing remains their forte.

Overall, wasn’t comfortable to pay more than 8,000 cr in market cap against its current market cap of 12,000 cr. But happy to see hear momentum view, as to how much optimism the Street is willing to give to the Home Finance business.

6 Likes

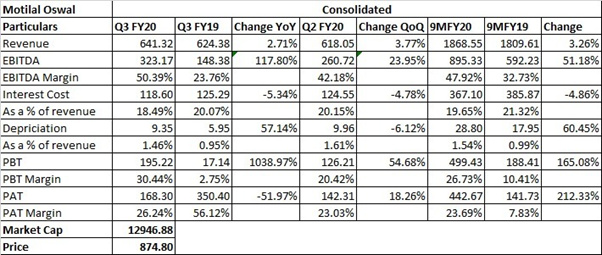

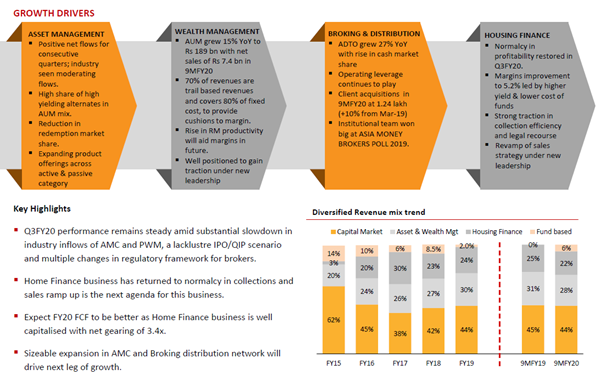

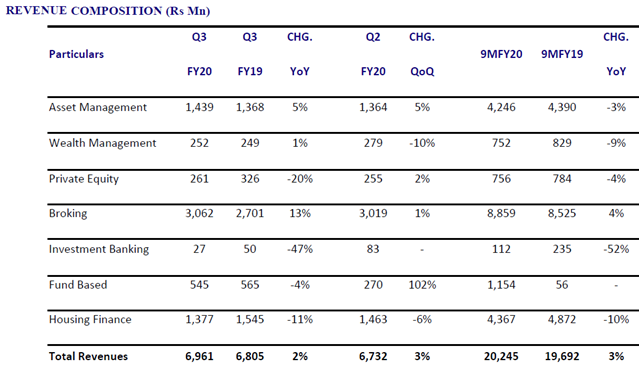

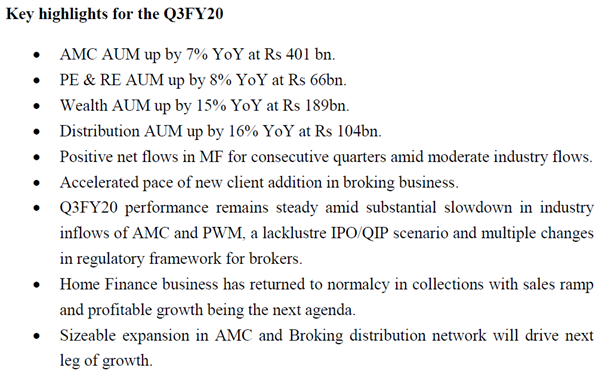

Motilal Oswal Q3 Results!

Q3 FY20 IP:

(NWE- Net Worth Employed)

Q3 FY20 CC:

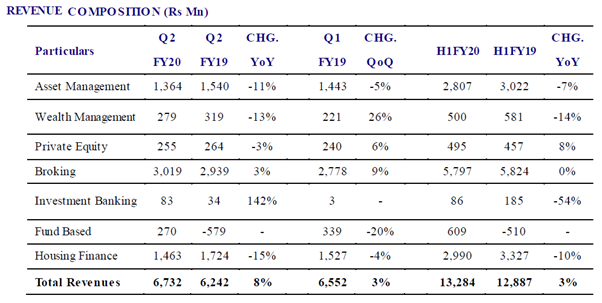

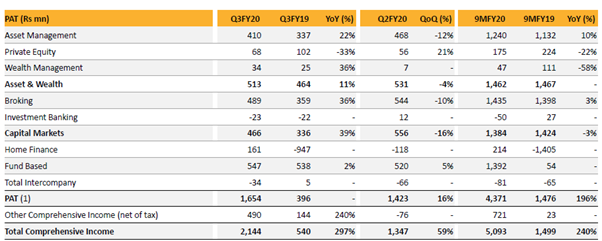

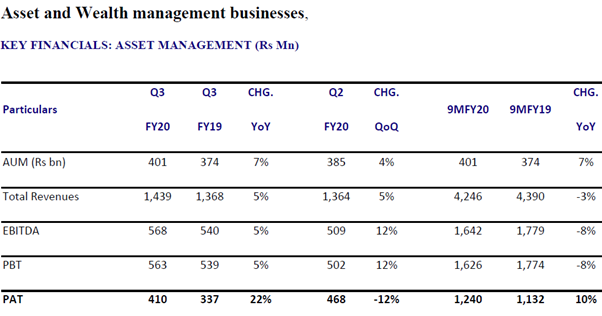

Asset Management business across MF, PMS & AIF stood at Rs 401 bn AUM, +7% YoY. Our AMC now ranks 12 by total equity assets; in PMS we maintain leadership position. Revenues and PAT for the quarter stood at Rs 1.44 bn and Rs 410 mn (+22% YoY), respectively. Our Equity MF AUM of Rs 210 bn is 1.9% of the Industry Equity AUM of Rs 10.8 tn. Our share of Alternate assets, comprising of PMS & AIF, is the highest among AMC’s at ~47% and has continued to rise. Several schemes rank top quartile in performance over 1 year and since inception. This has resulted in traction in our gross as well as net flows.

Capital market business:

Capital markets comprises of Retail Broking, Institutional Equities and Investment Banking business. Revenues for this segment were Rs 8.97 bn in 9MFY20 and contributed ~44% of Cons revenues. Profits were Rs 1.38 bn in 9MFY20 and contributed ~31% of cons PAT. Broking and distribution business profit stood at Rs 1.43 bn in 9MFY20.

Outlook: To sum up, Asset and Wealth businesses are now the largest contributor to our profits with robust growth in AUM. Home Finance business legacy issues are behind with incremental focus on profitable growth. We remain excited about the headroom to grow and the ability to generate free cash by each of our existing businesses.

1 Like

1581606214719 (1).pdf (298.5 KB)

@zygo23554

SEBI has banned upfront commissions for PMS distributors. It has also mandated all distributor fees to be paid by PMS and not AMC. Do you see a similar benefit accruing to Motilal AMC as HDFC AMC has seen over the last 12 months? MOSL pays almost 60 cr of fees on alternative assets per quarter.

2 Likes

Good you caught onto that, shows that we folks are clearly learning and applying those learnings real time. This was expected though, some wealth managers had stopped giving upfront credit to RM’s from this FY proactively. This no upfront regulation comes into force from May 1, 2020 as per the circular.

The circular also more or less rules out the possibility of buying AUM going forward, a lot of PMS were paying out more in upfront commission than what they were making from the customer as management fee. With the new regulation it essentially means that the most a PMS can pay the distributor is that annual fee that they make.

Motilal Oswal PMS has AUM of 15,000 + Cr on PMS & AIF and 6000+ Cr on PE. All of these were paying out upfront commissions in year 1 with an annual trail starting from year 2. Once this comes into effect, there will be definite cash flow savings for them in FY21 based on how much gross sales they do over the year.

I’d asked them this question indirectly on the Q2 conf call with the exact intent of figuring out the extent of this benefit, you can see from the conf call transcript and estimate the possible savings for yourself. The upfront being paid out by most PMS to large institutional distributors is in the range of 3-4% for year 1 and a trail income from year 2. After this the industry is likely to move to a trail income of 1.25-1.5% per annum from year 1. Effectively the yield for a wealth manager will not change over 3-4 years but the commission outgo for a PMS/AIF/PE will now get spread out uniformly over the period rather than paying out 4% upfront in the first year.

Extending this logic, you should be able to estimate to what extent IIFL Wealth yield to AUA will fall starting from May this year. They have traditionally clocked 0.7% of AUA per annum since they were doing MF business for lower margin and making spread on PMS/AIF/Structured products book.

9 Likes