First of all thanks for your analysis. It triggered me to really dive deep into MOFS in detail. Please see if what I have found is helpful to you.

The Net Gain on Fair Value change is a term used to assess an increase in the value of Equity holding which is notional but however, this assessment is done to increase book value. In Taxation terms, this is called Fair Value through Other Comprehensive Income (FVOCI). You could see this term used in the MOFS Annual report as well.

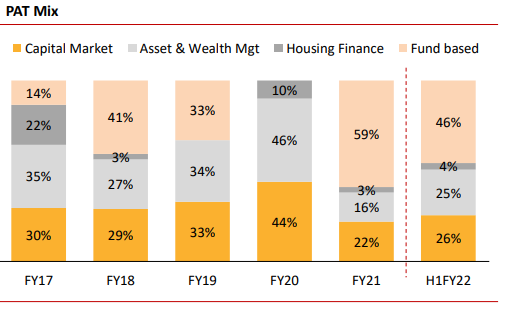

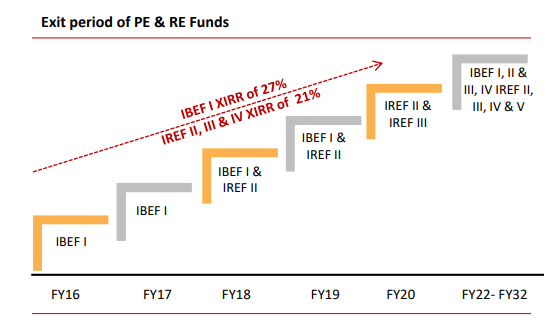

So the question comes why does MOFS use this? MOFS is a bundle of multiple businesses (Broking, AMC, Wealth Management, PE, and Home Finance). In this, the Private Equity part invests in Private Business as well.

MOFS has invested in over 31 Business which you can see here, even I was surprised that their PE funds have invested in some marquee names (IEX, Dixon, Kurlon, Dairy Day, Cycle Brand etc…).

Coming to the point the value in these companies needs to be reassessed from time to time to revise book value. Although MOFS hasn’t explicitly given a breakdown there is another example publicly available which is from xelpmoc technologies. This company invests in startups and makes software for them. In this list, you could see how they have been reassessed quarter on quarter.

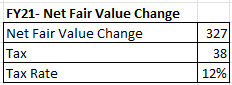

MOFS has done the same thing and has reassessed and they have also paid taxation on the same. The reassessment and holding are not publicly available. In FY21 they have increased the value of their holding by 327 Crores and paid around 12% Taxation on that. (Looks like a Capital gain tax not sure).

The calculation in your blog subtracts the Net Fair Value gain into PAT but the PAT of 1259 declared in FY21 is without consideration of FVOCI Income. Please see the highlighted picture below.(Pg 36: FY21 Annual Report)

So I believe you should reassess your calculation. Further, I wanted to point out that you have assessed the balance sheet based on “Brokergate”/Dividend Income/Interest income. If you dig further deeper they have given the split up clearly based on Business which will give you a better perspective. I’m preparing a detailed investment note. I will share it in a day or two