Pharmax acquisition update and latest earnings call transcript

Promoter has bought 18,26,618 shares from open market in December. Promoter stake has increased by 1.246% ion December month alone.

https://www.bseindia.com/stock-share-price/disclosures/sast/539940/

1 Like

Max Ventures - COVID Update :

Packaging films has little or no impact as it is essential business. Mid term can see some demand softening due to economy slowdown.

Real estate has short term impact for some project however premium commercial real estate is likely to consolidate and MAXVIL can potentially benefit in long term .

https://www.bseindia.com/xml-data/corpfiling/AttachHis/b0ab5aeb-fbaf-4302-9ad4-a8e4cca6180b.pdf

2 Likes

Good results

1 Like

Hi,

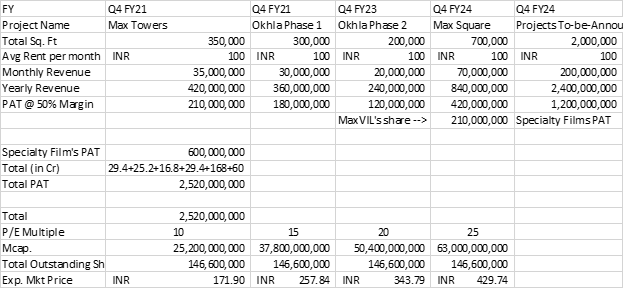

Put two and two together and came up with the following calculations. Request people to poke holes and correct me if i’m wrong. May seem optimistic or biased but this is just my prediction if you stay invested in the next 3-4 years.

| FY | Q4 FY21 | Q4 FY21 | Q4 FY23 | Q4 FY24 | Q4 FY24 | |

|---|---|---|---|---|---|---|

| Project Name | Max Towers | Okhla Phase 1 | Okhla Phase 2 | Max Square | Projects To-be-Announced | |

| Total Sq. Ft | 350,000 | 300,000 | 200,000 | 700,000 | 2,000,000 | |

| Avg Rent per month | INR 100 | INR 100 | INR 100 | INR 100 | INR 100 | |

| Monthly Revenue | 35,000,000 | 30,000,000 | 20,000,000 | 70,000,000 | 200,000,000 | |

| Yearly Revenue | 420,000,000 | 360,000,000 | 240,000,000 | 840,000,000 | 2,400,000,000 | Total PAT |

| PAT @ 70% Margin | 294,000,000 | 252,000,000 | 168,000,000 | 588,000,000 | 1,680,000,000 | 2,688,000,000 |

| 51% Ownership | Specialty Films PAT | 750,000,000 | ||||

| Total | 3,438,000,000 | |||||

| P/E Multiple | 20 | |||||

| Mcap. | 68,760,000,000 | |||||

| Total Outstanding Shares | 146,600,000 | |||||

| Exp. Mkt Price | 469.03 |

Pasted some excerpts from management con calls and other press releases.

Please comment and share your thoughts.

I have not taken into account their investment in nykaa or azure hospitality.

2 Likes

everybody is speculating that because of Covid, now WFH phenomena will increase , it means it will adversely impact the rental income ?

Few points to consider:

a) You have taken 70% margin but you need to include depreciation and interest charges as well. I think pat margins could be around 50% instead of 70%.

b) You have taken entire income of Max Square in your calculations but the share of income with max ventures is only 51% so should be pro-rated.

c) You are assuming 100% occupancy in all buildings which is too optimistic.

d) 2 mn sq feet yet to be announced i would not consider as of now to be conservative.

1 Like

I think Being a good location in Delhi,Okhla Phase 1 and 2 deserves more rent than 100 per sq feet.

Yes Max square only 50 percent revenues.

I did a similar exercise 4 years back and now my investment amount of 65 bucks is only 33.10, if one thinks that the market is valuing the business efficiently.

Your expected price in 4 years from the current price is a moonshot. Do study the business before applying 20 PE for both Commercial RE and film business, which is 49% owned by Toppan group. Ponder over below questions:

- How an individual investor will benefit? Dividend Yield; Capital Yield or…?

- How come the market does not see the potential that was evident in your basic maths?

- Who will fund all these upcoming projects? What about a cut for them before one calculates the PAT?

- Company did a rights issue for ~ 450 Cr. and the market cap today is almost at the same level although the business has improved as compared to those days. Why so?

‘We’ as the equity investor SHOULD dig deeper in to INDUSTRY & Company dynamics before taking the plunge.

Disclosure: Invested

2 Likes

WFH is only a theory and it can’t work for most of the firms. Besides if more education rates increase and more people come to work in white-collar jobs will increase demand for commercial RE.

What is the acquisition of Pharmax is for? What does Pharmax do? I am not able to find any details on internet.

I see that you are long term investor in max ventures, so can you pls answer your questions for benefit of all? Honestly, I do not have concrete answers for these.

Disc. Have tracking position

The idea of raising questions was to help the fellow VPer to do a deep dive. On a lighter note, I generally raise questions to keep others busy ![]()

My investment rationale is from the viewpoint of Real Estate (RE) as this is the only RE investment in my net-worth. RE has a long gestation period so market price ticker does not bother me. I trust the people in charge, both the promoter and the ‘BIG’ insurance partner, and finally the company is getting very focused on RE aspect.

I have nothing much to add ![]()

1 Like

With due respect to your views and the management, in long run they have proved value destructive to minority shareholders. In case of max india, the health insurance high growth business was sold to PE. In case of max financial, the best interest of minority investors would have been merger with hdfc life few years back when they had the chance. In max ventures, the big pe investor will get it’s regular rental income as it is now investing in individual projects rather than max ventures…we minority investor could end up paying for growth while someone else reaps the benefits…I had huge trust on management so was initially invested in all max firms…sold off max india at significant loss, still hold max fin and ventures

2 Likes

Hi all,

First of all, its good to have the discussion going again.

Second, I have considered MaxVIL’s share in max square as 50% only. Maybe it’s not readily observable.

Third, I have made changes to basic calculations (yes, its basic stuff). When you are looking 3-4 years down the line, the more unknowns / assumptions there are, the less accurate your model usually becomes

Also, if I could draw your attention back to Nov-Dec-Jan 2019, thinks were looking good for MaxVIL. The promoter had bought close to 30 cr worth of shares from open market. Every quarter in FY20 was profitable (things were looking to pick up!) and then corona happened.

Maybe now, with lots of pending events (Max House Okhla Ph-1 inauguration, Announcement of a distressed project acquisition, start of construction of Max House Okhla Ph-2 and Max Square, 100% occupancy levels announcement in Okhla Ph-1 and Max Towers, etc) MaxVIL’s time has finally come…? Let us wait and watch.

I have arbitrarily assumed 2M sq feet by 2024 as management intends to develop 1M sq feet a year (that’s the aspiration to scale, already shared a screenshot above)

Also, changed assumption to 50% margin and estimated mkt cap over a range of PE multiples. Let’s hope things work out! I hold a good amount at an average of 50. I first bought at 85 levels and have also averaged heavily at 28-30 levels.

1 Like

Pharmax Corp was basically a land parcel meant for development of Max House Okhla Phase 2.

Have you done any calculation based on if they use the cash from rent along with some debt on developing next big noida twin tower? Nothing against your views or management, the idea is if a company or group companies history is mostly non profitable growth and opportunistic deal making in which minority investors hardly benefited, what can we expect in future…only deals and mergers and demergers?

Disc. Non core holding but reevaluating

1 Like

Positive developments announced during the con call. Did anyone listen in…?

MaxVIL has bid for 2.5 to 3 million sq feet area campus (near or at Delhi One? I’m not very clear on the specifics)

The matter is sub-judice and is taking longer than expected (by 3-4 months, due to covid)

But hopefully they should announce something by Q2-Q3 FY21

Real Estate vertical - well capitalized

Lots of interest from funds looking to partner with MaxVIL for projects

They will strive for EBIT margin of arround 10 - 11% in the speciality films biz in the year to come

Assuming revenue to be 1000 crore, that’s a cool 100 crore

Also looking to retire some debt in the coming year, 5KTPA capex approved for Q3 costng around 30 cr by way of equity infusion by both toppan and MaxVIL

Let’s hope for the best!

Real estate biz has had negative EBIT due to max tower’s debt being capitalized (minor portion) and one time expense incurred for broker commission (makes sense)

EBIT should improve with more higher occupancy in the days to come (with both Max Towers and Max House Okhla Phase I being operational)