Couple of things that I would like to add here.

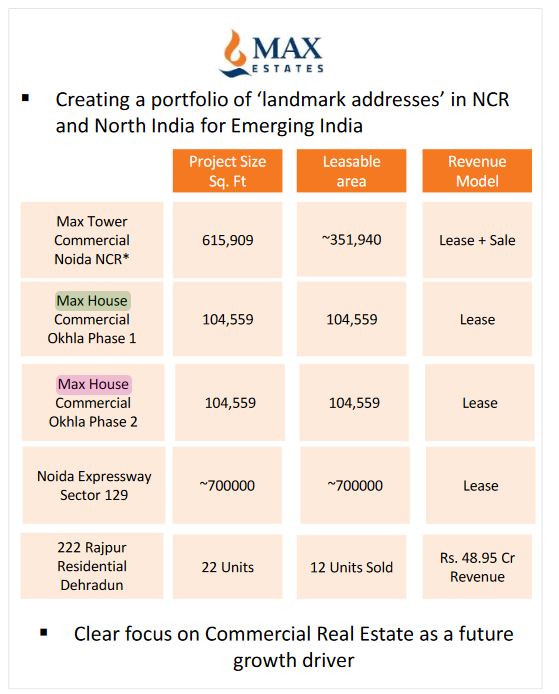

- Max House Okhla Phase-I’s capacity is 1 lakh sft as per management’s commentary from the beginning.

- Max House Okhla Phase-II is also 1 lakh sft based on the management team’s earlier communication.

Couple of things that I would like to add here.

Maybe you are referring to an earlier presentation. The screenshot attached below is from the Q3 earnings call transcript

Max House Okhla: Total capacity is 3 lakh sft

Phase-I: 1 lakh sft

Phase-II: 2 lakh sft

Got clarification from the IR. Total super built-up area for both phases included is 3 lakh sft for Max House Ohkla. Leasable area is ~1.05 lakh sft for each phase. The non-leasable area is 90k sft which is mostly for parking.

As per IR, the transcript of Q3 earnings is a miscommunication from management and they will fix the presentations going forward with the above data.

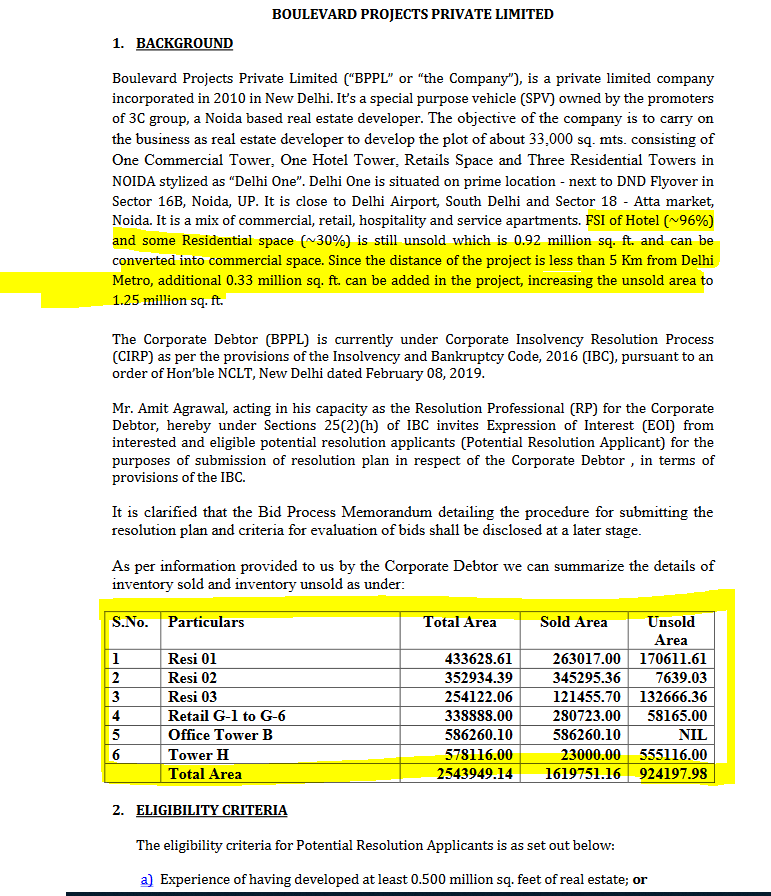

As per concall, the new project bidded under CIRP is the Delhi One Project adjacent to Max Towers. Matter is sub-judice and 100% approvals are not yet received. Approvals delayed due to Covid by 3-6 months.

As per management commentary:

Did some research online and below is the data I could find.

Bidders list shows Max Estates as one of them. Source: http://www.delhione.in/pdfs/EOI-person-final.pdf

Source: http://www.delhione.in/pdfs/Revised-teaser-New-30-04-2019.pdf

Looks interesting to see how they will deliver such a big project in a way efficiently. Can be a make or break for the business based on execution. Views invited.

Disc: Invested.

Awesome. How did you zero in on the link, if I may ask? Great work.

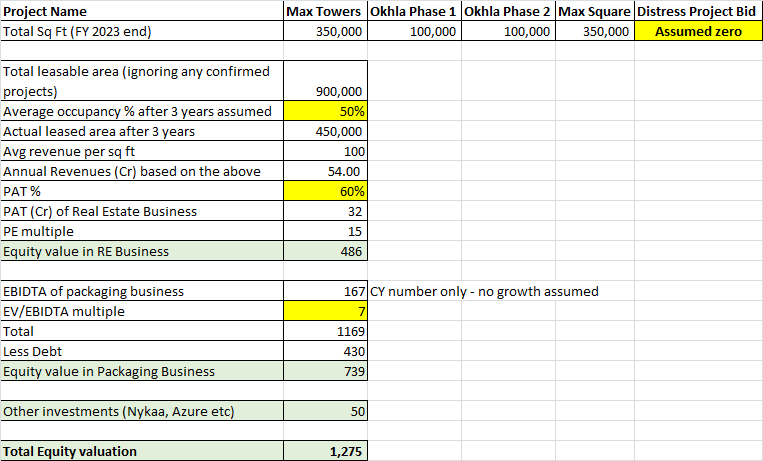

Taking forward the discussion on valuations that @white_hat had posted a few days ago. I have tried to make some further discounts conservative estimates. The key assumptions i have made, i believe are (quite) conservative, and are highlighted in yellow ink.

Assume this is how the company looks 3 years from now, I would like welcome views to understand, where could this possible go wrong? What am i missing here?

(Thank you @white_hat for the starting point)

Hi Ayush,

Few points I would like to add:

In my opinion, the key trigger can be the distressed project (if the approvals and execution etc come along well) and the remaining project pipeline. Future pipeline is 4-5 mil sft as per management which they are pursuing. This includes the distressed Delhi One project. Management expects 40% of the deals (1.6-2 mil sft) to be finalized this FY. Over period of time, they expect scale to be achieved by taking debt through lease rental discounting of the above leased projects, upper cap of 1:1 D/E (110 cr of debt at present) and rough equity of 600-700 cr for RE based on my below ballpark and (amateurish ![]() ) calculations.

) calculations.

Equity: 450 cr rights issue, 150 cr from New York Life + Siva Warrants, roughly 145 cr from Toppan.

Majority of above was invested in RE business primarly in the form of equity for Max Towers/Max House Okhla/Small residential project. 600 cr to construct Max Towers. 89 cr of equity in Max Square, 130 cr for Max House Okhla Phase-I.

Distressed project rationale in my view: Lesser cost to finish the construction, quicker turnaround time to lease (since a large part of construction is done - Travvir this link shows the unfinished buildings around Max Towers in Delhi One).

Please share your views. Experts, please correct the above calculations as applicable.

Disc:Invested.

Tour of Max Towers seems really good. Professionally built. Looks sleek and modern.

Agree with your point about the surrounding buildings. If they do indeed win the approval for development, completion wouldn’t take as long as we would think. Maybe 12-18 months, is my guess.

A couple of questions though.

Isn’t it strange that about 250-300k sq ft of Max Towers was conveniently sold off to related Max entities at “nominal” profits? Is this a governance issue?

Has Max Financial or Max India created significant wealth for minority shareholders who have held on to their ownership since nascent stages?

Where exactly is value to be found for us (MaxVIL’s minority shareholders)? Are they looking to sell part of the RE space to other players? What are the possibilities for a REIT listing? When will adequate scale be achieved for this? What is scale in this biz? 5 million sq feet? 10 million perhaps?

2 or 3 or 5 years down the line, do you see this firm becoming a DLF or a Godrej Properties type biz? Will mutual funds and other players start joining the party to gain ownership? This seems like the only way for share price appreciation. Finding the greater fool. Could MaxVIL become $1B - $3B company going forward? What are the conditions required to achieve the same?

I’m a shareholder and this is my 2nd largest holding and I remain optimistic about the firm’s future. But it would be good to ponder over some of the questions raised.

With regard to @Compounding_Miracles’s valuation, the book value right now is close to 900 cr or roughly Rs 60 per share. Equity valuation of 1250 cr after 3 years seems too conservative, in my opinion. But of course you have assumed zero growth.

That’s big conviction! Would be great if you can share your portfolio or top 5 holdings. It will help to understand your investment rationale in general. I ask this as at one point max group was one of my largest holdings. I have exited max india and trimmed down max financial. Max ventures is something I am still holding. However, it is not clear to me what significance this company holds to the promoters and what their intention is. It’s name suggests it is neither a real estate not packaging company but rather is a venture to create some businesses. What if they create and sell out to PE the successful baby like they have done for max india for health insurance? Will small investors still benefit? Thanks

Hi,

Centrum Capital

MaxVIL

Kei Industries

Godrej Industries and

CRISIL are my top 5 holdings

A mix of safe and risky bets ![]()

Good question. The initial 1.15 lakh sft of space was already sold to the erstwhile Max India by the 3C Developers. I am not sure if it is just an accounting entry in P&L for Max Estates but the results show 161 cr for 1.15 lakh sft. So on average rental of 100 per sft, it is 8.57% rental yield.

The 1.45 lakh sft sold to Max Life Insurance in Q2 FY20 was at 200 cr. So, the rental yield turns out to be 8.7% which looks okayish to me. In my opinion, the profits look “nominal” because of the cost of construction which is around 350 cr for a 6.15 lakh sft building (~60 cr per lakh sft of construction cost + an acquisition cost of 250 cr to take over the project). As per management, there was lot of baggage for finishing Max Towers due to the stuck Delhi One surrounding the towers campus which costed them more. They seem to take lesson from this in construction of Max Square, projected construction cost of 300 cr for 7 lakh sft - making it 42 cr per lakh sft (plus an acquisition cost of 110 cr for land, so total cost of Max Square is 410 cr for 7 lakh sft).

Regarding 2., data is out in the public, so I would not add any comments on that. This is the recent development - Max promoters to sell stake in financial and healthcare business to reduce debt | Mint So MaxVIL might be the main focus for the sponsors in addition to Antara going forward.

3.) The management guidance is to target to deliver 1 million sft per year of commercial RE over the next 5 years. That is the scale they are referring to in the past 2 concalls.

4.) Not sure if we can compare to DLF/Godrej. Business model is different. Build and sell vs. Build and lease. More relevant comparison might be Embassy REIT or Phoenix Mills (retail lease vs. commercial lease of course is different). The company looks undervalued but it is more from asset POV. For the share price to appreciate, they need to show earnings via. leasing and it will need significant amount of inventory to be built to reach that phase in my opinion. For me as of now, it is a pure play on the execution and management skills of Sahil Vachani (and not Analjit Singh for me).

I have highlighted several points mentioned in the con call PDF:

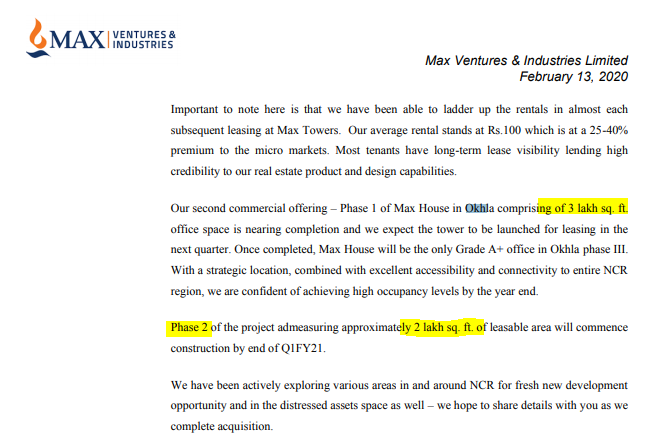

Max Okhla Phase 1 to commence leasing in Q2FY21. Phase 2 to launch soon after.

They have teamed up with start ups and created virtual video-based interactive tours of their offices to rope in prospective tenants.

Upon completion of future platform-level projects, they will be entitled to development, management fees etc (Any idea how much this would amount to?)

Significant opportunities seen in commercial real estate. Grade A offices to be least impacted.

Actively prospecting distressed green and brownfield assets of 4-5 million sq feet. Anticipate closing of about 40% in current FY. This may include certain brownfield assets that might be immediately leasable. Build-out period for greenfield projects roughly 3 - 5 years.

Looking to monetize stakes in both Nykaa and Azure hospitality and focus future investments only in real estate space.

Expect significant debt reduction to happen in the specialty biz by end of next FY.

Have clear line of sight to delivery 5 million sq feet in the next 5 years (“conservative target” as mentioned by CEO)- Page 11

For the Delhi One project, They have received 100% approval of committee of creditors and final clearance and approval is pending from NCLT. Anticipate delay of 3 - 6 months. Deal structured to match outflows with future inflows. Platform partnered likely to be a norm going forward in-line with asset light biz model.

Max house okhla Phase 1 and 2 to cost roughly 130-140 cr each and expect Phase 1 rental of 15 - 16 crores from year one.

Not looking to dilute equity, especially at current levels. Stock is hugely undervalued according to CEO (Page 20)

Max Square costs 30-32 crores per lakh sq feet compared to 60 crores per lakh sq feet for max towers. Quality will be same. Reason for higher cost at Max towers was they had to complete a lot of external development as developer had gone bankrupt and that is not the case with Max Square.

Overall, positive commentary. Lets see how things unfold going ahead…

MaxVIL Con Call.pdf (727.3 KB)

Max House Okhla Pre-launch event:

What’re the implications for minority shareholders like us? It will cause dilution but improved earnings due to value added products will offset it.

Board of Directors of Max Speciality Films Limited (“MSF”), (material subsidiary of the Company) in its meeting held on July 27, 2020 has approved issuance of equity share capital upto INR 30 Crores (approx…) on rights basis to its equity shareholders, viz. Max Ventures and Industries Limited and Toppan Printing Co. Ltd., Japan. The equity shares will be issued in ratio of their existing shareholding, i.e. 51:49. The said equity funds shall be utilized by MSF for setting up of a new Metallizer Line.

The new Metallizer Line is expected to be up and running by the third quarter of FY 2020-21. The line will not increase overall capacity because the base film remains the same, but it will enhance MSF’s ability to improve the value-added speciality component in its product category.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f871de99-80e1-43f1-bc7f-b003fd6ae545.pdf

The shares will be issued at around 89 rs per share of 10 rs face value while currently they are trading at 39 rs per share of 10 rs face value…what am I missing here?

Very good results by Max ventures

Rs 89.5 per share is the share price of MSF not MAXVIL. The equity dilution is happening at MSF level and not at MAXVIL.