There is also cash at bank which needs to be given some value. Also their dominance in the market needs some value to be attached.

It is not just the growth, you also need to look at the longevity of growth and possibility of us being right. So we may have to adjust margin of safety accordingly.

Also you must consider the 1000 bucks a share (or whatever it is now) bank balance when you look at current market price.

I considered Free Cash Flow for DCF Valuation. However I am seeing Cash and bank balances as Rs. 711000000 and the total number of shares is 302080060 . Per share the value would be Rs. 2.35. This is very less.

I used Free Cash flow to value in DCF.

For Market share and presence of MOAT, DCF is not the correct valuation technique in my view. We have to Consider EPV (Earning Power Value) which is a Combination of Earning Value + Asset Value + Growth. Generally Growth is put as 0. I did a calculation and it stands at 4,402. Clearly Market has put 3.5 K extra for Growth.

1 Like

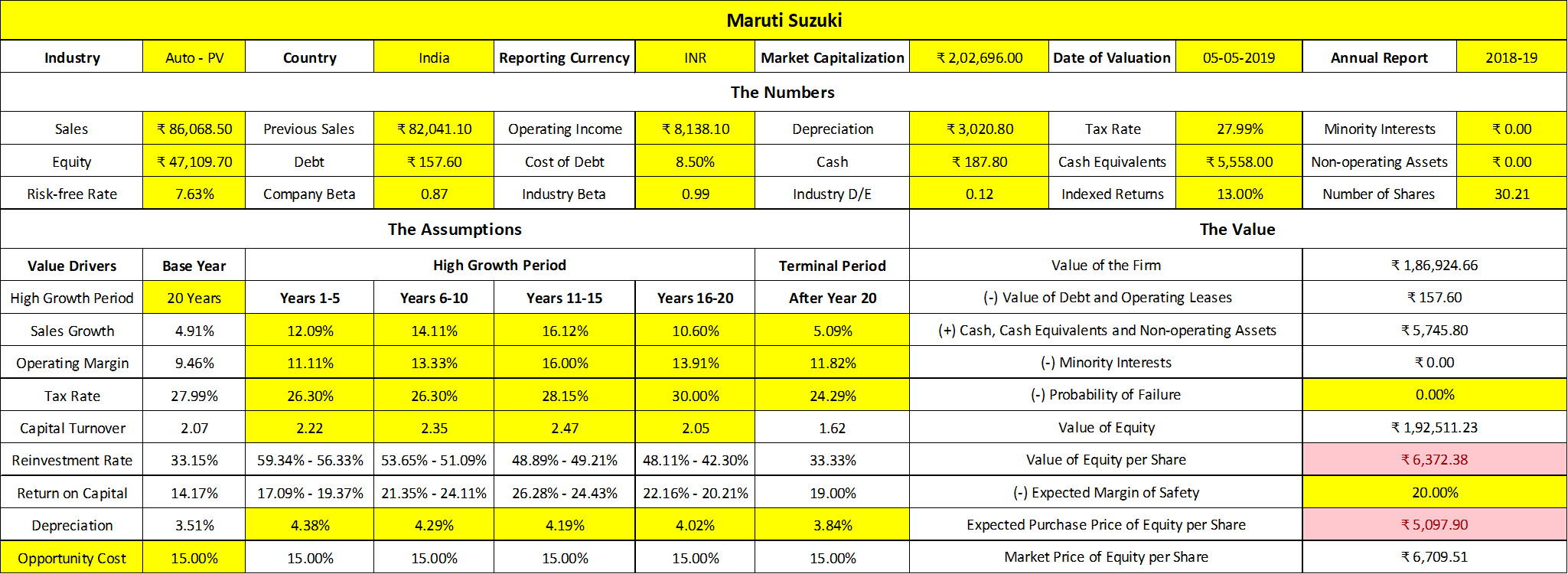

This is how I would probably value Maruti Suzuki:

Numbers and Narratives (Compact) - Maruti Suzuki (Dinesh Sairam).xlsx (25.9 KB)

At an even lower level of MoS of 10%, the value is ~Rs. 5700. I wouldn’t mind purchasing Maruti Suzuki at this level too and then averaging down if it goes below that. The company has an excellent and consistent operating history–so much so that there’s probably no need for a Margin of Safety at all. But hey, at this point, it’s a force of habit for me.

9 Likes

There is 34000 crores in debt funds. So please recheck.

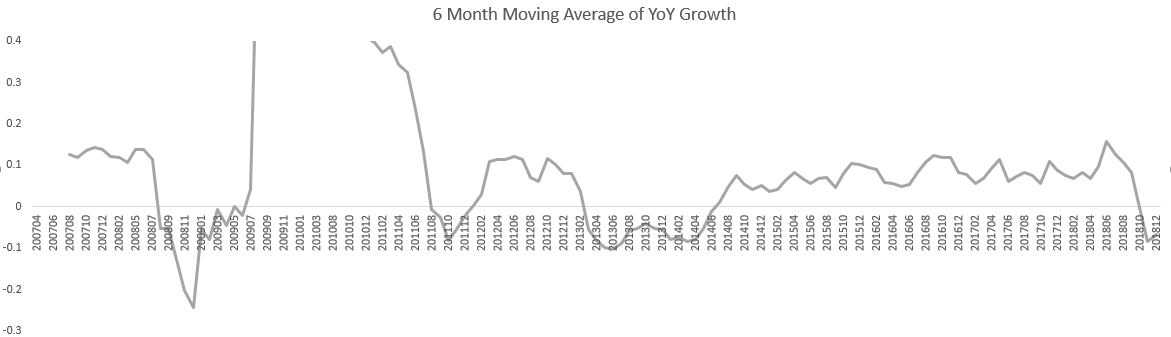

The recent auto slowdown is bring touted as 1st time phenomenon. Media making most out of it taking to another level. Below is 12 year monthly YoY growth of PV sales chart at 6 month moving average to make it smooth. As u can see, 1. Happens every few years with poor macro specially during poor macro financial situation 2. Longevity of correction may last from 6 to 24 months 3. Around 14-15% growth for 6-12 months , tops r created 4. Poor financial macro always played around fall. 5. Even the best of businesses could be semi cyclic ,so look to history. Every cycle has new narrative 6. Also, seeing the width and depth of correction, one can interpret about bottom formation

I think we need to factor historical behavior to arrive at normalized growth rate, normalized margins, valuation band at peak of optimism and pessimism and where we are comfortable at and then look into latest developments like EV, Shared mobility and factor in how future could be different from history to make best judgement

Data Source: Aceequity

5 Likes

When i checked the Annual Report this information is scattered. Where did you get the exact figure from?

Sheet looks good. Is this an Automated template? or you fill in the details?

Automating a valuation is the worst thing someone can do. Yes, I do fill in the Numbers myself and the assumptions used are personal to me. This is a compact version of the model I’ve discussed here:

If you want more details, feel free to DM me. Let’s not derail this thread with an unrelated conversation.

1 Like

1 Like

Maruti is a Auto + EV Battery company. We need to think about them in 2020. If we think 2019, we need to think the value it is providing coming down from 10K to 6K. All the bad news is already in the price of the stock, which is why it is stable.

Bulls and Bears are fighting right now clearly showing that it is not going down even with bad news, and also we already got the ‘super-bear’ saying 3000-4000 price point. Usually, there is always an outside range-view-needed to call the CMP as the bottom.

Of course, nothing in life is certain, and it could go anywhere, but the probablity is clearly showing that CMP is the bottom and SIP buying is the BEST of the BEST approach.

Listening the shudown of plants etc is VERY positive. It is the best way to manage expenses, and not create inventory where the margins will go down. Also, they usually do a shutdown in June and that is coming also.

I would say, Maruti is a leader, new model coming out in Dec, Batteries will be a huge leverage, and of course, non-Indian buyers are still buying. Now, that election is over, and Rate Reduction is being talked about, this will really help. Aug to Nov will start to become a bullish timeframe from Maruti.

KKP

6 Likes

A small analysis on MSIL

-

MSIL Income Statement (Will explain the projections)

-

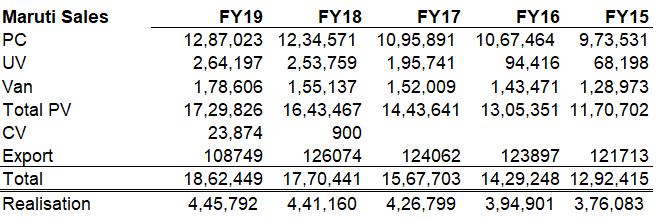

MSIL Sales Analysis

2a. Historical Sales

2b. Sales Projections

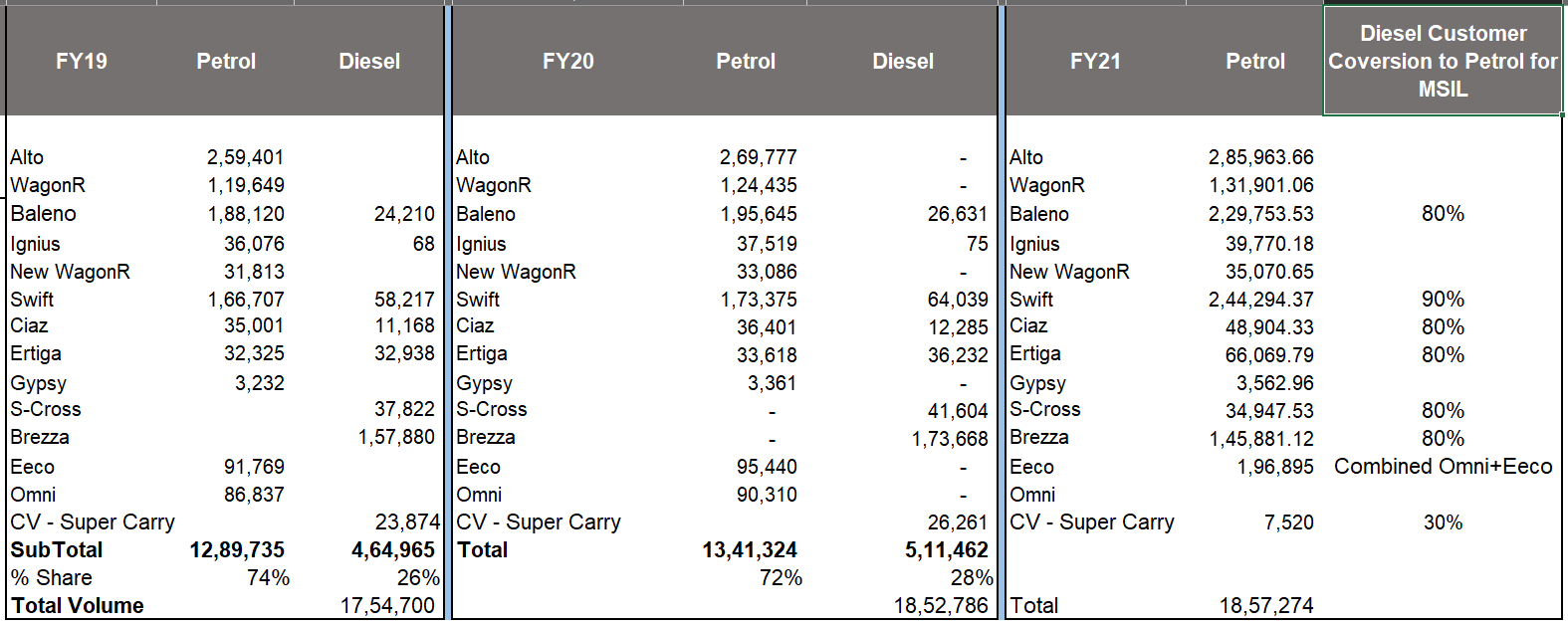

Petrol & Diesel cars growth rate for MSIL

Modelwise sales analysis

- Revenue Realization per vehicle forward looking

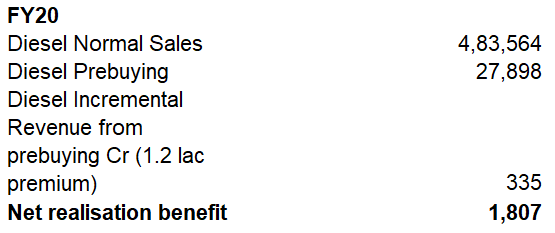

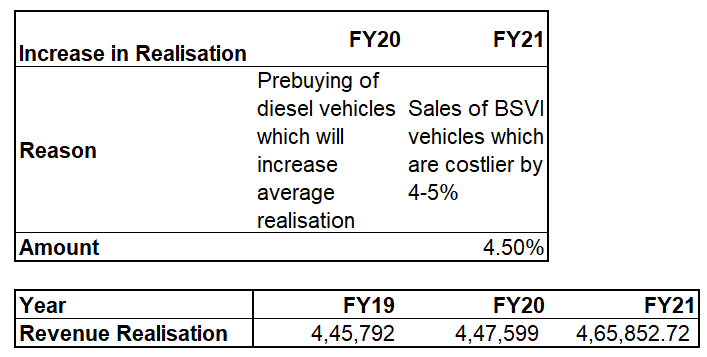

3a. Increase in realization on account of diesel pre-buying in FY20 & Increase in realization in FY21 due to BSVI price increase

-

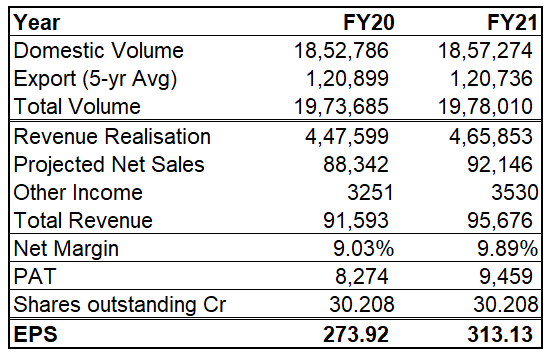

Revenue Projections

-

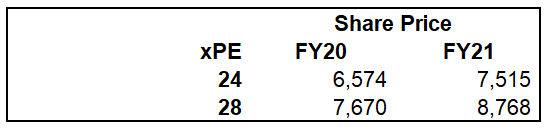

Share Price

Any views ?

1 Like

Share price prediction seems like a futile attempt as nobody can predict the multiples. Also the prebuying may not happen. Diesel growth rate may also be negative.

If you see current offers for commercial inventory, Uber and Maruti are giving special incentives for buying petrol (CNG/LPG) cars this month. Alto for example gets 60k cash back in 3 months.

Disclosure: I hold Maruti in my core portfolio and forms a very big %.

Leave aside share price, the main thing which I wanted to drive was, even if MSIL converts 80-90% of its diesel customer to petrol in FY21 still it can only touch sales levels which are at par with FY20 (if the growth rate is what I have assumed).

Also, Uber+Maruti petrol offer won’t affect diesel sales as Uber has either CNG (buy petrol & put a kit) or diesel vehicles, where CNG is available people invariably choose petrol/CNG. And currently Uber Cities + Good CNG network overlap is only in Mumbai & Delhi

Are you factoring in the growing aversion towards Ola and Uber due to abnormal pricing. I am noticing this especially in Chennai.

Disc : Invested 3.5% of my PF in MSIL

1 Like

I was referring to petrol + CNG/LPG. They are impacting sales of diesel for entry level based on my survey of fleet operators.

This is not true in some places like Chennai. Fleet operators now prefer diesel over LPG/petrol.

Its the case for every non CNG city. Chennai doesn’t have CNG.

Nice efforts @uditvd

Mind explaining how you arrived at growth rate of petrol and diesel car sales to be 4% and 10% respectively?

This looks quite stretched looking at the current slowdown.

I’m personally expecting a de-growth of 10+% for FY20 on the number of car sales. Important to note that there is slowdown in many sectors and not just Auto.

De-growth in car sales might lead to de-growth in margins too due to operating leverage. And if both revenues and margins are going down, it can lead to de-rating of the stock too.

We can already see that margins have fallen in FY19 and so did PE Ratio of the stock.

Disclosure: It is an excellent company but doesn’t look like a good time / price to enter. I’m quite bearish on the stock for the next one or two years. Not a buy / sell recommendation. Just presenting personal views. Not a SEBI registered analyst.