Company’s replies on diesel phase-out scenario:

Regarding the contract agreement with Suzuki Motor Gujarat (SMG), the management has explicitly mentioned that only cost-based manufacturing would be charged to MSIL and the chairman - R.C. Bhargava has appreciated Osamu Suzuki on this regard in AR FY14.

However, no terms were mentioned about Li-ion battery manufacturing plant.

Who will gain the margins of this plant? Is it going to be SMG or MSIL?

Are we sure that this is also going to be cost-based manufacturing?

Also minority shareholders can’t really verify if SMG is selling the cars to MSIL at cost and not booking profits.

Having said that, Royalty / Revenues is decreasing YoY for MSIL which is a good thing.

| 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | ||

|---|---|---|---|---|---|---|---|

| Royalty | 37672 | 38480 | 32443 | 26575 | 24863 | 24540 | |

| Revenues | 840869 | 796060 | 665861 | 516664 | 452811 | 451345 | |

| Royalty / Revenues | 0.044801 | 0.048338 | 0.048723 | 0.051435 | 0.054908 | 0.054370 |

The sales network has increased rapidly over the past decade and at a much higher pace than the sales.

This implies the dealers are not making that much money which they used to make a decade ago.

This can shun away prospective dealers from working with MSIL as the feedback they receive from new dealers who joined MSIL just few years ago might not be great.

| 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | ||

|---|---|---|---|---|---|---|---|---|---|

| Domestic Sales | 1653500 | 1444541 | 1305351 | 1170702 | 1053689 | 1051046 | 1006316 | 1132739 | |

| Sales Network | 2627 | 2312 | 1947 | 1619 | 1310 | 1204 | 1100 | 933 | |

| Sales / Showroom | 629.4 | 624.8 | 670.4 | 723.1 | 804.3 | 872.9 | 914.8 | 1214.0 |

Disclosure: No holdings. Not a buy / sell recommendation. Not a SEBI registered analyst.

2 Likes

news update

Could it be a game changer just like Maruti True Value . Although Maruti has joined the race of dedicated focus in areas like mobility, EV (electric vehicle) little late as compare to it’s peers ,as Hyundai invested i OLA in India’s biggest cab aggregator, Ola.in March . The move is appreciable but how good time will tell .

some good moves

Company is saying that it is using some cost cutting measures .Does it means even after long years of manufacturing there were not able to recognize these measure .HARD to DIGEST …

How the Company will write offs the large investments in diesel engine plants over the years it will be interesting to see . In my Opinion the price will slide more on account of this .

Also company admit that there will be less demand in yr 20 .

The Next question is about the Suppliers and vendors which are / were supplying the components for diesel cars may have huge inventory at their disposal can push the company in the Corner for compensation or some kind of negotiable deal .The Cost of components may rise . for every new vendor it will take 3 to 4 years of development period .If they source out new It will increase the cost .

Des ; Not invested but certainly the company is in watch list .The vies are personal and should not be consider as a suggestion for BUY or sell .I am not Sebi approved analyst

2 Likes

For Maruti, all of the good and the bad news are going on for a while, and the stock has had a great sell off.

For the value investors, it might be time to start adding at the rate of 10 to 100 shares, and then keep on SIPping. This will just get an investor into a powerhouse car manufacturer that has a good market share, mind share and also lots of past success. Lot of shops cater to repairs, support and OEM parts for Maruti. In addition, partnership with Suzuki, and now Toyota, plus getting out of diesel, will lead to the company becoming stronger coming out of this ‘auto recession’.

These supporting elements around the ‘car manufacturing’ is key and add to this that the average buyer is coming in from an era that has never had a car, and now can afford to upgrade cycle to motor cycle to car.

EV will coming in 2020, but a slow move to migrate to EV will allow the consumers to get into a car. Add to it that fact that it has beat Tata Motors in many categories, will have a new model out by end of year, and also the lessons from the 2018 and 2019 slow-down will make this company strong in 2020.

Support levels are really working for now, and hence it is a great choice for patient and disciplined investors to get into this company.

KKP

2 Likes

Buying Suzuki motors looks like the best solution for all the scenario’s , PPFAS has some great videos on both auto sector and Maruti which you can check.

2 Likes

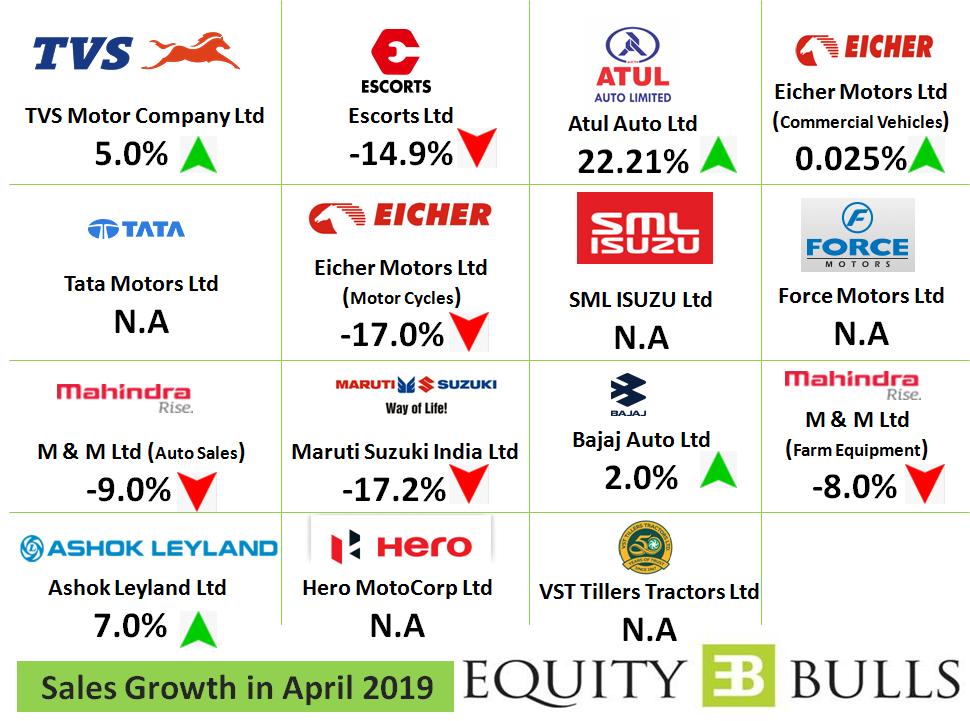

Y-O-Y sales down 20%

Hi

Just sharing the data on the sales. I am not a 100% on the April 2019 figures for a lot of manufacturers but still going ahead and sharing. Honda is a positive outlier in the month of April 19.

Rgds

2 Likes

Hi Deepak,

Since you have been tracking Maruti for a very long time,want to know your views for the reasons for auto slowdown and how earliest are the chances of revival.

In my opinion(I might be wrong to analyse), there are few factors which are cumulatively creating headwinds for the sector:

- BS VI upgrade: the buyer is confused whether he should wait till some clarity comes, thus not buying now

- Disruption due to ola and uber - which I dont think much impact, given that they are only present in few cities and further, they have increased their rentals too much(so no more affordable)

- Insurance costs have gone up (3 yr insurance etc)

- Car financing issues due to NBFC funding crisis

- Election time: people usually defer buying after elections

Are these the reasons or something else for this fiasco?

5 Likes

Adding few more plausible reasons to the counter.

- We have been seeing a bull run across the country since a long time. Possible that consumers have bought too much stuff (not limited to cars) on credit / loans during the happy times and are now loaded up with EMIs to pay back. So there is a drop in affordability / spending.

- Heated traffic in cities is causing car rides to be stressful but not enjoyable. So consumers are not super keen on upgrading their cars.

Personally, I bet the most on reason no. 6 among all the listed till now.

5 Likes

I just paid my insurance and I just paid for 1 year (both comprehensive and third party) and the insurance that I paid was less than what I paid last year.

Everyone is giving reasons of the slowdown in auto, but is it possible that the current slowdown in auto is just the cyclical slowdown that happens in auto sector every 4-5 years?

2 Likes

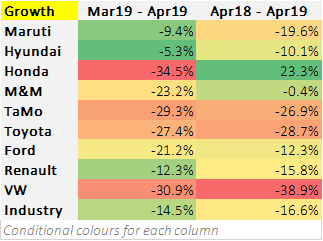

The reason for Honda sales to grow 23% as per Honda is “HCIL’s April sales growth is primarily due to the lower base effect, as there was no Amaze in the corresponding month last year during model runout.”.

M&M did reasonably well but it is also due to new models like XUV300 and Marazzo launched recently.

Hi @abhijain & @lingalarahul7

Let me share my opinion on the valid pointers you have jotted down. Though opinions are like armpits everyone has got one. We don’t mind sharing our opinions ![]()

We as investors, most of us individual small time retail investors, get bogged down with information overload. Just trying to play devil’s advocate here.

Please note what the financial media tells us. As they say ‘sab bhaav ke khiladi hai’ I dont know the Gujrati equivalent of this phrase.

BS VI:

How many of us know the current certification of our cars?

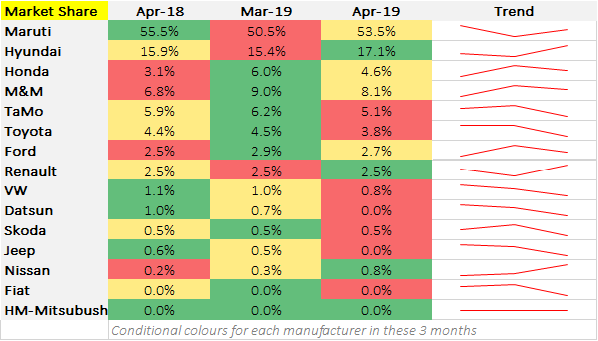

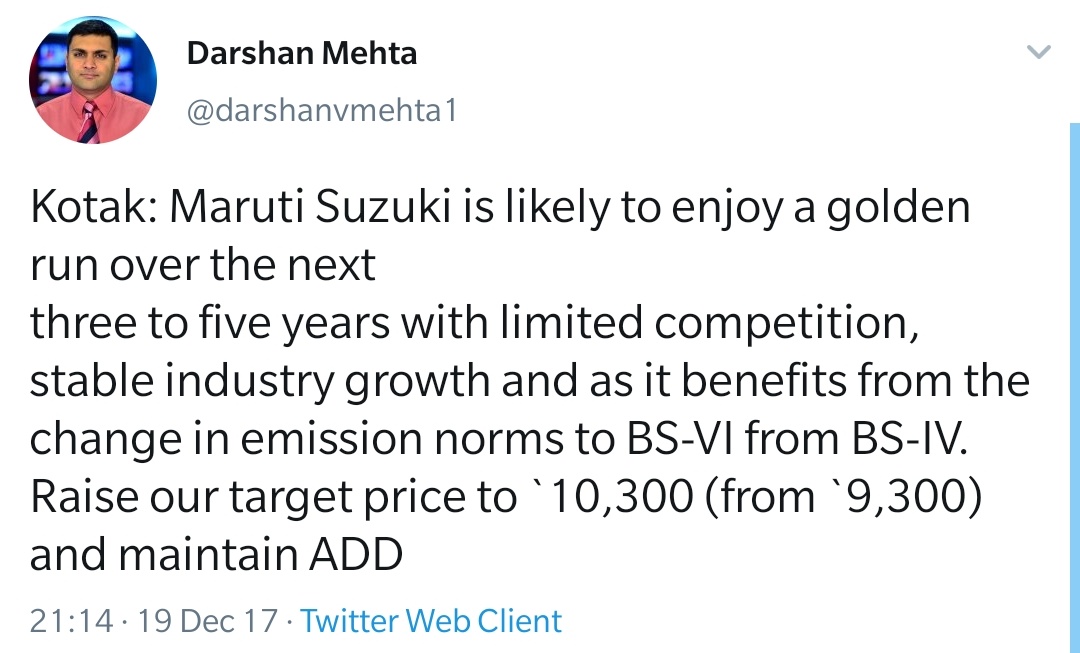

In the month this Kotak statement came in Maruti had lower market share than what it has had till today. None of the months since then Maruti has had a lower market share since Dec 17. The industry from this period has grown a mere 4 odd percent.

Ola/Uber:

How many of us know how many daily rides happen on Ola & Uber?

Most of the folks on this forum would be from NCR/Bombay/Calcutta/Hyd/Bangalore/Madras and would be recurring users of this service. So we have assumed that this behavior is prevalent in other cities. This is not the case. In Bangalore Ola does 4x of Uber. In NCR Uber does more than Ola. This is what I hear. Look at the investors in both Ola/Uber and we can try to guess what can happen next.

Insurance:

Do we defer purchasing a car if we have to pay 2000 more for insurance?

Customers I think have more transparent options on this than before. Though most of it happens via dealers. But have a look at a startup like Acko. Compare the premium you need to pay via them vs others.

Elections:

I think in the last 3 months someone from Maruti said this. I do not know the rationale of this.

Consumerism:

Do you have more credit cards than you had 3 years ago? Or a bigger credit line than before?

More goods/services today are bought by individuals on credit than it has ever been bought by consumers in our Indian history. Infact credit has never been so affordable for an average consumer.

Traffic:

How many of us pay Rs 175 for a 15 minute ride in a city like Bangalore?

Propensity to spend gives us the power to chose. And yes for comfort people switch to cabs. But its a fallacy to assume that whatever subset of consumers we are in the universal set is in that too.

Opinions aside lets look at Maruti and how analysts and financial media takes on a ride more bumpy than the stock price movements. Everything is retrospective it seems.

2017

April 2017

Maruti market share: 52.5%

Industry 10 month growth rate: 28%

December 2017

Maruti market share: 50.3%

Industry 12 month growth rate: 5.2%

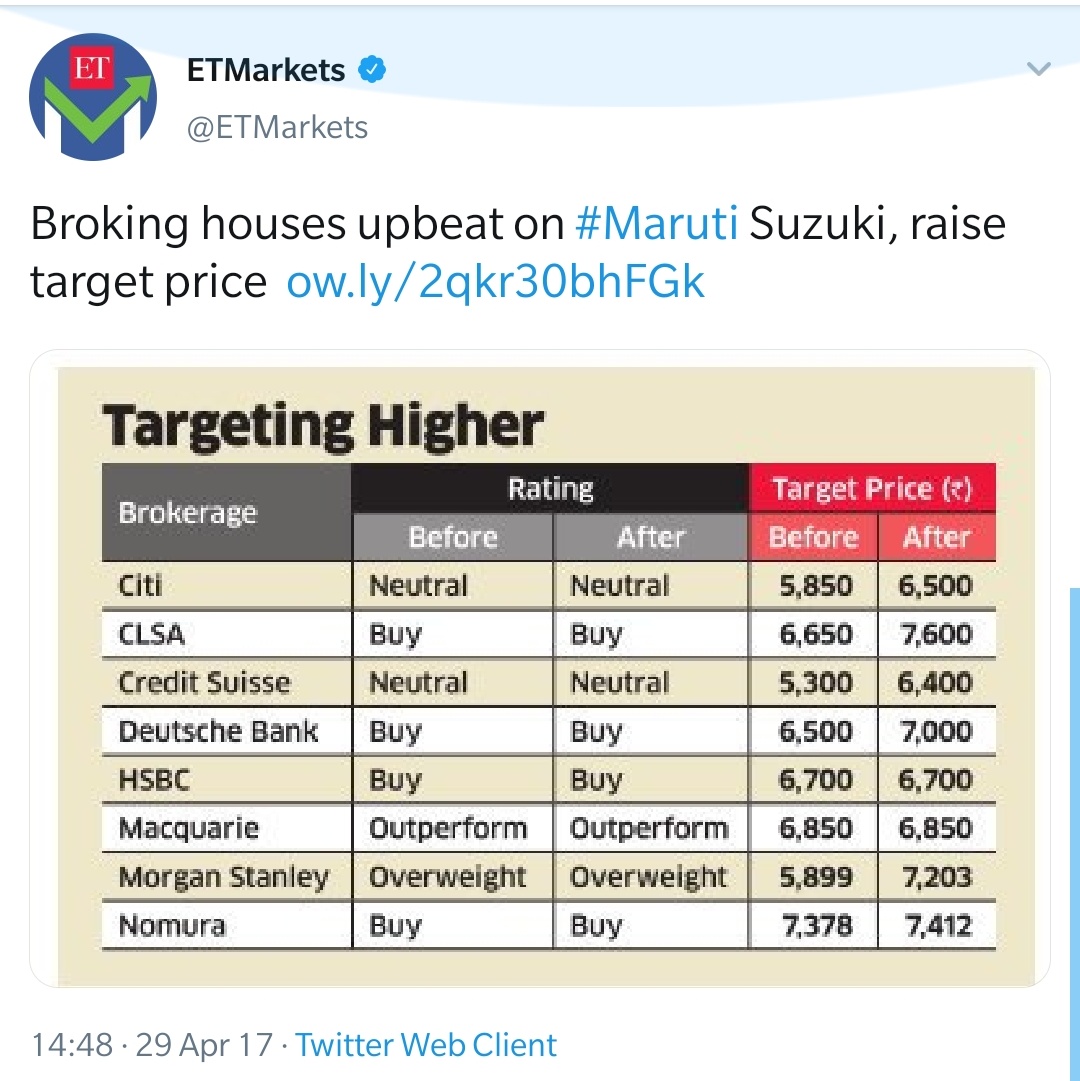

Price in this period had reached its peak of 9000 in December. Targets are over 10k.

2018

3 times in 2018 monthly market share fell below 50% in calendar year. Price again touched 9000 I think in July. Post July everyone starts cutting targets. Industry has slowed down to a mere 0.1% growth in calendar year. Maruti despite having 50%+ exit market share is growing at 1%.

2019

Price tanks in the year. Industry growth YoY in April 2019 is down 16%. Death knell goes off. Maruti still maintains one of the highest market shares it has 53%+. In the last 3 years this is still in the top 3 market share months I believe.

The question like Chirag has put is this Maruti screwing up (if they are so) or is the industry down in the dumps. The former doesnt look like it. The latter? If yes then shouldnt we be playing the game of catching falling knives ![]()

Regards

Deepak

13 Likes

I think the Gujarati equivalent is: “Bhav Bhagvan Che” … which roughly translates to “One needs to always bow before the market price”

1 Like

Thank you Deepak for this excellent analysis. Fact that you took time and effort to post the calls that were being given by the brokerage houses and analysts as events were unfolding and price was changing really put things in place.

It seems obvious that most brokerage houses and analysts are always behind the market price curve.

En-mass negative calls were given for the IT industry during early 2017. This is one example. But you will find dozens of such articles if you search for them.

We all want to buy Maruti at 6000 when it is at 9000. And when the price does come near 6000, we listen to analysts who are calling doom and gloom and stay on the side.

Maruti is just and example but sadly retail investors do this time and again for various sectors and companies.

7 Likes

If Buffett could go wrong sometimes, these analysts going wrong is not surprising at all. As far as my limited understanding goes, I would not think very high of the analysts who are young, they may have big college degrees but they haven’t got any experience, they are yet to see a 2008. Some of them may be good, but not all. I would give weight to someone who has been at the game for years. And when you are experienced you will know how to react, if at all should you react.

One who has considerable experience and presents a holistic analysis with facts and figures helps us very much. If not that, I would rather listen to someone who is experienced even if he does not present any data.

1 Like

By analysts I also meant brokerage houses.

Most brokerage houses have seen 2008 and 2000 but they too, run with the rabbits and hunt with the hounds.

3 Likes

I did some Fundamental Analyis and sharing below on MSIL

Statutory Warning: This is NOT an investment advice to buy or sell shares. Please make your own decision, as blindly acting on anyone else’s research and opinions can be injurious to your wealth. I do not own the stock, but my analysis can be biased, and wrong. The below is my personal analysis for Education purpose. I am not a SEBI registered research analyst.

Business Overview:

Maruti Suzuki India Itd’s: Principal activities of the Company are manufacturing, purchase and sale of motor vehicles, components and spare parts.

Automatives being a Cyclical business there’s seems to some decline in sales and MSIL has reduced its production. The company is partnering with Toyota in acquiring Battery technology and as part of the deals it’s sharing some of it top cars like Baleno, Brezza design with Toyota. Lately its planning to stop the production in Diesel cars by 2020.

Industry Wise (Porter’s) Analysis:

Competitive rivalry : Good Competitive Rivalry exists and MSIL stood on top but it needs to maintain the position.

Buyer Power : Overall there is not much control on buyers from Industry stand point.

Competitive rivalry, Buyer Power acts as Negatives.

New Entrants : It’s not easy for new players to establish very quickly. But Electric Cars and Automatic cars are one future technologies that needs to be looked carefully which MSIL has not yet ventured into. These can be disruptive technologies for existing companies.

Supplier Power : There seems to be not much of supplier power because most of the production is in-house. Engines is the only loophole as FIAT is the supplier

Threat of substitution : For people with a mindset of fuel economy, good service across India, After Sales there is not much of substitution exists

New Entrants, Supplier Power, Threat of substitution acts are Positives

Overall MSIL’s large service network, after sales and Fuel Economy are the main advantages. These cater to the Middle class needs and mind set of India. This acts as a MOAT (Narrow - because other players can replicate) for the business.

Observations from Annual Report

75% of cars sold in India are sub 4 Meters and less than Rs. 6.5 Lakhs at Factory level. Suzuki Motor Gujrat is ramping up capacity. Automobile business is cyclical in nature and capital intensive.

Automobile business is cyclical in nature and capital intensive.

Utility Vehicles Grew by 21%

Passenger Vehicles Grew by 3.3%

Passenger Vans Grew by 5.8%

Mini Cars declined by 2.1%

Diesel Models showed Weakness

Company is focusing on Localization of parts which is increase the Margins and production process.

Acquired 370 new Locations

It’s Partnering with Lithium Ion Battery companies for Electric Vehicles. It Partnered with Toshiba Corp., Denso and SIAM for EV’s.

It has great number of sales and service outlets in India

Balance Sheet Analysis:

Negatives:

Equity Share Capital was diluted in 2013.

Cash is less

Positives:

Long Term Debt/Overall Debt is negligible

Overall it’s a Healthy Balance Sheet

Profit and Loss Analysis:

Negatives:

Employee cost, selling and admin cost in increasing

Positives:

Top line sales growth has been good over the years.

Material Cost is reducing

Operating Profit Margins is Improving

Consistently paying dividends

Net profit improving

Overall it’s a Healthy P&L

Cash Flow Analysis :

Negatives :

In FY10, FY12 Cash required in Investing was more than Operating Cash.

Positives :

OCF in Increasing

Operating Activities is the major sources of CASH

Operating Cash Flow is Positive and Sufficient to cover CAPEX

OCF is higher than net income from FY10

Operating Activities are the major determinants of operating cash flow

OCF is consistent

Overall Cash Flow charts look good

Ratio Analysis :

Negatives:

Asset Turnover --> Decreasing

Positives:

Net Profit Margin --> Increasing

Financial Leverage --> Constant/Maintained

Overall the ROE average for 10 years is greater than 15% and key leverage component is maintained.

Valuation :

The DCF Value is Rs 4993 and with a Margin on Safety of 30% the ideal buying range is Rs 3495. So as per DCF the current CMP is not attractive

Reverse DCF: At the Current price of Rs. 7000 the Market is expecting a growth of 18% for the next 5 years and 13% after that.

Residual: With r at 12% and g of 9% the stock’s CMP of Rs. 7000 is less.

The EPV and APV combined is Rs. 4402 and the current stock price is 7000. So it doesn’t look attractive. But the additional Speculative Rs. 3000 must be for the MOAT existing with the company.

Overall the price does not look attractive at current CMP as per DCF and EPV Valuation methodologies. But as per Residual and EPV it looks attractive.

Management Analysis :

Positives:

Paying good Dividends

Shares are not Pledged

Remuneration of Management is much less than 1% of Net Profit.

Negatives:

The Equity Shares were diluted in FY13

Overall Management seems to have integrity and did not observe any frauds in my analysis.

Competitive Landscape:

The Competitive landscape includes a wide range of companies ranging from National, International Players. The Indian companies include Tata Motors, Mahindra. The foreign Players are Hyundai, Nissan, Renault, Toyota, Honda. Below picture shows a brief of the Market share in India

Peer Comparison:

Risks :

Employee Strikes

Employee cost increasing

Global Economic slow down

Investment Decision

POSITIVES :

Narrow MOAT Business

Healthy Balance Sheet

No Cover-up’s and Shenanigans

Management Seems to be good

NEGATIVES :

Not much power on Buyers

Competitive Landscape is high (International and National Players)

New Technologies like Electric Vehicles, New technologies of CARS can lead to disruption.

Price seems to be a little on the higher side because the market is accounting for Growth.

The ideal price Range is Rs. 4000-5500 as per DCF. But since it has some MOAT (especially of Scale and Brand) some price can be added to it. Since the industry seems be on downtrend and MSIL is preparing for future (Toyota partnership), I will wait for some more time and the stock in watchlist.

8 Likes

- what are you assumptions for the DCF

- can you explain what are these residual, APV and EPV calculations?