Yes, it is a SAFE EPS Story with Really Good Management.

Hi Yogesh,

I completely agree with your view point. Increased contact of Bank and customers is inevitable, going forward. Also, since banks are likely to be more vigilant in granting loans, the credit worthy customers are more likely to avail loans from these banks - Customer gets better int rates & banks get better creditworthy borrower - Win-win for both.

Hence, Manappuram is more likely going to have a low creditworthy customers.

The question we need to ask is - whether it is operationally feasible for Banks to enter the gold loan business given the (a) Avg ticket size being 30K to 40K (b) Having locker facilities at the branches for storing gold & additional security © Loan valuation officers to check the gold purity etc…

Specialized gold loan companies have always survived competition for these reasons - which appear to be valid.

I guess time will tell.

3 Likes

I think this product can be a very good offering which can be marketed to the middle class segment of India. Getting safety lockers is quite painful and cumbersome (as experienced personally). From what i have understood from this information mentioned in the annual report (correct me if i am wrong) is that a customer can store gold in Manappuram branch and he gets a loan whenever he wants. Its not compulsory to take the loan, but if you want it can be available easily. So a customer is getting both a depository service (dont know if they charge you for just keeping the gold and not taking the loan) and loan is easily available using an app …How many people depositing gold end up taking a loan is a question mark for me right now… But if it is really convinient as what the company is projecting then I think there will be quite a few takers for this …

Thoughts and alternate opinions are welcome…

2 Likes

Not many. Those that are financially savvy will not borrow at 25% regularly.

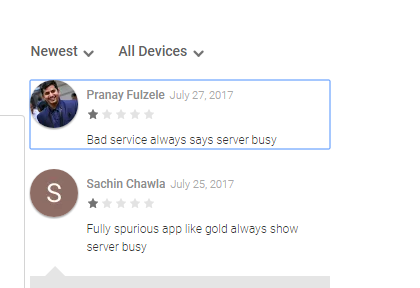

I think we should look at the technology side more holistically.If you just visit the App Store and see the latest ratings and comments, you would have a broad idea about how is the technology story unfolding. If you go through multiple comments, user are facing lots of issues with the application - one being server always busy. App depends on customer stickiness, and post that a financial application where customer would log in once a while needs to have a better feedback. All said and done, there are multiple questions like - How many customers are using the application? Is there any change due to the same if noticed?

Gold and MFI loans serve completely different purpose.

- GL is for discretionary/one-off spending like family events, Start of the year school supplies/fees, festivals and any other emergency requirement. Gold is poor people’s credit card.

- MFI loans are given to women borrowers for income generating purpose only.

- One cannot get a MFI loan right away like GL. The process to find/join a JLG, go through training etc takes many weeks.

1 Like

Agree.

The cost to source MFI loans is extremely high. MFIs keep the tenor of the loan from 12 months to 24 months to justify the expenses incurred and generate sufficient returns.

Gold loans are for relatively shorter tenor with an option for rollover. The marginal cost to source gold loan is low if the financing company has existing branch network.

MFI loans are for income generating activity; gold loans may have multiple end uses including lifestyle / discretionary expenses.

Regards

1 Like

Sustainability of Gold loan business

I talked to a banker. He told that he would give loan against gold within two hours. I asked if he would give Rs 10000 ? He immediately clarified that bank would never lend this much little amount as cost incurred would be more. As per him bank will not entertain any gold loan below Rs 50000. It is the stage where NBFCs start to find there niche areas in spite of lot of banks. So the business model is intact, sustainable.

14 Likes

Some early signs that all is not lost for MFI biz. Rating agency CARE seems to give it a thumbs up.

My key takeaways from the AR FY17.

- Competitive landscape will be benign going forward.

“BANKS COULD NOT CAPTURE AND HOLD MUCH OF THE GROUND VACATED BY THE GOLD LOAN NBFCS.” Similar to new NBFC entrants, new private sector banks that entered the gold loans segment also reduced their focus on the segment during FY13-15. During this phase, the relative inexperience of the new entrants to operate in the gold loans segment was exposed. The larger entrants such as HDFC Bank and ICICI Bank also experienced a reduction in their gold loan portfolio during this period. However, during the first two quarters of 2017, these two banks have shown signs of renewed interest in Gold Loan segment. Their continued focus and sustainability in this sector can be gauged only in the times to come.

- Growth Outlook - The gold loans market is expected to regain ground even as the growth rate is expected to be lower than that experienced during the period of rapid expansion (FY07-12). The Gold Loan market is expected to grow between 13-15% over the next three years from FY17-20 and reach a market size of ` 2,100-2,250 bn by FY20.

Over the next 2 years, Specialised Gold Loan NBFCs are well positioned to grow and reclaim their lost customer base from banks and the unorganised sector. The overall regulatory environment is currently neutral for Specialised Gold Loan NBFCs and expected to continue to be stable. Further, competition from banks can be expected to be subdued as public sector banks grapple with a weak credit demand and stress in their asset quality. Going forward, the market share of gold loan NBFCs is expected to increase steadily for the next two years.

5 Likes

But for a lending institution with some collateral than nothing to recover the amount . MFI and gold loan both cater to almost similar profile customer but gold loan cos have a security while MFIs don’t have it .

Well, I will add few points on MFI vs. gold loan origination. We think ordinary folks are irrational to apply for gold loans when they could get an MFI loan. Largely there are two types of borrowers in the gold loan segment. One, who is in absolute distress and need immediate liquidity. And second who has a very lucrative biz opportunity but no credit history or bad one to approach other financial institutions. e.g. one good second hand CV is up for sale in the neighborhood or somebody wants to buy a cow/buffalo calf. Our maid took gold loan to buy second hand furniture for a quick flip as she had a ready client. If the loan is for starting a biz, it gets refinanced by MFI / NBFCs later. So high cost loans are for very short duration say 3 months while they continue to generate 20-25% ROI for the full year.

1 Like

Hello,

My management posted a query - as to why Manappuram is trading at a discount to Muthoot Finance, inspite of the superior ROA & ROE posted by Manappuram. They asked me to dig deeper into the stats - for the past 12 Qtrs and compare them on parameters like NIM’s, Opex, Gross & Net NPA etc… I did the statistical analysis (all of it sourced from the Qtrly presentations / Concalls posted by company on their websites) to compare them and found no reason for Manappuram to trade at a discount to Muthoot. May be there is something amiss and needs deeper thinking. I am attaching herewith my analysis and would really appreciate community’s comments - Is the valuation gap justified or is the market pricing them incorrectly?Comparison of Muthoot Vs Manappuram - 2nd Aug 2017.xlsx (47.4 KB)

14 Likes

@ronak Price to earnings of Muthoot is 15 and not 22

price to book 2.67 and not 3.3 for muthoot am i reading anything wrong here? report states different figures.

I think figures entered in excel for PE and price to book is of Muthoot capital services

Please correct me if I am reading it wrong. Thank you

Hi…seems you are looking at standalone numbers for Muthoot finance…pls

check the consolidated stats…u need to click the consolidated tab and

then check the stats…

1 Like

Good comparision ronak,

I think part of the discount given to manappuram is because of the fact that muthoot is a bigger player with higher AUM, and more in terms of all other parameters. And even if the gap might not be too big to warrant such a disparity in valuations of both companies, usually markets do tend to give higher valuations to what it perceives to be the market leader.

Plus one difference I found in both cos was in case of muthoot, promoter holding is much higher at 73% as compared to manappuram’s 34%.

Both stocks have given a breakout and are quoting very close to their all time highs. I think valuation gap would remain for some more time unless manappuram demonstrates higher growth as compared to muthoot. These kind of valuation mismatch can often change within a few days as market is at heart an animal with big mood swings.

19 Likes

One of the reason could be 12% of Manappuram loan book is MFI which market perceives to be risky. Moreover, This can easily be offset by the fact that Manappuram loan term is only 3 months with 75% LTV. This ensures in case of default, both principal and interest can be recovered by auctions where as Muthoot’s 1 year loan can result in loss of some interest component.

I personally believe this gap will close down once Manappuram MFI loan book goes back to pre-DeMo NPA levels and HFC segment starts growing at a faster clip.

7 Likes

Also MFIs are reporting high NPAs, provisions derailing the express trains on this track. Examples are all MFIs like Ujjivan, BFSIL etc.

Disclosure- Invested.

2 Likes

Concall highlights:

MFI:

-

state risk wise south and east r better. karnataka , maharastra, up and haryana r high risk states n would reduce exposure.

-

south and east : 60-70% portfolio. formulated from april and following it

-

1235 crore till dec.balance is 600 crore :12% on that under risk which provisioned.

-

Most of NPAs have been taken care of and do not expect any major shock going further

-

Disbursements mode post Dec has 100% collection efficiency

-

chance 10-15% provision may come back

-

Provisioning is approx 33 crore above RBI limits and have not taken any RBI relaxation

I could not hear few points properly interms of 60 day NPA vs 90 Day NPA

Gold Loan

Was not satisfied with answer on why gold loan AUM is decling and why future looks good. There was no concrete answer for visibility

Security Charges:

security charges increased due to additional guards and additional time window for guarding. Looking for ways to redcue

New leadership hired to expand home loan business.

Got rating upgrade. With lower cost of funds and leveraging branch network and newly hired seasoned management, expect to grow home loan business

Q1 Result key concerns:

- MFI losses looks like provisioned but a 10% hit on book every 5 yeasr should be risk norm for a MFI

- Bigger concern is 3rd consecutive quarter of AUM fall and somehow did not find managements answer very convincing. Not sure if it is due to heated up competition or demonetization effect continuation or market saturation. Any views on this point?

6 Likes

@suru27, thanks for taking efforts to post updates here.

I have been hearing this from many lenders for last several quarters and every time they say this is a one and done deal only to come back later with another big hit on the bottom line. Banks mastered this art with terms like watchlist to take the focus away from the plain old non-performing assets number. Now its turn of NBFCs. Every quarter there is some excuse. Next time it could be GST.

Like Yogi Berra said, it ain’t over till it’s over.

3 Likes

Same here…found the management arguments very uninspiring and the investor presentation makes for worrying reading…did anyone understand whether the security charges are going to be in similar range every quarter or was this a one off thing…the main thing in the stocks favour is the inexpensive valuation

Disclosure: Have a small position in the stock