That’s an interesting observation ,not sure if it holds for long term. So, apart from growth, debt, return on capital etc etc, float can ve an impact on PE. In long run too any quantifiable experience ?By long I mean over 5+ years

It should not matter in the long run but consolidations will last longer. It is about plain demand and supply in the short term. Number of shareholders is much higher in case of MFS vs. Muthoot so much more number of folks need to get convinced for its upmove. I also suspect many global hedge funds take position in gold loan companies as a hedge against many other positions. so no option but to wait and not sell out of frustration.

4 Likes

Manappuram has been consolidating slightly below its all time high range of around 106. It will need a big push or trigger to cross the hurdle. My guess is if q1 fy 18 results are good esp in terms of NPA, market can give it a thumbs up.

It was shaping up to form a cup and handle but now with such a long consolidation, the handle itself has become as long as the cup. Let see how it plays out.

disc: invested.

15 Likes

Hitesh bhai , is not it like the last attempt few months back with a cup and handle pattern did not succeed but now the its more of a ascending triangle pattern ? Last week I thought gold deposit may act catalyst but did not happen. So, ya results look next possibility. Good part is in last few days it has not gone back to 96 which reinforces ascending triangle is still playing out n wow volumes too have increased

Disc :Invested

In the other type of NBFC’s the customer borrows for a productive purpose or for discretionary items like cars etc. Can someone tell me what do gold loan customers take loans for?

Sorry if this is already discussed.

Saurabh,

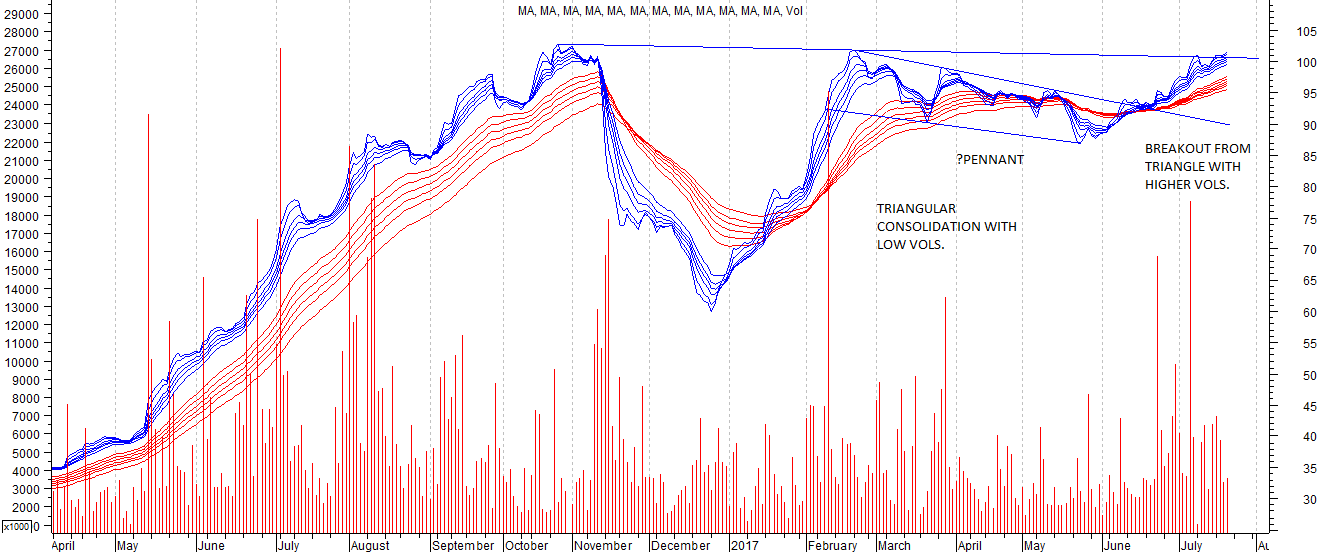

I have used guppy moving averages in the attached chart where the lines in blue represent short term moving avgs viz. 3, 5, 8, 10, 12, 15 and in red is longer term moving avgs viz 30, 35, 40, 45, 50, 60. This tends to reduce the effect of whipsaws and is often very useful in spotting patterns like cup and handle, flags, pennants etc.

Besides the obviously visible cup and elongated handle, there was a possibility of a flag like pattern where instead of a flag there is a slightly triangular consolidation in form of a pennant. At the time of breakout from the pennant, volume features have been as per the requirement of pattern. There is a dip in volumes within the consolidation phase and once it broke out there were a couple of big volume days.

Distance from the bottom of pennant to top is 100-60=40. Add that to breakout level of 92, we arrive at a potential target of 132.

In fact I quite like this tight consolidation in a tight range. Its like a spring coiling tightly. It would be interesting to see what kind of moves we see if and when 106 kind of level gets taken out.

15 Likes

Thanks Hitesh bhai for explaining so well with chart.

Hello Guys,

I recently presented my work on Gold Finance Co’s to my Investment team and got some real good insights on the same. I was pitching for the idea to invest in Gold Finance Co’s - especially Manappuram and highlighted the positives for the company. You may refer to the attachment for the detailed note. My basic hypothesis was - since Gold Finance Co’s have a secured book with Gold as collateral - they deserved to valued at par or better than their Micro Finance peers - which cater to the similar target audience but run an unsecured book. While this point was accepted - they argued against it citing the following reasons.

-

Scalability - Since the avg ticket size of the loan is 30K to 40K, scale of operations have to be high to maintain profitability. - Now, since the target audience is at the bottom of the pyramid - increased scale would happen only through incremental penetration - More branches. Repeat borrowings at rates in excess of 18% - 20% p.a. are very risky - as few business can earn ROE consistently above this level. Even if one assumes ROE are high - say 30% - the lender takes away a bigger chunk of the earnings (18%) vs owner of business who earns 12%. Not a win-win model. Importantly, Banks though with stringent norms would offer loans at much favorable rates. Net-Net, Loan are unlikely to be repetitive for the aforesaid reasons - hence loan would ideally be to new customers

-

Credit Profile of the borrower & it’s end use - Primary target audience is at the bottom of the pyramid - very low credit profile - and end use of loan is not always to increase business - but to meet some urgent need (medical / marriage). Now think about this deeply - you are effectively giving consumption loans @ rates in excess of 18% 20% p.a. to a sub prime borrower - recipe for default. One may argue that the loans are secured by the gold - but as a lender, you want to earn income not by auctioning the collateral, but by the borrower making an regular payment.

Would appreciate more comments on these

Gold Loan Companies.pdf (936.2 KB)

18 Likes

Excellent preparation on gold loan cos.

Regarding point 1, you assume the lender takes away a big chunk of money as compared to owner of business. But in case of manappuram and even muthoot, isnt lender and owner of business the same guy i.e the company itself?

Regarding credit profile of borrower as mentioned in point 2, its always risky at the bottom of the pyramid but as compared to MFI, gold provides some sort of cushion in case of defaults. But in a normalised scenario as per the NPA figures provided by the co the default rate is quite within limits.

I think the small size of loans is exactly what gives these companies the edge over banks. I cant imagine a bank officer going all out to market loans with a ticket size of 30-50k. They would always be interested in doing higher ticket size loans of vehicles or personal loans or consumer loans or HF besides corporate loans.

The main competition for them would be from unorganised players and that will always remain.

I like the move by Manappuram management to shorten the loan tenure which can act as a big risk mitigator.

Both companies are quoting above or near to their all time highs and seem to be in the process of climbing the wall of worry after which fireworks can begin.

10 Likes

Hello Hiteshbhai,

Appreciate that you liked my presentation.

On point number 1. I was referring to a borrower making …let’s say rickshaw driver… He borrows money from Manappuram taking a gold loan at 20% rate p.a. and runs a rickshaw. What would be the roe of the rickshaw driver… 30%…on his investment of Rickshaw. Now if he earns 30% and pays 20% to Manappuram…he gets to keep 10%…only…Sooner or later he will realize that banks are a cheaper source n will migrate to them, once his credit profile increases…Hence, Manappuram will have the constantly mine for newer clients…and most of these would be of low credit profile…as like the rickshaw guy, they too will migrate to banks once their credit profile improves…Thus, sizeable growth for Manappuram will happen with higher branches…

5 Likes

Hi Ronak - fantastic work with presentation!

Assumption that gold loan is consumed only by poor is slightly misplaced. Rich borrow as much against gold for consumption. Refer the below extract from a article published in Mint few days back. Mr. Nandkumar has also spoke about how Gold loan has become a lifestyle product.

Quote

It is the richer households who are more likely to mortgage gold, the data shows. Only 4% of households in the bottom 10% income class ever availed of gold loan as against 13% of households in the top 10%. 14% of households in the top 1% households by income reported ever having taken gold loan.

The poorer income classes take gold loans mostly for medical emergencies or financial crises. As the chart below shows, the proportion of households availing gold loans because of such reasons is much higher among the poorer four deciles (bottom 40% of the income distribution) than among the richer income classes."

Unquote

Disclosure: Invested from lower levels.

2 Likes

This is a valid argument but typical Manappurum customer is not financially savvy enough to understand all this math nor he/she is going to open a savings account to park extra income. 30% interest on a 3 month loan does not sound that big. they look for absolute interest rather than % rate. For these kind of customers, gold is their savings account. Banks also does not have enough manpower to go after these guys to convert them into account holders. After all the push by the government towards jan dhan accounts etc, financial literacy has remained low. Many educated people I know haven’t even moved beyond savings accounts and fixed deposits.

I think rich borrow against property. LAP is the equivalent of gold loan for rich. That is now available at 12-15%. Many rich businessman prefer to borrow against their residential house at these rates which are cheaper than bank loans and they can still make money as their returns are higher than 15%.

6 Likes

One other point to ponder is that the rickshaw driver can also approach microfinance company where there is no need for collateral and the interest rate is very similar.

Manappuram has come out with its silver jubilee, 25th annual report. It’s a treat to read and provides insight into digital initiatives company is taking to tap future growth. Would highly recommend reading their AR.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=2d32cbaa-2e48-4a0b-9757-9088fad408f4

Excellent point guys… Your thoughts have made my thinking towards the company clearer. Now, lets together work to making a list of key monitorables / issues critical to business ofManappuram. Some issues which crop up to my mind are as under. Pls add up to the list, which will help us gain further clarity on the business.

- What is the impact of Peer to Peer (P2P) lending on companies like Manappuram. A friend of my asked me to lookup into Faircent which is an online portal - which allows the lender and borrower to list. It’s like an internet based market for lenders and borrowers to meet. What’s potential threat of such co’s.

-

Impact of Govt’s Mudraa Loan scheme on Gold loan Co’s.

-

With the increasing share of Other Businesses in overall portfolio - should not the NIM’s reduce - as Housing loan and Vehicle Finance are lower yielding business. Hence ROE’s would be lower. Also note, Microfinance would be yield accretive (or atleast not dilutive)

-

Loan waivers by govt have been instrumental in many farmers willfully defaulting on the loans. We are again approaching elections in the next 2 years - How has the company geared to avoid repetition of such defaults

Would appreciate your thoughts on all these issues

1 Like

Hello,

I just made an addendum to my report on Gold Finance Co. with latest available stats. Am uploading the same herewith. On the key monitorables, I have done some more research and my comments on the same

A. Govt’s Gold Monetisation scheme - It has not been very successful as govt has hardly put any efforts to popularize these schemes. 6.4 tons mobilized so far

- Onerous process of melting the jewelry, verifying the purity, obtaining the certificate from registered hallmark valuer and converting it into Gold Coins – not everyone would be willing to do that (certainly not the bottom of the pyramid customer – due to sentimental value). Moreover so because once you deposit the Gold - it is locked in for a period of 3 Years - hence these schemes are useful for those having excess gold. Hence not relevant for the bottom of the pyramid customer

- Very low int rates of 2% to 2.5%. These too were taxable, until recent budget which exempted the interest from taxation.

So net net - Gold monetisation will not have too much impact on Gold Loan Companies

Addendum to Gold Finance Co’s.pdf (226.7 KB)

6 Likes

Reading the latest annual report for FY 2016-17 makes me wonder if the turnaround story of Manappurum has prematurely ended and business model shaken in FY 2016-17.

Demonatisation has dealt a severe blow to manappurum’s customer base. While rest of the economy has recovered, as per the AR, working capital cycle of Manappurum’s customers have not got back to normal. That means we are looking at few more quarters of no or negative growth and asset quality issues.

Another interesting thought that came to my mind is about sustainability of gold loan business model. MFIs offer similar interest rates without collateral. Using gold as a collateral actually limits the amount that can be lent. To me it looks like Manappurum got into MFI business because it saw MFIs taking away its customers. Now if a customer loses it’s collateral in an auction, manappurum can lend money to the same customer as a MFI loan (they say they only do JLG loans but I am skeptical).

There is a lot of talk about adopting technology and using less cash. All that is good and that’s the way forward. But that also means now the customer has to get in touch with banks (either branch or ATMs). Banks can try to convert these customers into account holders or even gold loan customers. Banks will not go out and poach customers from Manappurum but they will be happy to make gold loans if a customer walks in.

Overall I think the manappurum has turned around and from now on this is an EPS story.

7 Likes

Yes, it is a SAFE EPS Story with Really Good Management.

Hi Yogesh,

I completely agree with your view point. Increased contact of Bank and customers is inevitable, going forward. Also, since banks are likely to be more vigilant in granting loans, the credit worthy customers are more likely to avail loans from these banks - Customer gets better int rates & banks get better creditworthy borrower - Win-win for both.

Hence, Manappuram is more likely going to have a low creditworthy customers.

The question we need to ask is - whether it is operationally feasible for Banks to enter the gold loan business given the (a) Avg ticket size being 30K to 40K (b) Having locker facilities at the branches for storing gold & additional security © Loan valuation officers to check the gold purity etc…

Specialized gold loan companies have always survived competition for these reasons - which appear to be valid.

I guess time will tell.

3 Likes

I think this product can be a very good offering which can be marketed to the middle class segment of India. Getting safety lockers is quite painful and cumbersome (as experienced personally). From what i have understood from this information mentioned in the annual report (correct me if i am wrong) is that a customer can store gold in Manappuram branch and he gets a loan whenever he wants. Its not compulsory to take the loan, but if you want it can be available easily. So a customer is getting both a depository service (dont know if they charge you for just keeping the gold and not taking the loan) and loan is easily available using an app …How many people depositing gold end up taking a loan is a question mark for me right now… But if it is really convinient as what the company is projecting then I think there will be quite a few takers for this …

Thoughts and alternate opinions are welcome…

2 Likes