Check out @geordiejob’s Tweet: https://twitter.com/geordiejob/status/1065850011315920896?s=09

1 Like

I work in Bhubaneshwar CGD and I can tell you that steel is required for high pressure pipelines. For low pressure and final mile connectivity MDPE is used. Further my company also manufactures petrochemicals so I can tell you that no company in India manufactures MDPE. Only LDPE and HDPE is manufactured by Indian companies because MDPE manufacturing requires some specialised knowhow.

11 Likes

1 Like

Niti Aayog-led panel mulls free-market pricing for all local natural gas

In my opinion, good for upstream players but could be bad for downstream ones!

3 Likes

Mumbaikars cant get enough of MGL. ![]()

On a serious note, this problem of limited CNG Stations might be holding back conversion rate of vehicles from petrol/diesel to CNG. People looking at those long lines at re fuelling stations will get discouraged from switching.

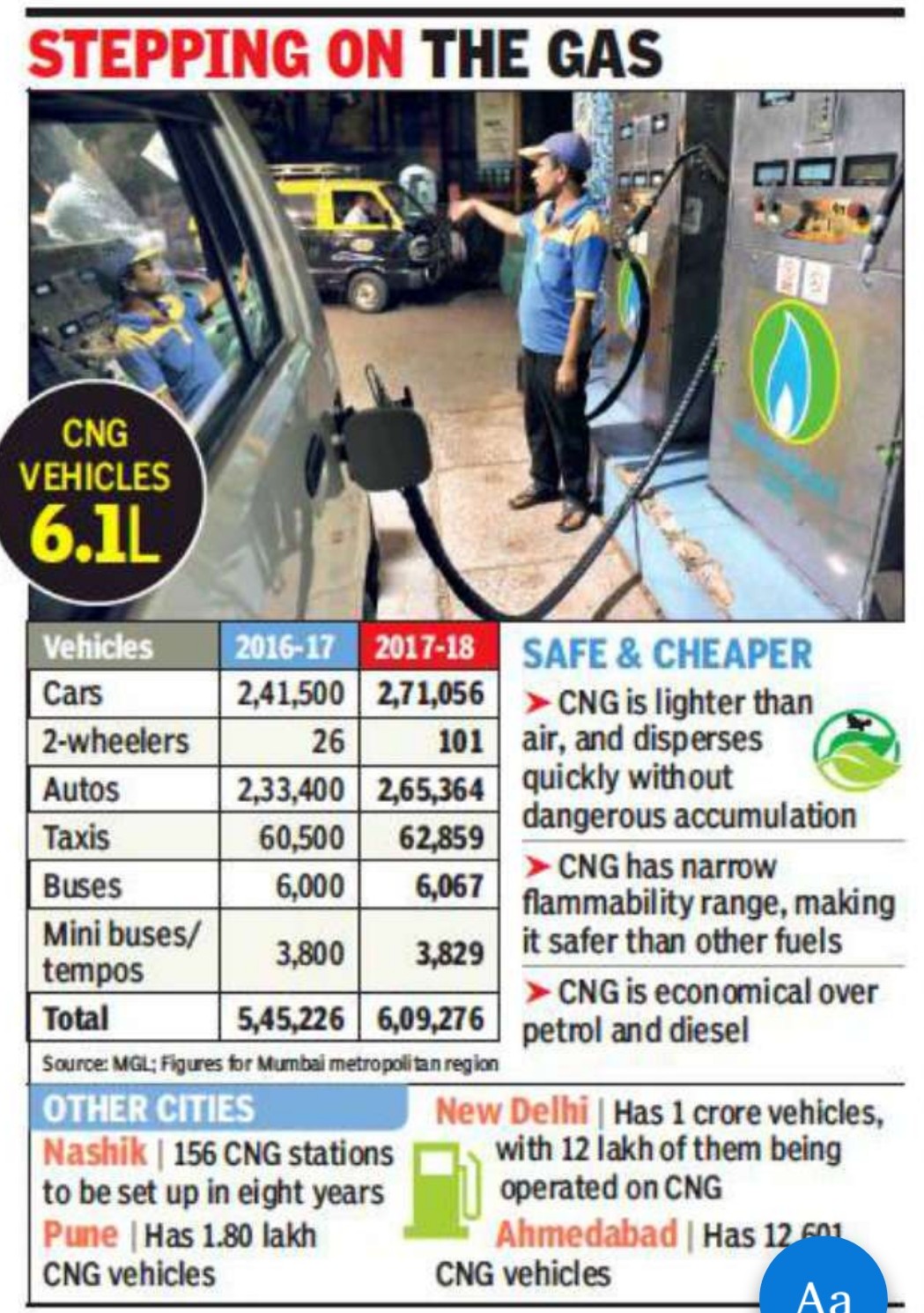

Came across this interesting graphic in TOI few days back which shows the CNG vehicle population is showing healthy growth for now:

In Q2’19 as well, vehicle conversion rate was 21000 vs 10000 in Q2’18 (source : Mahanagar Gas Q2 Results Light Up On Better Volume Growth | Mint)

This is the story everywhere. In Pune also i see almost 300-400 meter long queues of autos. Some auto drivers said that this is eating up lot of time and affecting their daily business.

3 Likes

Yes work is slow, progress is slow but it’s more linear and certain in my opinion.

MGL expects to add another 200K PNG connections for the full year FY19 & open another 35 CNG stations.

Reading about these challenges makes me compare them with the challenges Tesla is facing in the US - production targets being missed repeatedly, deliveries getting delayed with people waiting for months for their cars to get delivered etc. But the strength of the product is keeping faith of the customers intact for now.

Likewise for MGL I think ultimately development of the ecosystem will take its own time but once it reaches an inflection point, people will naturally get attracted to the product.

1 Like

Hi All, As per news spot LNG prices have reduced in December . I don’t see any news regarding reduction in cng prices in Mumbai. I think this would be a positive trigger for next 2 qtr.

2 Likes

@pk89 retail CNG prices are based on global benchmarks and are lagged by a quarter, so spot updown doesn’t affect to retail CNG prices that much as the average out

2 Likes

to be precise, it’s actually based on previous 6 month average. The next revision in the price would be in March

1 Like

Good set of results from MGL. 9.5/- dividend has been announced.

YoY performance:

Rev growth of 25.67% accompanied by vol growth of 9.79%

EBITDA margin at 32.46% compared to 36.69%

Net Profit up by 10.67%

Margin is probably down due to their inability to hike gas prices dueing Q3 as the crude prices were down during this period.

All in all, 10% vol growth is heartening.

Any thoughts?

10 Likes

The ~10% volume growth is a positive. Again, a 10% PAT growth for next 5 years, with a combination of volume increase or margin expansion looks reasonable to expect.

Regards

SJ

1 Like

Looks like MGL hasn’t bid for any city in 10th round ?

1 Like

Dear Sir,

I have observed that you are very active in discussion this stock. Can you please help me understand how the rupee/dollar exchange rate impacts the financials of this company?

Since i have been holding IGL for long which has done well and also have MGL which has not done so well, the main risk here is that it is government owned. Greater public good takes precedence over share holder wealth maximization. There is also a regulator called PNGRB who can put a spoke in the wheel. There was a period on uncertainty in IGL i think in 2013, when the regulator questioned the margins and the stock price went crashing. I think the price you have mentioned is a good price to buy MGL. A basket involving the three IGL.MGL and Gujarat Gas is also not a bad idea.

2 Likes

Regulatory risk is omnipresent not just in govt owned businesses but in Pvt ones as well. Look at how Pvt banks CEOs have been shown the door by RBI. Pharma cos are regularly investigated/inspected by USFDA etc. We all know about the whole Maggi episode which made Nestle suffer a lot. And then there are tax cases like the Vodafone one.

Govt can just swoop in anywhere and take the whole pie whenever it desires.

A strong business imo should overcome the adversity posed by regulators and emerge stronger just like IGL also has done. However, it’s true that these CGDs won’t be worth holding at current premium prices if regulatory price action (or introduction of competition) takes place.

1 Like

Dear Biju,

I think that it is important for me to check where there is value.

I also have been pondering for a while now, (in my short tenure in the market) about how investors/analysts underestimate terminal value of businesses.

-

The business generates free cash to large extent and pays out handsome dividends. (a high yield on this price)

-

The moat of the business is clearly visible. Can anybody else set up a network in the city of Mumbai economically today or going forward, esepcially considering the fact that MGL are also slowly expanding their reach and network. It is highly unlikely. So that means MGL have this cash cow in the mumbai area that still has significant room to grow in that region itself. This “moat” signifies that the business will most likely stay relevant for atleast the next 7-10 years.

-

The mgmt. is conservative to say the least. This is good in the case of this investment because we would rather have them exploit their existing GAs to their max potential and generate more and more free cash with a high return on capital rather than bid and expand aggressively.

-

The company trades at ~13x cash flow. It is quite cheap considering its growth prospects in its exisitng GAs, industry tailwinds, low penetration and high return on capital for the business. I see them as a cash cow for the years to come.

-

Since the business model and its assets will stay relevant for atleast another 7-10 years we could see a consistent compounder here.

-

And odds are in favour that after 10 years the business will still stay relevant. If that is the case and we are right on that front our returns could be magnified.

The EV thread on VP was started in 2015. We are almost 5 years ahead now and we still do not have one fully integrated charging station in the country for commercial use (to the best of my knowledge)EVs will first begin to take over developed markets in my view. EV is a long term story not a 5 year story. EV in my eyes is a 20 year story. Even if it happens sooner in say 5-10 years and in a big way at that, we arent paying too much for MGL. The business will have decent terminal value. Plus nothing stops MGL from putting up charging stations at their locations as well.

Anyway if EVs become big, our electricity needs will also grow and India will move from coal based to Natural gas based. So this might end up being a boon for the Natural Gas industry as a whole. And then the use of Natural Gas in various industries listed here https://www.mahanagargas.com/business/type-of-industries.aspx There seems to be a long way to go for the industry. (correct me if im wrong on this please)

I think MGL can deliver index beating returns over the next 5-7 years. (that is 15% plus cagr incl. dividends with low downside)

Would love views of experienced members as always.

9 Likes

The business model is sort of a local monopoly. We can see that in the FCFs. I am invested in, for similar set of reasons

I would prefer them to expand in few more areas. Not participating in some of the recent biddings baffles me. Can IOC or HPCL turn out to be a dark horse? I don’t know if HPCL can get a favorable pricing from ONGC after ONGC’s acquisition of Govt’s stake.

Nice analysis,

But I was trying to understand, why the company is not entering in to new geographies, Why are they so passive for bidding in other geographies… If they are not growing apart from normal growth in Mumbai and Raigad, I feel their PEG ratio is rightly relfected in to current market price.

So, as an investor, if I want my PE ratio to expand keeping the PEG ratio constant, I will need a good growth… Which I can not see in MGL as they are bidding passively for CGDs…

Also, can anyone share the CGDs won by competitors of MGL… That way, we can pick a stock based on forward PEG ratio instead of forward PE…

2 Likes