Read at the link shared by @AKGupta sir in this thread. It has details. IOC seems to have bid the most 35/50. Adani -19 own and 7 partnered with IOC, HPCL-24/50, Torrent gas -20/50, BPCL thru subsidiary-14, GAIL-10

While growth is good, but the question is at what cost? What will be incremental ROC and ROE for these geographies from even a 3-5 year perspective, or is better to grow at a steady 10-15 % for next 5-10 years with minimal capex in Mumbai and Raigad. While PEG is an important ratio…ROE and ROC are equally relevant. I personally liked the move of not bidding aggressively for the new geographies because of the uncertainty in the returns from these geographies. Groups like Adani bid aggressively as they need to keep entering newer businesses and keep expanding the existing businesses to raise new debt and manage debt at group level.

Regards

SJ

1 Like

Exactly…I personally prefer conservatism over aggressive make or break like business moves. Especially given that MGL is in one of the most densely populated place not just in India but in the world. Cities on offer are unlikely to offer better prospects than Mumbai for sure. Plus it takes years of development work in a new city before revenues start to flow from that GA…this limits free cash flows…

However, a couple of additional cities in the MMR adjacent area wouldn’t hurt.

3 Likes

An interesting aspect in this business is population density.

Higher the population density of your GA, higher will be your RoCE.

Because if population is closely knitted like in Mumbai or Delhi, less km of pipelines would be needed to connect lots of customers (residential / commercial / industrial).

So expansion in Raigad might not come with the same amount of RoCE that we have had in Mumbai.

I think this is the reason Gujarat Gas has lower RoCE / RoE as compared to MGL and IGL.

Please note that GGL’s GAs are mostly concentrated in district areas.

GGL has achieved 12.5 lakh PNG households with 21000 km of pipeline laid out while MGL managed to achieve about the same with just 5000 km of pipeline.

Lets define a metric called ‘Households per pipeline km’ for the listed CGD companies.

MGL FY18 - 205

IGL FY18 - 76.5

GGL FY18 - 57.7

AGL FY18 - 51

IGL has 76.5 but this is increasing at a fast rate if you compare it across years, while for GGL it has been decreasing / matured YoY. And Delhi is ‘very’ less dense than Mumbai, opposed to what one would expect on first thoughts.

Higher population density also drives CNG vehicles growth.

If the population density is high, it is in the best interests of the CGD company to install more number of CNG stations within a small area. Now from a car buyer perspective, he will find more number of CNG stations in his closer vicinity and will not have to worry too much about the availability of stations to refill his fuel tank.

So return on new capital which would be deployed onto Raigad may not be attractive.

Please share your thoughts.

Discl: Not invested in any CGD company.

17 Likes

Yes, population density is a defining metric in the CGD biz and the main reason for the above normal cash flows of MGL. The two moving variables in CGD valuations are population densities of their combined GA and natural gas prices.

Overall a satisfactory end to the year. The volume growth came in decent at ~9.2% and EBITDA at 31.7% for the year. Dividend per share has also increased marginally to Rs. 20.0 for FY18. Link to results.

1 Like

MGL profits depend on 3 or 4 factors

BG selling stake,Rupee depreciation,Rising input costs of natural gas, and of course EV markets .

From Nov 2018 to today stock price 30% discount

INR/USD is at 4% discount

International natural gas prices are at 1% discount, given the trade spat US natural gas shipments to China has dropped dramatically due to additional 25% duty, Natural Ags inventories are piling up which can mean there will be further downward pressure

EV market is customer driven and Wagon R -EV to be priced at 12 Lakh.

MGL Q4 results are conservative.

Looking at above MGL has good prospects

Please share your thoughts

Disc : Invested in MGL

2 Likes

1 Like

Lock in period to sell remaining 10% in MGL by BG Asia pacific ended yesterday. Last 2 times BG reduced the stake with bulk deals in market and stock fall by 5% and 7% respectively. Any thoughts on what will be the approach this time by BG? I was expecting the stake reduction to happen today

1 Like

City gas discoms may lose exclusive rights to market CNG https://www.livemint.com/news/india/city-gas-discoms-may-lose-exclusive-rights-to-market-cng-1562001699308.html

1 Like

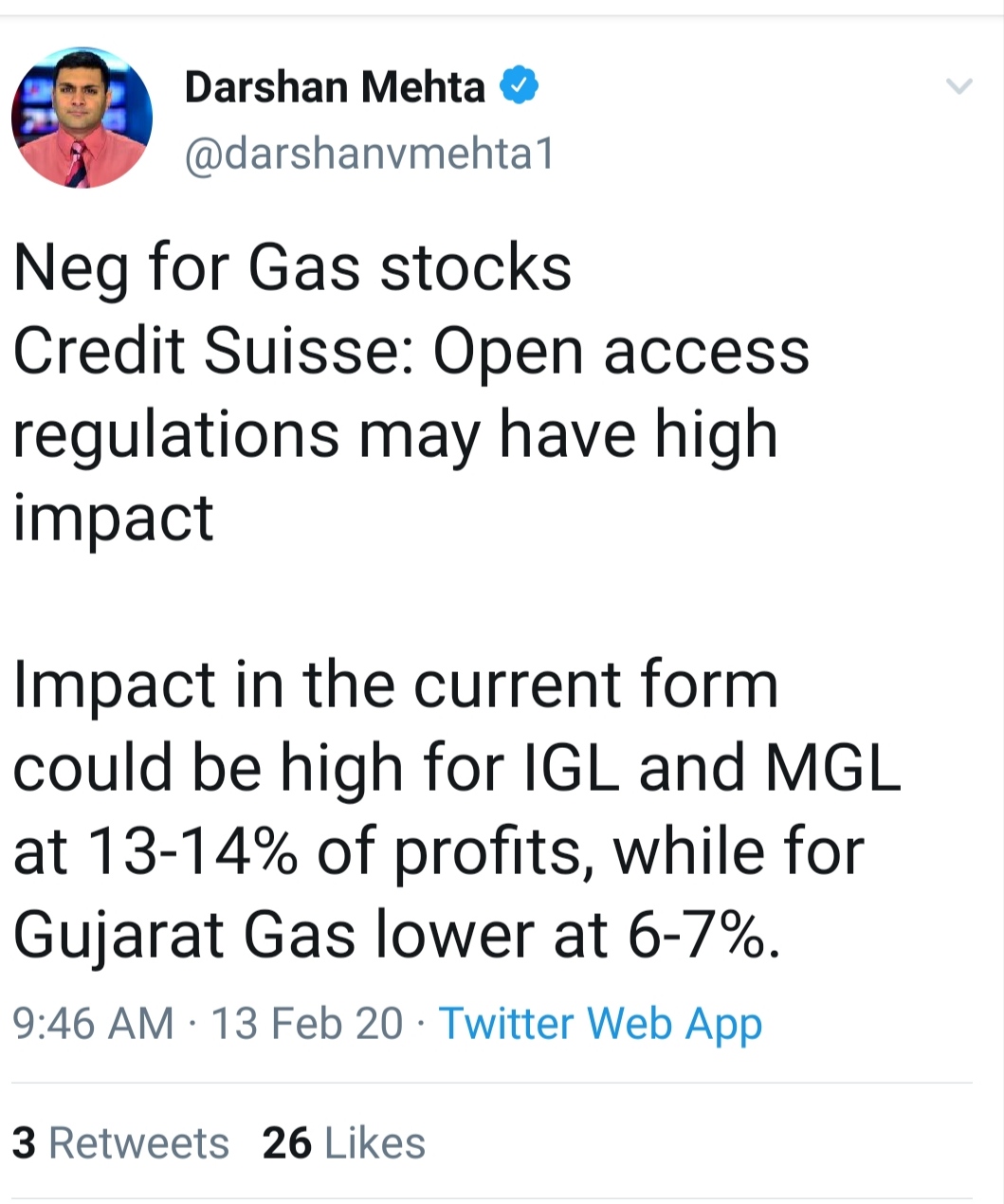

Nirmal Bang Report on Indian City Gas Sector

We are taking a negative stance on the Indian city gas sector, as it enters a transition phase that will bring current networks in Delhi and Mumbai under open access subject to regulated tariff, even as end-consumer prices of compressed natural gas (CNG) and piped gas (PNG) are left free.

Includes Initiating Coverage report on Mahanagar Gas.

1 Like

Mahanagar Gas Q2 FY20 conference call:

India currently imports about half of the gas it consumes. Imported gas accounted for 51.2% of local needs.

Natural gas pipeline expected to expand to 28,000 km by 2023 end from the current aggregate

length of about 16000 km.

Capacity of LNG import terminals are also planned to be doubled to about

55 million tonnes per annum in the next three years.

Power (31%), fertilisers (25%) and city gas (22%) sectors are major consumers

The price of locally produced natural gas has fallen to $3.23 per MMBTU.

During the quarter 32,241 domestic households were added.

In the second quarter we had a net addition of 47 industrial and commercial

customers and thus as on quarter end we had 3923 industrial and commercial customers.

We had 244 CNG stations supplying CNG to around 7 lakh vehicles and our

aggregate of steel and PE pipeline network stood at 5393 kilometers.

Raigad: At second quarter end, 13 CNG stations were operational in Raigad.

CNG sales in Raigad reached the level of 30460 kg per day.

CNG sales volume grew by 1%, Domestic sales volume grew by 4.5% while the industrial and

commercial sector sales grew by 0.2%.

Overall, the PNG volume grew by 2.2%.

EBITDA margin was 34.9% Vs 31.8%.

The company elected to exercise lower tax rate of 25.2%.

CAPEX: For H2 FY20, 300 Crores plus and 500 crore capex in FY21.

4 Likes

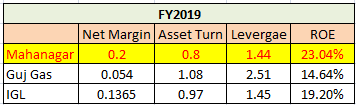

Good points, @lingalarahul7! High density should definitely play a crucial role in this business model.

To add further to your findings - it seems like Mahanagar has superior ROE because of superior margins when compared with Guj Gas & IGL. Below please see the details:

I’m yet to dive deeper, but below question for the group:

- Has anyone decoded what’s driving Mahanagar’s better margins compared to other 2 players?

It is very surprising to see such a vast difference in margins for these players in the same industry who would be procuring raw material at almost similar cost.

Disc: not invested

impact?

1 Like

There could be impact of Mumbai metro lines opening in coming years on MGL There was a study on Nagapur metro indicating 40% savings in fuel consumption in #gallons

http://ijirt.org/master/publishedpaper/IJIRT146226_PAPER.pdf

Currently BEST, auto rickshaws, taxis are major commercial consumers of MGL.