Comments welcome and though I’ve taken care to prepare the comparison from DRHP, annual report, etc. there could be mistakes.

There are many things going for the life insurance cos and you may go through the investor presentations, DRHP of SBI/ICICI Life to know the opportunity.

Additional Resources:

IRDAI First Year Premium of Life Insurers - This is a good resource to check the first year premiums of life insurance cos. Data uploaded every month, almost like the monthly SIAM numbers. You can check previous months also and July data is yet to be uploaded.

You have prepared very nice comparison. But I could not find your question or you justed wanted to share the information with the members.

If we value ICICI pru based on IEV, it is trading at a multiple of 4, which seems quite high to me. What should be IPO price of SBI & HDFC Life, if we assign a multiple of 4 to them?

I actually wanted to see if SBI Life is worth investing for me or our family members so did this comparison and anyway since I’m invested in ICICI Pru life, I kind of track the numbers. IMHO, there is not much to choose from these three companies though I like HDFC Life a tad better but SBI has this huge banca channel which can be leveraged. I might apply for HDFC Life IPO and recommend SBI Life for my family members.

I don’t have a view on valuations and don’t know what price to pay. But ICICI Pru Life was available less than 2.5 times EV in the past.

We do not know how many shares HDFC Life is going to offer for sale (or if there is going to be any fresh shares for sale) under IPO so can’t find out the price. SBI will be offered around Rs 660/share if we assign a multiple of 4. SBI sold shares to KKR and Temasek at Rs 460/share in December 2016. Even ICICI Pru Life sold to Azim Premji for around Rs 226 before the IPO where it was priced Rs 334.

excellent compilation of life insurance com. by drgurdge

I have invested in icici pru life

my thought process for investment was

its NEGATIVE capital employed business (float of premium paid)

it can be a CAPITAL light compounder

due to high promoter percentage possibility of consistent dividend

Working capital: ₹ 25.91 Cr only

icici pru life got Protection –3.9%

ULIPs –84% ideally protection should be more than ULIPs because ULIP is always market related and in bull market easy to satisfy with fund performance and consistency ratio but in bear market it is difficult

Good analysis. I am new to learning the business of insurance companies and how they are valued. As I understand such companies are valued as a multiple of Embeded Value. Can you share some details on how this EV is calculated? I went through details in the HDFC life investor presentation but still not getting a good picture of the various parameters that go in the calculation. Thanks

To begin watch this video - icici pru ceo nicely explains insurance jargons.

Icici pru life 2017 annual report is good read - management has spent couple of pages to explain what is EV, RoEV, VNB, VNB, what all products insurance companies typically sell etc.

Intuitively I feel insurance in India is expensive and not affordable but I don’t have any data to back it up. That’s one reason I am unable to invest in this sector as I feel the costs have to go down before it becomes a mass product.

Perhaps you can use some of the data you have gathered and throw some light on affordability of insurance in India and coverage and compare it to income levels of the insured.

@Yogesh_s,

I have not looked at the affordable part. But we have to keep in mind:

Most Indians mix insurance and investment. Thus an amount is looked at as capital and not cost. The more you invest, more the money on maturity.

Rs 1.5lac tax deduction available for life insurance.

Banks insists on insurance for their mortgage loans and I’ve seen that it may be mandatory (or pushed) though one might already be covered. Good opportunity to cross sell.

Regulator might put a cap on commission paid aka SEBI putting a cap on the expense ratio.

More direct selling, POS products will make more affordable.

NPS angle. India is now contributing pension society and a minimum 40% of corpus needs to be bought as annuity. In another 15-20 years we shall see a lot of annuity products being bought by the then retirees.

I feel Insurance is a way to minimise your loss. I have to insure my life (and pray that we never get to use the policy) no matter the cost.

The overall insurance industry success would depend on the following

Open Architecture - If open architecture becomes successful, it will be difficult for different banca led insurance companies. Everyone would want the pie, would become difficult to sustain.

Agency Channel - Agency is a bleeding factor for all insurance companies, no one is able to maintain the right Opex for this channel. In past 10 years contribution of agency has gone from 72% to 36% in the overall new business

Regulator might put a cap on commission. There are already caps in place for all the products plus web aggregators.

It is still a distributor led push product, online term plans have not been profitable due to various spurious claims. Organisations are investing but yet to see anything impactful

Someone mentioned POS Product, POS Product do not have margins for distributors or insurers. Hence promoting them would be difficult

There are various factors which are good and bad for the sector, but need to see which one would add to the overall growth.

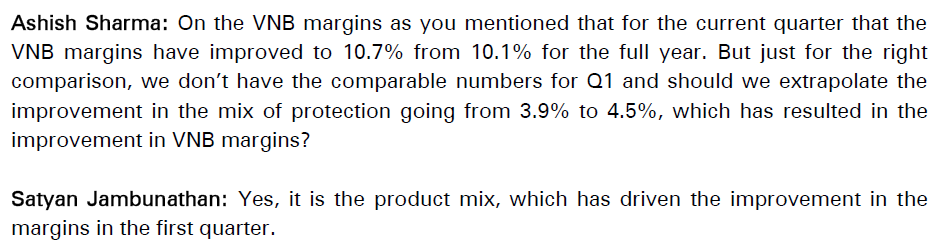

I’m not sure on what basis you are claiming this but term protection plans are profitable and aid to the increase in VNB margin. ICICI management commentary:

My bad if there was some miscommunication/misunderstanding

Spoke about online term plans, which have high acquisition costs, not protection plan per say but the digital foray of insurance companies where they are trying to pitch directly to the consumers.

From the interview of ICICI Pru CEO, I could make out that instead of looking at Profit before tax PAT, we should look at Value of New Business VNB for an insurance company.

Is it not similar to look to Gross Merchandise Sale for a e-commerce company instead of looking for Profits?

VNB, it seems to me is only the indicator of how could the business do in the future given the policies company has written in this year? Provided many many assumptions they do while calculating the number works out.

Another point, the competition in Insurance industry at the point is so immense that companies have to sell the insurance policy at loss.

This type of competition can happen in any industry and that industry would like to show investor the promise of future.

Shouldn’t we assume that industry facing a lot competition, the companies have no differentiated products and no moat whatsoever? Increased competition from existing or new players could take whole industry in red.

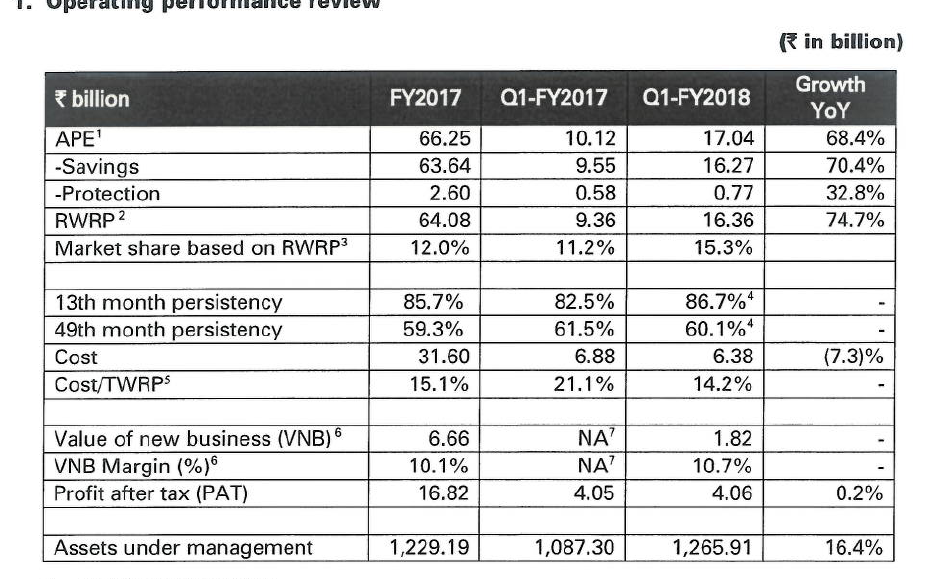

Thanks to this thread, I was re-looking at the numbers of ICICI Pru. What struck me was APE increased by 68% compared to same quarter last year but net profit increased by 0.2% only?

APE in simple terms the premium received. (regular + 10% of single premium). When premium received by the company increased by 68% why it did not percolate to the bottomline. So I looked at the financial performance of the company. Screenshot below for easy of all.

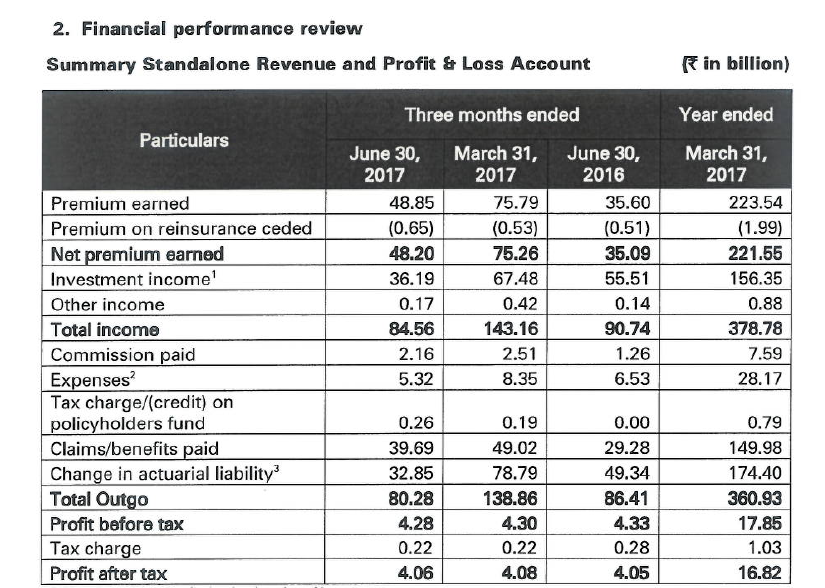

Have a look at the line item Investment Income, there is 35% decrease in Investment Income.

Management does not talk about Investment Income at all. I do not see a single line in the quarterly report or presentation about Investment Income. Investors have right to know more about Investment Income.

If I am correct Insurance company has two income sources

Premium income &

Float

What is float?

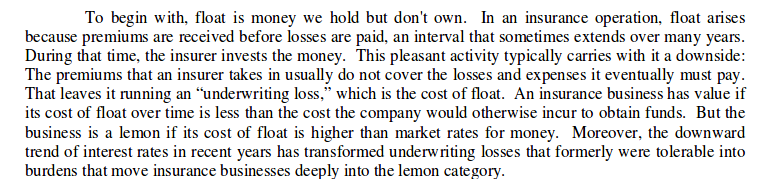

Since Berkshire Hathaway is a insurance company, Warren Buffet in his 2002 letter, Page 7 describes Float as

I think the company need to disclose more about its Float and investment operations and investors should demand more information from the company. I think we should know

How much is the float of the company, every quarter?

I am not an expert in Insurance company valuations/financials but see my view:

I don’t think any company is declaring the float but not sure.

I don’t think any company is declaring the mark to market value too but not sure.

This should be available in annual report.

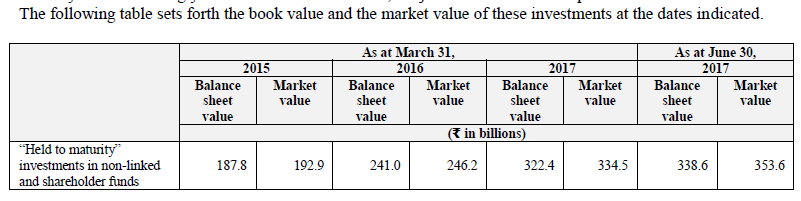

Available in the DRHP of the company. See the portfolio mix of the investment funds:

Column 1: ICICI Pru Life, 2:HDFC Life and 3: SBI Life

4.Each insurance company would have an Investment department/team who which invest the float. I myself work for a Insurance company and our company’s income generated from investments (inc. profit from sale of investments) was Rs 600 Cr in FY16 with a yield of 8.4%.

This figure can be checked in the annual report of the companies.

I don’t think it may be comparable. There are a lot of factors like the equity market returns, G-sec yields, etc. The AUM increased and yield of the investments would have come down and thus there is a decrease in investment income.

I check the item called “Transfer to Shareholders’ Account” in the statement of Statement of Revenue Account (Policyholders’ Account) to see how much is transferred to the shareholders.

HDFC Life has also filled for IPO and you may see the DRHP here:

It was a great read for me and IMO must read (along with the DRHP of SBI Life) for anyone interested to invest in insurance companies. I’ve also updated my comparison document here with latest figures wherever necessary. Life Insurance Cos -v2.docx (14.1 KB)

I am seeing newa mentioning HDFC Life plans to raise anywhere from.7500 to 13000 crores via IPO. At those levels the company would be valued between 50000 to 86000 crores. If we have to value insurance companies with EV, which was 12400 at the end of last year, the EV multiple comes to the range of 4 to 7 as FY17 EV. HDFC group will get a premium, so will it be valued at same or higher levels of Icici Pru which is currently listed with a market cap of roughly 64000 crores? (Btw, the EV of HDFC Life at the end of FY18 Q1 is around 13200 crores)