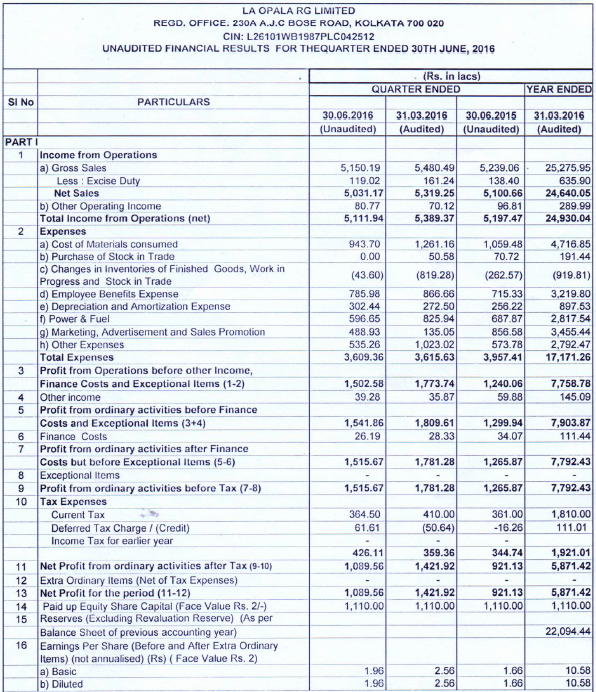

Laopala came up with subdued Q1 performance. It was on expected lines as Q1 remains weakest quarter for them. QoQ sales went down from 51.9 Cr to 51.1 Cr, although they have managed to clock bottom line growth of 18%, It has increased from 9.2 Cr to 10.9 Cr. The worrying factor is no growth in Top line despite expanding the production facilities.We observe a severe drop in marketing / advertising expense, I feel that after expanding the facilities, they need to push sales else they will remain under utilised. Let us see how Q2 & Q3, the best quarters for sales, pan out. Investors can take decisions based on next 2 quarter results. If the sales don’t pick up, it will become tough to hold the stock.

since q4 laopala has chnaged the way they account dealer commission…

they also reported that they hv reduced some distributor commission by 15%

so to avoid confusion lets see it without marketing exp. than

51.97-8.56= 43.41 q1 fy16

51.11-4.89= 46.22 q1 fy17

6.5% growth

1 Like

Kotak Mahindra Sold 14.23 lakh Shares of La Opala RG on 19th August 2016, The buyer was Jwalamukhi Investment Holdings, which is part of Westbridge Crossover Fund, LLC who already hold around 5%.

http://ripplesadvisoryindore.blogspot.in/2016/08/kotak-mahindra-sells-1423-lakh-shares.html

Westbridge Crossover Fund, LLC now has more than 7.5% (both direct & indirect) in Laopala. Earlier investment by them was 2 years back & price was around 370

Centrum Broking has come out with its second quarter (July-September) earnings estimates for the Consumer sector. The brokerage house expects La Opala to report net profit at Rs 17.8 crore, up 63.1 percent quarter-on-quarter. Net Sales are expected to increase by 39.1 percent Q-o-Q (up 13 percent Y-o-Y) to Rs 71.1 crore, according to Centrum. Earnings before interest, tax, depreciation and amortisation (EBITDA) are likely to rise by 52.1 percent Q-o-Q (up 23.9 percent Y-o-Y) to Rs 27.5 crore. They

expect sales to grow by 13%, led by volume growth of 23-25%. The company has taken price cuts which would impact revenue growth. Operating profit will expand by 24% to Rs 275mn. Operating margins are likely to expand 340bps on the back of lower to flat overhead cost. Adjusted PAT is expected to grow by 18% to Rs 178mn.

Consumer - Centrum - 15th Oct.pdf (195.6 KB)

I just entered this counter. Hope there’s still gains left in this

This stock is ONE of those where we can enter at every level BUT with PATIENCE.

Fresh entry in any stock just before the results is not advisable, but if you are here for LONG term, it must give reasonable returns. Said that the coming quarters are the best (historically) quarters for our company and we expect to see good run up but if the numbers don’t meet the expectations, we may see short term reversal also.

1 Like

La Opala RG Ltd will have meeting of the Board of Directors of the Company held on November 10, 2016, inter alia, to consider and approve the un-audited Financial Results of the Company for the second quarter ended September 30, 2016. Let us have a close watch on movement till then

The company has just shared the SHP as on 30th Sept 2016, One major point to note is that retail interest has increased drastically and it has addition of almost 300 retailers during current quarter itself. Retaining share holders & moreover attracting so many retail share holders gives us strength to hold it for much longer term.

Interested boarders can go through SHP Updated 30th Sept 2016

Laopala has declared Q2-2016 Results

The major findings are

Topline growth of 10.85% (Q2-15 Vs Q2-16) & 36.37% (Q1 vs Q2)

Bottomline growth of 13.87% (Q2-15 Vs Q2-16) & 57.48% (Q1 vs Q2)

EPS growth of 14% (Q2-15 Vs Q2-16) & 57.65% (Q1 vs Q2)

Although the Q1 - Q2 comparison does not hold any value as Q2 is historically strong among all other quarters, but Q2 comparisons give us a view where company is growing at lower than expectations set by itself in last 5-6 years. The expansions have not made major impact till now & we need to wait till the expanded facilities start operating at 100% capacity & the production starts reflecting in sales. I will still recommend HOLD for this GEM & wait for 3-4 quarters more to take a decision…

1 Like

La Opala is valued on AOCF/EV yield methodology. They have further ascribed a discount of 10% to

historical long-term average AOCF/EV yield of FY13-17E to La Opala and arrived at a target AOCF/EV

yield of 2.5% for La Opala, and hence, the implied EV/AOCF multiple of 40x. They use average cash flows generated over five years (and hence remain conservative) during FY15-19E and apply 2.5% Adj OCF yield to arrive their target EV and their TP of Rs564. Upgrade to Buy. At their TP of Rs565, stock would trade at FY19E P/E of 30x.

1 Like

I couldn’t rootcause the reason of slowing topline. But here are my guesses

- Firstly when I searched amazon for dinner set LaOplala’s product were down in the search results.

- Secondly plastic consumption in kitchen is increasing day by day, this may make opalware out of fashion in future.

Thoughts?

Increasing competition compare to increase share of organized players in unorganized Opal wares market. Borosil and Cello Opal wares increased capacity. Cello Opal Wares added significant capacity in new plant

I guess Cello Opal is not listed, If Borosil and LaOpala have similar business how can LaOpala have high ROE while Borosil don’t. Surprisingly Borosil too gave mind boggling returns as far as the scrip is concerned inspite of Low ROE, I still need to understand the underlying maths properly. whereas La Opala turned around very well in last 6-8 years in expanding margins and having good ROE and. Now the concern is topline slowdown of late. Do you have the number of organised vs unorganised split ?

Issue of Bonus Shares

La Opala announced that its Board of Directors may consider the issue of bonus of shares to equity shareholders during its meeting scheduled for February 5, 2018. The company is yet to announce the bonus ratio, ex-date and other information related to the bonus issue.

Our company has clear differentiation strategy whereby it caters to economy and premium segments through separate brands. The company derives 84% revenues from domestic business and remaining 16% from exports (40 countries). The Indian market for opalware is worth Rs 450 cr and is growing at ~20% annually. While there are limited players (Borosil and Cello) in the organized opalware segment in India, competitive intensity is high owing to market under penetration.

Our company has capacity of 21K tonnes/annum (tpa), which it plans to expand to 25Ktpa by March 2018, providing scope for revenue expansion. The company has a debt free balance sheet, cash and liquid investments to the tune of Rs 135 cr (March 31, 2017), stable working capital intensity (13-15% of sales) and ROCE close to 30%.

1 Like

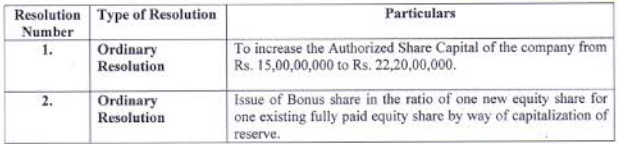

Board of Directors had recommended issue of Bonus shares to the shareholders of the company in proportion of One (1) Bonus shares for every One (1) existing equity shares held by them in the Company as on the Record date, to be fixed separately subject to shareholders and other regulatory approvals as may be required. The approval of shareholders is being sought through postal ballot route.

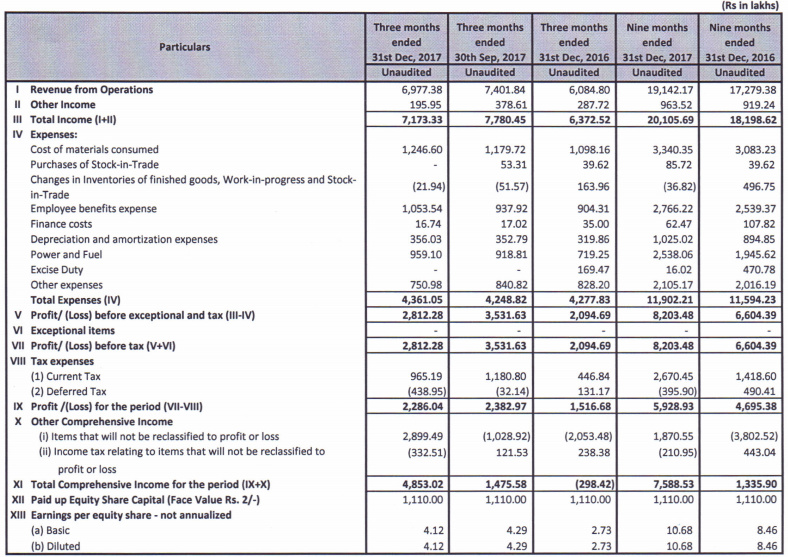

Q3 results are also declared

Management has fixed Friday, 23rd March, 2018 as the Record Date in order to determine the eligible shareholders to receive bonus shares, subject to the approval of the shareholders by postal ballot, the results of which will be announced on Tuesday, 13th March, 2018. The Members whose names will appear in the Register of Members of the Company and/or Register of beneficial owners maintained by the Depositories at the close of business hours on 23rd March, 2018, will be entitled to receive the Bonus Shares.

Shareholders have approved following resolutions

Laopala came up with another subdued performance with 7.82% topline growth, while bottomline has grown by approx 18%

The worrying factor is no growth in Top line despite expanding the production facilities. They had expanded the Sitarganj manufacturing capacity few years back, which started operations on 16.11.2015 & seems that is still underutilized ( as topline has not shown expected growth)…

The Directors at the Meeting held on 30th May 2018 approved the plan for setting up a new unit at Sitarganj to manufacture Opal Glass Tableware at an estimated cost of Rs. 135.00 Crore, which provides visibility that management is still able to see bright future. The main concern remains is under utilization of current facilities, without that it will be tough for prices to move in right direction. eagerly waiting for how Mr Market reacts to addition of capacity by investing 135 Cr. I personally feel that after expanding the facilities, they need to push sales else they will remain under utilised.

1 Like

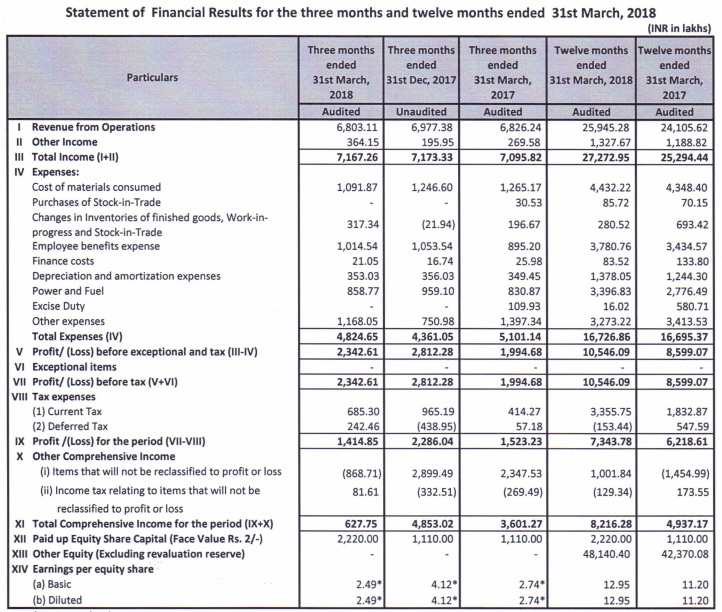

How are the EPS nos. arrived in the above table???

3601.27 lakhs EPS is 2.74, No fo shares 5.55 crores??

627.75 lakhs EPS is 2.49, No. of shares 11.1 crores ?? (Bonus shares issued during the year)

Also for the yearly figures, unable to understand how they arrive at the EPS??

R they using item IX as the profit and no. of shares as 5.55 crores in all cases to arrive at the above table EPS figures??