Sitarganj expansion plan can be seen both ways. 1. It could be considered as management’s confidence of the future growth 2. It could be considered as “bravado” knowing current under utilization of the capacity.

La Opala is the domestic market leader with very good brand recall in the opalware market for last 25+ years. They also have 30%+ OPM for last few years. Now for the first time, they are facing competition from another domestic player i.e. Borosil (after acquisition of Hopewell ‘Larah’ brand). Borosil is planning to spend 30 Cr in Advertising and Marketing for FY 19. So unless La Opala drops their prices (which will reduce their margins), it would be difficult to grow sales from here on.

But market size is also increasing and La Opala has cash to fight the competition (by spending more on A&M as well as dropping prices). This means growth will come at a cost. Sometimes market leader tends to down play the competition and thereby allowing competitor to get “foot in the door” .I think lot will depend on how quickly La Opala accepts the competitive threat and take corrective steps.

Disclosure - not invested in La Opala. Invested in Borosil. Hence would be happy if La Opala ignores competition

Any idea why power cost is up so much ?

Disc: initiated a small position recently after price correction n wait of almost 2 years to buy 1st tranche at desired price

Q1FY19 result ahead of expectation: Total revenues were flat at Rs551mn on the back of healthy volume growth and new capacity addition of 4000MT from April’18. Operating profit was up 36 per cent to Rs245mn with 596bps operating margin expansion to 44.5 per cent on steep gross margin expansion due to increase in inventory. Power cost was up 57 per cent YoY on new capacity while other expenses were up 29 per cent YoY. PAT was up 15 per cent to Rs145mn. Other income was down 50 per cent on lower treasury income.

New capacity to boost volumes: During the quarter the company expanded its capacity by 4,000MT in its Satarganj plant taking the total capacity to 25,000MT. This helped the company post high double digit volume growth during the quarter. It is believed that this volume growth will get better in the festive season given the affordable pricing for the dinner set. Management suggests that the new green field capacity of 11K MT is on track and would be commissioned in H2FY20 taking the total capacity 36K MT. Significant under penetration of the opalware products coupled with growing distribution would drive growth for the category and company.

Management focus on category growth and not margins: While the operating margins for the company was up 596bps to 44.5 per cent during the quarter, management maintained that the full year margins would be about 40 per cent range given the significant investments they would do in brand building. While gross margins would remain high on stable RM prices, higher sales contribution of premium products such as Sovrana and Quadra, operating margins would remain muted on higher Advertising & Promotion spends and expanding distribution reach. Competition intensity continues to remain high which would mute price hikes. Hence the management would focus on volume growth and not margins.

Key downside risks could be increasing competitive intensity by borosil coupled with delay in commissioning of new plant.

Recently I visited DMart and could see lot of Laopala products available. This was missing earlier. I take it both ways… on one hand it is good step towards pushing sales but on other hand margins will certainly be lower as DMart is known for low pricing hence lower margins for suppliers as well.

I can see Laopala products available on almost all online shopping portals as well… looks like management is pushing hard to utilize expanded facilities & ofcourse they are adding 50% more production facility in next 6 - 8 quarters.

How are you guys confident of La opala continuing to earn 40%+ opm margins in the future. IMO it is just too exorbitant. Borosil has reasonable margins in comparison.

If we look at the FY18 results of Hopewell vs LaOpala it leads us to some interesting observations. OPM for HTPL is 6.7% va 41% for LaOpala.

From a cost of materials consumed perspective HTPL spends double on packaging material than LaOpala for every rupee of sales

HTPL has 60% more raw material cost too as a % of operating revenue. These two points are major areas. Now the Borosil management does say they are getting to operational efficiency and thus I think their differences on these two with LaOpala will narrow down.

In addition to the above 2 points HTPL even spends double on freight forwarding. This too will change as per Borosil management due to efficiencies kicking in.

Other points include - HTPL is carrying more inventory as a proportion to sales (on this the management says they dont want to dump products on channel partners) , it pays more salary to its employees, HTPL also has more loss due to discarded PPE

I could not figure out the marketing budgets for LaOpala but HTPL has significant budgets ~5% to its own sales. Borosil management is going aggressively to increase this in the coming quarters 13% to 14% of revenues.

Borosil (Larah) should be able to improve margins but I don’t think it will reach the levels of LaOpala. Despite Borosil’s management saying they are not gunning for market share as the market is expanding this is going to put pressure on LaOpala margins which I think will not be sustainable in the future. Larah top line will also get a decent bump up putting further pressure on LaOpala. Like I mentioned in the Borosil thread Larah is undercutting Laopala on pricing and this is an important point in marketing and product positioning decisions which will do the rounds in these two companies. Interesting.

Foreign investors sell stake worth Rs 109 cr in tableware firm La Opala

ABG Capital, LTR Focus fund and Steadview Capital Mauritius Ltd. sold over 4 per cent stake in tableware company La Opala RG for Rs 109 crore through open market transactions.

Borosil (2nd largest opalware manufacturer) had reported a 48% jump in sales YTD. this indicated Laopala is loosing market share big time. Also declining margins is not helping the share price. No one knows how long this decline will continue. But on the positive side High ebitda margins were not anyways sustainable and is not reaching saner levels. Once competitive intensity cools down the performance might improve.

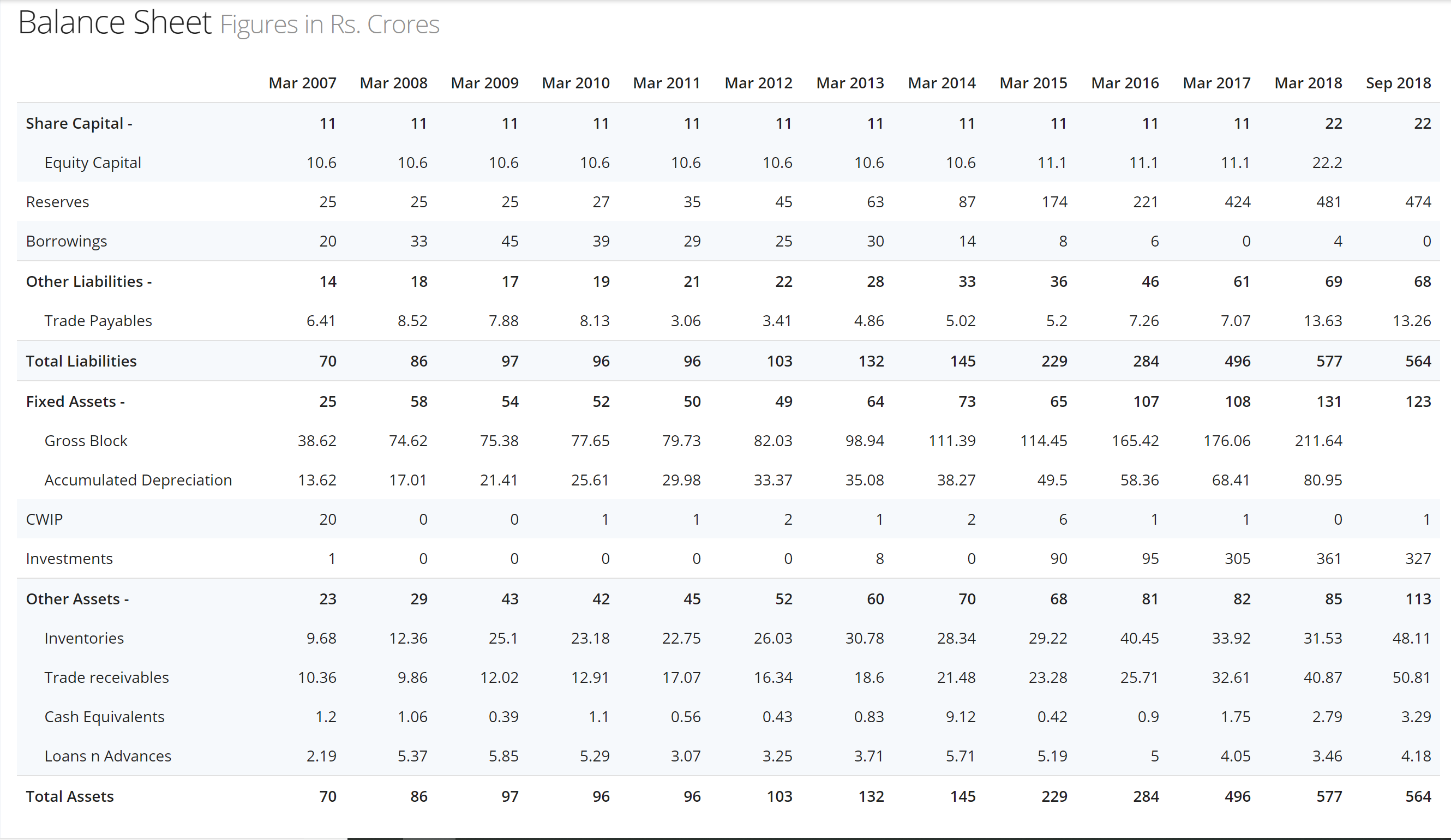

This is the balance sheet of La Opala. As you can see in the image above the total assets has reduced from 574 to 564. The company has earned profits of 14.49 and 21.53 crore in june and september quarter. They only reduced their liabilities from march to septemer quarter by 5 crore. Value of final dividend paid for year 2018 was 11 crores. So where has 14.49+21.53-11(Approx for dividends)-5 crore for reducing liabilities=20 crore gone. Since assets reduced by 13 crore around 20+13 = 33 crore is missing. I might be missing something obvious(Still a beginner) and would really appreciate the community’s feedback.

All of it explained by fair value through PL under OCI - Lo opala owns some shares in its own self through investment in a promoter entity. 33 crore difference is owning to its own stock movement

Dear All,

Whats the reason that ROCE has suddenly reduced to about 13 % in last 2 years from above 20% ?

Also is the antidumping duty on opalware extended ?