Thanks for providing the info. However this is for export only which account for only 32% of sales. I was looking for overall sales volume and realizations and paddy procurement prices. I will take a look at the conf call transcript to dig that info out.

Precisely for this reason, I created a shared spreadsheet where we can contribute so anyone starting to investigate a company does not have to start from scratch. Here is the link to the sheet.

I think numbers may not be readily available but are discussed in concall and ve seen questions being asked even on break up of volumes in terms of branded,non branded etc. I am afraid that pdf files of concall transcripts are not available on site/researchbytes and you may need to go through all audio calls. Disc : 3.5% of portfolio at Rs450. Currently holding.

On inventory part, yes, rice is a cyclic business with 2-3 year cycles,so, companies who have ability to hold large inventories at cheaper price and understand cycles may be partially better, nonetheless, investors should always factor in normalized margin. Another important aspect of current upcycle in rice has been too much of competition deteriorating pricing. The same has been discussed in both KRBL as well as chamanlal concall. Also, there are 2 companies kohinoor and lakshmi energy and food who have already defaulted on interest payments or in very poor shape. So, to create any view on valuation, an understanding of business cycle, normalized ratios, demand side and supply side consolidation should be taken. Personally, apart from factoring normalized profit margin and then doing traditional valuation , I am yet to find a better way to valuate considering the complexities with inventory. Disc: Hold KRBL at 450 (3.5% of portfolio) , Chamanlal - Have done both buy and sell in last 2 years and current hold only 20% of initial investment,booked profits shifted to KRBL 2 months back. Bad timing may b

Your points r correct. Lot of these details r in concall.Worth listening if looking for operational nos. I am too currently holding considering the recent news. However, time to accept diligence failure n improve.

Good analysis. But I’m pretty sure the requirement to mark down inventory is there only when Net Realisable Value of Finished Goods has dropped below its cost. (Ind AS 2)

For raw material intended to be consumed (and not sold directly), there is no requirement to mark down if the prices drop, as long as the final product will be sold at a profit.

Lower paddy prices will be seen as a positive and gross margin accretive for KRBL as long as they can keep prices of Basmati rice the same.

KRBL has been in the basmati rice business for many decades. Since they age their rice before selling, they need to carry very large inventory. Due to their considerable knowledge of the business (understanding of the paddy cycle) and brand strength (ability to charge a significant premium retail price in both export and domestic markets) they manage the spread very well. They do this by increasing/decreasing their paddy sourcing depending on the stage of the cycle.

Also, they hold inventory in their books at cost, haven’t heard them mention or seen them book inventory gains/losses in their P&L. They have been able to do this over the years without significantly impairing the quality of their balance sheet, unlike many of their peers.

Finally, if the overall consumption of basmati rice (both domestic and export) keeps increasing, they have sufficient milling capacity left to be able to absorb this growth without any further need to invest capex.

Business wise, yes this is a WC heavy business, due to the need to hold inventory, but apart from that it ticks most boxes as a quality business.

KRBL accounts for inventory using the avg cost method. The sales have remained flat in the last 3 years while the inventory and gross margins have increased significantly. This implies that during the this period the cost of goods sold has decreased for the same volume sold year on year. The inventory value will increase as cheaper raw material is taken out from the books. Thus, with no significant movement in sales volume - the company can get a temporary boost in margins. This kind of margin improvement is not sustainable over a long period and it will revert.

Agreed, there will always be a dislocation between cost price and selling price when the average holding period of the inventory is 1.5-2 yrs. However, the company has been able to consistently maintain industry beating margins without leverage and also build a strong brand recognised in their chosen markets - both abroad and in India. There must be some truth in their claim that understand this industry and know how to maintain their margins. The management has repeatedly mentioned that they cannot promise margins like in recent times, but have always maintained that they can manage this within a range, better than others, due to their ability to intelligently source inventory and sell a premium branded offering.

Very well said @bheeshma. In other words, at least part of the profits KRBL reported are phantom profits. There is nothing wrong with that but as investors we should be aware of it especially when stock has rallied so much over the past 2 years.

It is likely that KRBL is doing as well as it can to run the business. Its a difficult business to run given all the moving parts and they have done a fairly stable job of maintaining the margins.

The news regarding alleged wrongdoings has come at an inopportune time but that’s not the real reason causing the fall. The market valuations far exceeded its intrinsic value in recent times and are now reverting back to it. The news is just helping it along and in my view and causation and correlation is perhaps being confused.

The business eats up of unit of capital to produce one unit of sales and delivers a net margin between 10% to 12%. It also reinvests most of the earnings into the business. That’s just the way the economics of the business have been in the past and its likely that they will be like that in the future.

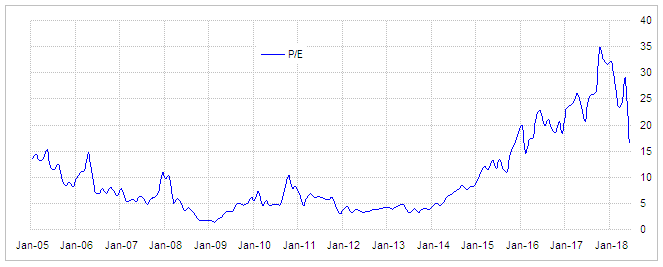

In my view, the business is likely to get an earnings multiple of 10-12 given this configuration. Even now its grossly expensive and likely to get cheaper as margins become more sober. Nothing wrong in the business and the owners have managed it well.

The basmati rice business is not inherently capital intensive, other than the investment that is needed to fund the inventory, which is reqd as mentioned before to age the rice. This is turn gives the basmati rice its quality, and is what is appreciated by people who eat basmati rice, esp. in ME markets. The business generates sufficient operating cash flows in order to fund this inventory as can be seen by the overall quality of their balance sheet. So I tend to look at this as a competitive strength as most of their peers have not been able to do that.

And they have sufficient milling capacity to be able to absorb any future vol growth. So no immediate capex foreseen.

In the last few years (2014 onwards I think) most of the capex that you see (~700+ cr) is because of the investments into the energy business, which the company did to get benefits due to AD etc. If you take this out, you will find that the rice business has been + FCF generating.

Now that these SOPs have been discontinued, the company has said in prior con calls that they will not make any further investments in energy segment, but I am going to closely monitor that going forward.

Adding to the above, considering that Kohinoor and Lakshmi are in trouble, and also considering the LT’s Insurance claims may well never be realised and adding further that Interest costs are rising, KRBL might actually be the only serious player standing in the branded organised rice sector in India (which is 70% of the global supply). Sounds like a superior competitive position if you ask me. A PE of 10-12 as highlighted above might be too low.

Also, demand is increasing in modern retail and exports margins might increase due to INR depreciation.

As far as the building of rice inventory is concerned, it has been clarified time and again over the last several quarters that Aged basmati rice is different from new basmati rice. I don’t think that KRBL will have too much trouble in passing on costs and maintaining margins. Even if percentage of gross margin comes down, the absolute EBITDA per ton I believe will be maintained.

My sample size is too small to be statistically significant, but in my hometown, Patanjali has become the market leader in Basmati rice displacing KRBL in last one year. Confirmed this after talking to two distributors and they feel Patanjali is more VFM and can gain more marketshare if it manages the supply chain more efficiently. So, IMHO, KRBL faces more threat from Patanjali than Kohinoor/LT. Going forward, Patanjali may emerge as a serious competition and I believe basmati rice business has less moat than FMCG and Patanjali has successfully penetrated FMCG moats.

I think the present slide in stock price has some thing to do with high revenue share from Iran. Trump has been asking countries (including India) to cut down on oil imports from Iran. If our government bows down to this demand , Iran will definitely retaliate with cut in Basmati imports.

A few data points according to the conference calls which may explain the flat sales… FY18 volume growth -20%, FY17 flat , FY16 28%

FY16 - one time Tender order of 100k in exports - led to higher growth - FY17 the tender order was absent…

FY18 versus Fy17 - bulk supply of 100k reduced in domestic market ( No idea why)

So if we believe the company’s commentary, the flat sales was more due to high base of FY16 and decline in volumes in FY18 .

Part of gross margin improvement may have been due to the reduction in bulk supply which is done at lower margins. Nevertheless, the phantom profits will definitely be reversed in next few years.

Just because there is a bad news around the corner you are giving PE-10 to this biz. How about the brand value which they have developed over a period of time? it takes lot of efforts to develop a brand like India Gate. Just check with FMCG veteran if promoters would like to sell India Gate Brand to someone how much value they can fetch thats why FMCG players trade at 40-50 PE. Here, it is a mix of FMCG & exporter of rice, it should command minimum PE-20. Pabarai was not fool he saw value at 500 plus…

I wonder how discussion changed because of bad news. Aging Inventory was a moat for the company and big positive and now we are suddenly started seeing negative in this. Similar was the case with their business model.

Unlike Manpasand, Vakrangee cases, there is a legit business underneath here. This is more like Avanti’s and DCM Shriram’s big fall which offered a quick trade.

I have no idea about what pabrai saw. My assessment is based not on the news but on the possibility that margins will revert. If they do then the market valuations it is quoting do not look exciting.

Ofc if margins sustain at current levels and the co becomes more capital efficient then there is a case for higher valuations but in my view that wont happen.

In the end, we are all trying to derive valuation comfort. The bad news has nothing to do with it.