Why do you say KRBL as a company has nothing to do with the issue? From what I read in the report, 100% subsidiary of KRBL was used to launder money and pay the kickbacks and this subsidiary was later transferred to a related party. If this is true, KRBL was the main entity used in this scam.

4 Likes

Frankly, it’s astonishing how speedily a report has been prepared to assuage investor’s concerns

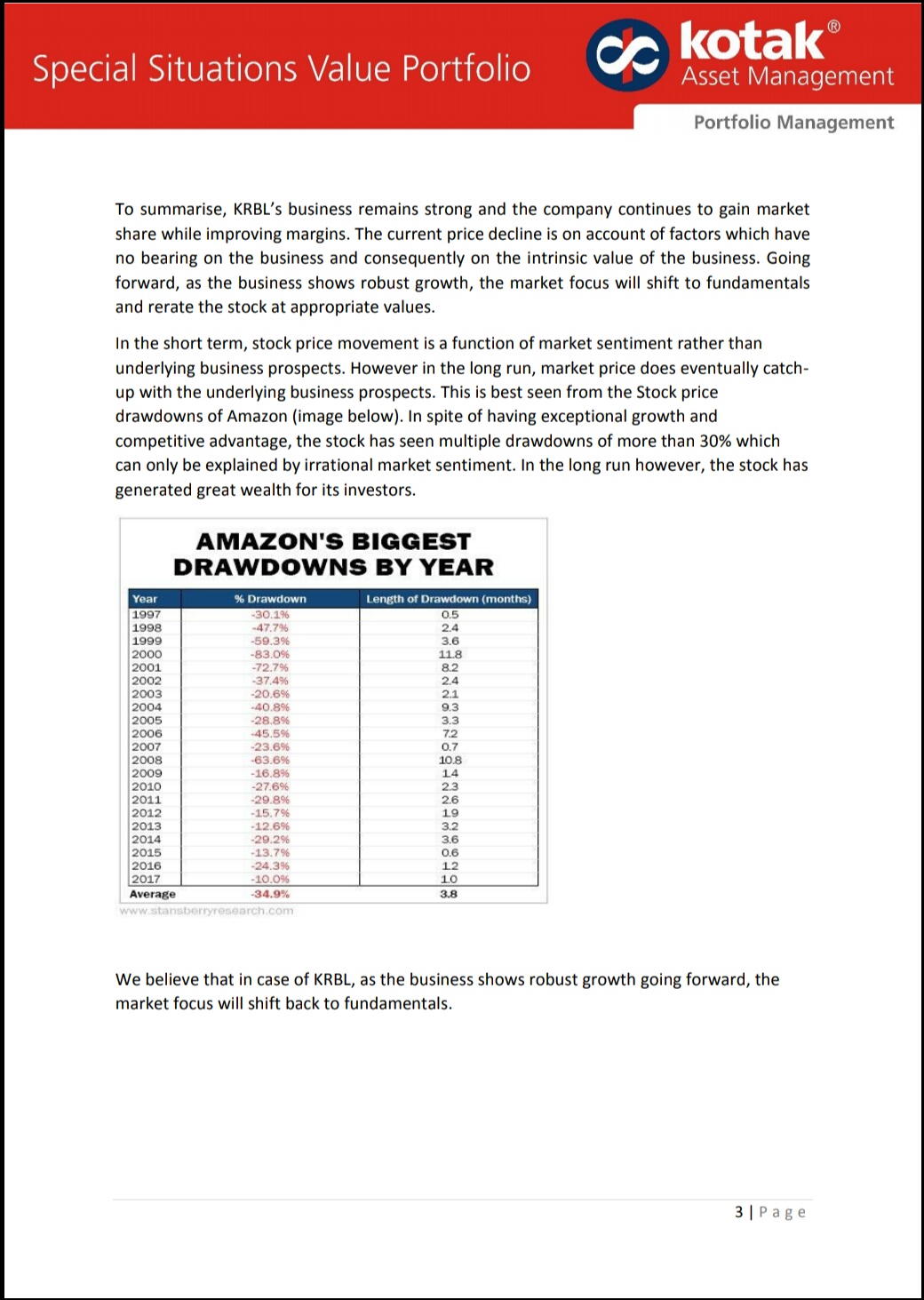

At the end of the report parallels have been drawn with the share price fluctuations of Amazon. In my opinion, it’s ludicrous such a comparison has been drawn- A comparison of apples and oranges.

8 Likes

My view is that for a retail investor to declare promoters as honest or otherwise is too difficult.The lure of I’ll gotten money can take anyone to unbelievably low which we have seen from satyam, Geetanjali even ICICI bank and many others.I can,t remember any Indian company which came under cloud and was found to be false.My view is to be v cautious in such cases as promoters know that legal system is too slow, sluggish and they can get away.

3 Likes

“The ED document accessed by this newspaper says that RAKGT was incorporated in 2007 by KRBL DMCC, Dubai, which itself was incorporated in 2006 as a 100% subsidiary of KRBL Ltd, India. In 2009, the entire stake of KRBL DMCC held in RAKGT was transferred to Potdar, the nephew of the promoters of KRBL Ltd, according to the ED,”

Info on RAKGT …shared by Atir Khan of Sunday Guardian

1 Like

KRBL had their Auditors " Vinod Kumar Bindal & Co" and last year changed to " SSAY & Associates,Noida".

Which seems to be normal rotation of auditor.

Please correct me.

Disclosure:

Have a tracking position

2 Likes

As a research report, they are just re-iterating what the mgmt has stated. Have they done any digging to investigate the issue ?

Fact v/s Opinion. Facts help distill the confusion and provide guidance on the uncertainty. Opinion of the mgmt does not count always. Not sure comparing to amazon is right, but that is “One” fancy comparison.

1 Like

I was accumulating KRBL from 430 , but I exit at 365. Approx 20% loss, as the allegation were serious in nature. A contrarian in me, wanted to buy more since there are all the sign that KRBL is marked leader in Basmati, but there are better opportunities available.

Just wanted to highlight that we missed an opportunity, and we are not good detectives  but can use this event for learning.

but can use this event for learning.

When the Shareholding was reported by the company, it did not have Pabrai’s name. The stocks were in the name of “Clearning House”. When do you see something stuck at clearing house for a long time? This is something which we should have caught.

(I remember that in the group, people were asking and wondering about why Pabrai’s name was missing, but never suspected such a fallout). Easy to say this in Hindsight

11 Likes

I think the kotak report has ulterior motives. Notice the shareholding patter. They hold 2.63%

Why has no other brokerage come out with their opinion yet ?? Because Kotak seems to lose from this downfall and hence the urgent report in favor.

I am invested and thinking is dumping. Plenty of cheap fish in the pond available.

7 Likes

5 Likes

This issue is pending in high court. Sub-Judice. There is no conclusion yet.

The Jt. MD, in the interview, mentioned that Pabrai got his money back and Balsharaf got the shares back (presumably from the Clearing Corporation).

It would be interesting to check out the Q1 shareholding pattern which should be released sometime during the first week of July.

People care too much about star investors and forget that they are human after all. Why does it matter if Pabrai bought it knowingly or unknowingly? All you have to do is to decide if this will bring down the valuations in the long term and if this will continue to happen. Will the tax perks encourage these companies to act like this in the future? Each investor needs to answer these questions to himself and can take a call!

2 Likes

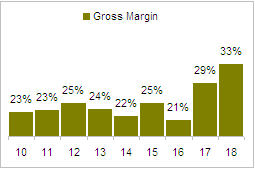

KRBL maintains huge inventory of rice. Since paddy prices are expected to come down, basmati prices will follow the trend as well causing KRBL to mark down its inventory. This will increase its COGS to rise and reduce gross margins.

In fact, the exact opposite could have happened in last 2 years. As paddy prices were rising, it marked up its huge inventory causing COGS to drop and gross margins to surge.Now margins could revert to mean of 24-25% from current 33%.

Source: Capitaline

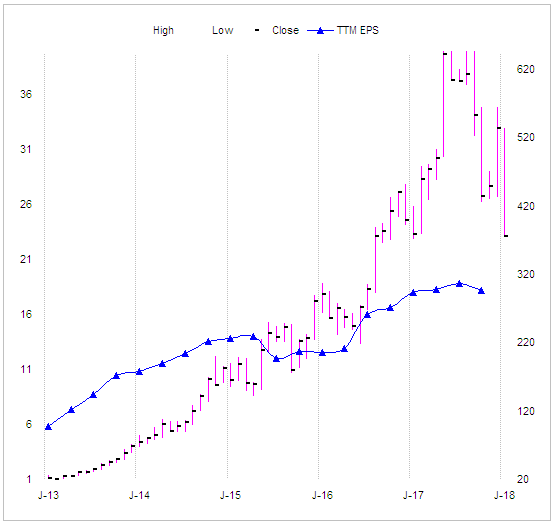

Stock price has run up far ahead of EPS.

Source: Capitaline, BSE

Looks like market priced this stock as FMCG company and PE ratio steadily jumped from 5 to 35 over last 5 years.

Recent issue is just a wake up call to investors in this company and they are repricing the risk. I have seen this wake up call behavior happening in many cases. Some issue causes investors to take a serious relook at their position only to realize that it is overpriced. Stock corrects for valuation reasons and not the issue that caused investors to wake up. Just my opinion.

18 Likes

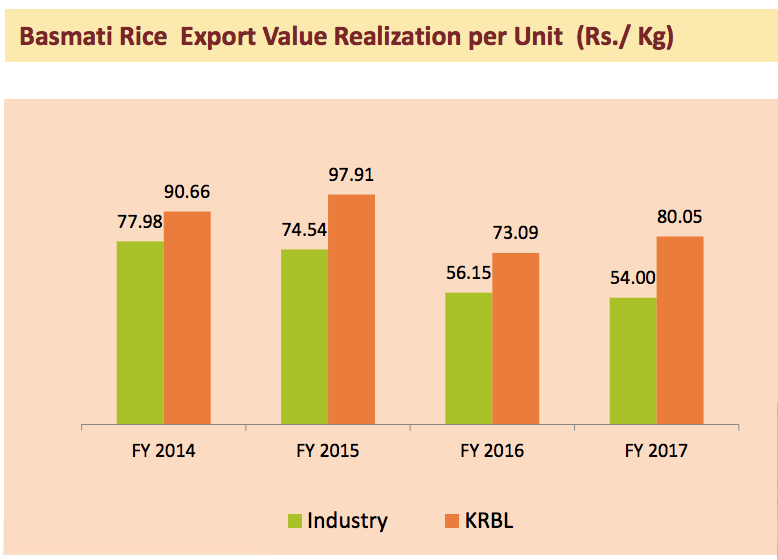

Does the company disclose annual sales quantity and price realization? I was trying to find that information in annual reports but could not find it. They talk a lot about global macro, Indian rice industry and give detailed statistics of the industry but nothing about their own company. Impossible to build a conviction when you can’t find out sales volume and realization which the company can easily disclose.

5 Likes

Derating of KRBL will have a rub of effect on other rice companies as well. Chaman Lal n LT are correcting . We have to wait for the dust to settle and to see where the price get stabilised.

What @Yogesh_s is saying is correct. Cos with huge inventory and long working capital cycles have a tendency to increase margins in an inflationary raw material environment and the opposite happens in a deflationary environment. If its a fixed cost business , the problem is compounded further. Prices have a tendency to catch up with valuations as markets are occasionally irrational but rational for most part. The 7 - 10 year average margins should be a good approximation for margins to be expected in the business in the long term.

3 Likes

We are only talking about moral compass . Do you think no interviewer has asked about this status of transaction to Mr Pabrai. It is conveniently edited. May be there might have been other compulsions to him .

I have seen this info in Investor Presentations and heard it in concalls. These snippets are from latest concall.

This is from FY17 AR or Investor Presentation (Am not sure where I got it from but its from an old post of mine in this thread)

So they do disclose volumes and realisations but perhaps not all in one place and not every time in the same channel.

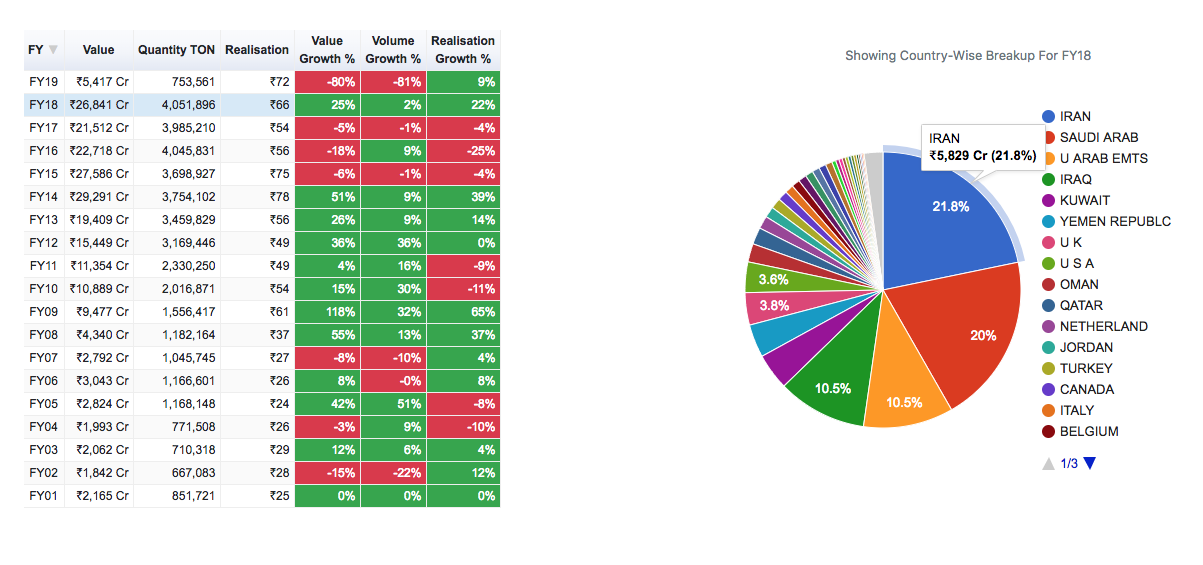

This is not true. This is the Export data for Iran. They have imported in 2017 (FY18) and also have imported in the first 2 months of this FY.

and Iran was in fact the biggest importer for Indian basmati rice in FY18.

I think what we need is a snapshot of all this data in one place so that we don’t go back and forth on the same things and don’t have to search for data points every time.

Disc: Not Invested

4 Likes

My bad. I thought the basmati import was banned for whole last year. It is only seasonal ban imposed in July 2017 & and the ban was lifted in Nov 2017. Apologies for incorrect info.

http://www.tribuneindia.com/news/haryana/iran-lifts-ban-on-basmati-import/505062.html