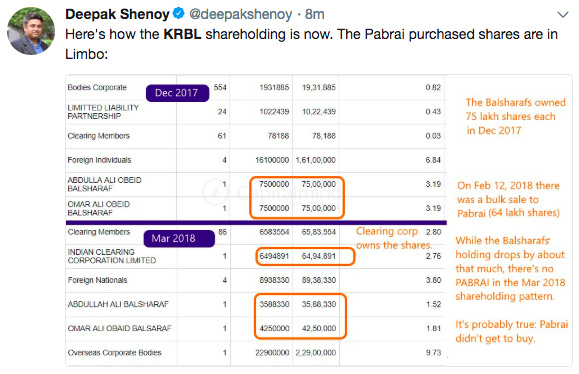

@sajijohn - Those are some very serious allegations and the exit of Balsharafs and the way the management reacted in the concall portraying as if they know nothing about what happens to their stock leaves a lot to be desired. If the Balsharafs operated demat accounts and participated in trading, then I wonder if they were involved in a money laundering/ pump-and-dump scheme. It remains a mystery why the Pabrai fund’s name appeared in the disclosures while not appearing in the shareholding as well. Remember this is a transaction with the Balsharafs. So definitely there is something murky going on here.

Disc: Exited in the run-up post results for different reasons.

Balsharaf - One of KRBLs top distributor and shareholder is suspected to be involved in Agusta scam

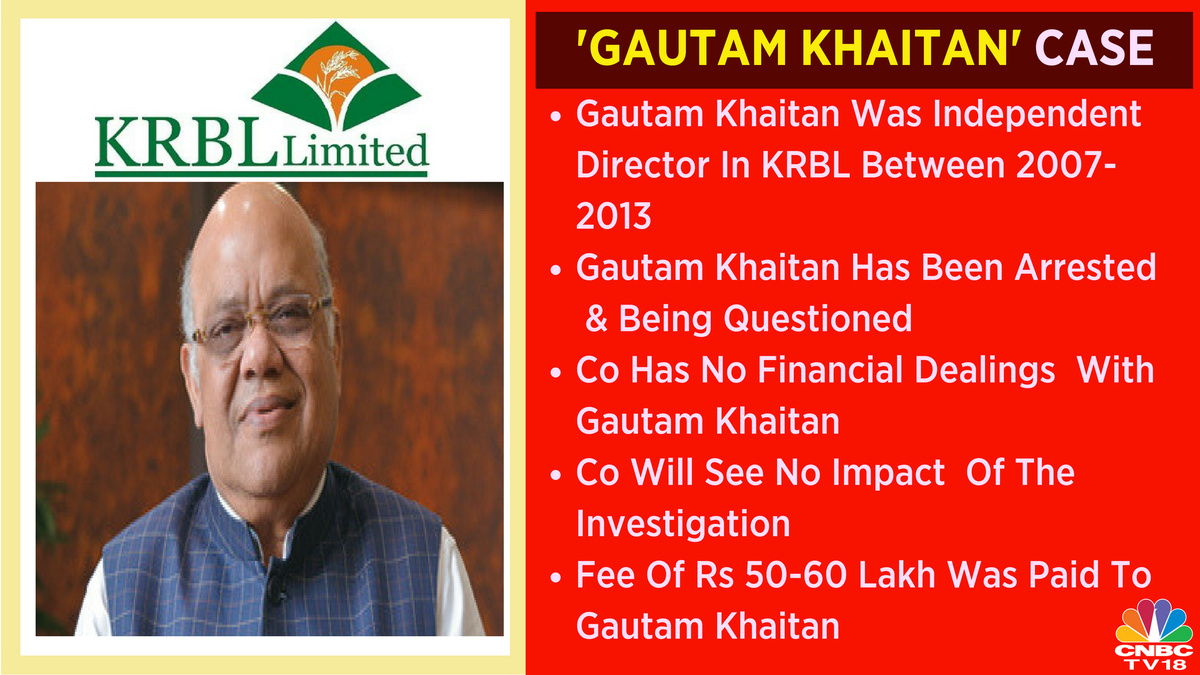

Gautam Khaitan - Independent director in KRBL from 2007-2013 is allegedly involved in the Agusta scam

Anoop Kumar Gupta - Jt. MD of KRBL questioned by ED about KRBLs role in Agusta scam

Some twitterati’s reaction and agree with the over-reaction part. The market has lost it’s direction and hence hatching on the news/sentiments. Due to the latest allegations/resignations, every small/midcap investor is scared out there.

Mr Anup Gupta denies that he mentioned anything about “taking loan from Balsharaf and repaying it to ED”. If what ED says is true, then it may come to haunt KRBL management later.

The creation of subsidary RAKGT under KRBL DMCC & transferring it to Anurag Potdar (mentioned as nephew of Promoter of KRBL). This again needs to be investigated as to why this is done.

From the article, these two things are very discomforting. Need to see what else comes out in future.

[The Augusta westland helicopter deal is worth 3600 cr.]

Voice of Mr.Anoop Kumar Gupta doesn’t looks so confident.

But the alleged amount received by Khaitan is insignificant ( $ 2,75,000) and the news paper goes on " The ED document accessed by this newspaper says, “funds to the tune of Rs 110 crores have been received by M/S RAKGT from various companies.”".

Looks the amounts are not so big considering the KRBL size but the damage is already done.

This case will end up like another Bofors, never ending…a political weapon for next few general elections

Disc: invested at 450, waiting to settle down the dust to acccumulate

Pabrai investement issue was raised and extensively discussed in this forum. Mr Pabrai has given many interviews since then but he never divulged the reason publicly. In fact this issue was raised in the concall, but management , eventhough they are privy to the info, they merely said they are not aware of Pabrai invedstment in their company as per their records. Now when the skeletons are spilling out of the cub board , Jt MD in his media interview , admits that ED has stalled the transaction and Pabrai gave back the shares to the original owneer. This only proves we shd be extra careful instead of blindly following celebrity investors. Recent Anoop Kumar inverview has raised more doubts rather than clearing the issue.

Disc; Exited the investment with minor loss. May reenter once KRBLmanagement is absolved of the alleged money laundering issue.

I think there’s one major lesson for investors in general and amateur investors in particular- It could be disastrous to clone investment strategies of star investors

And, often, our instincts may discourage us from investing in a particular stock. It may serve us well to commit the error of omission than the error of commission.

IMO, KRBL has a real product and I won’t put it in the same category as PC Jewellers and Vagrangee whose numbers may turn out to be outright fraud.

It would have been more ideal had the management disclosed its questioning by ED prior to the news report. But otherwise my take is that Mr Gupta seems to be an honest businessman and at that stage (2013) in his career and business, would have hardly had any motivation to receive proceeds of crime.

If one is a long term investor (who will remain invested in the business for 5-6 years), then such news reports with remote possibility of any monetary outflow from the company are not worth much and such moments are quickly forgotten by the market.

All this while people were hoping for a correction in prices, let me tell you this that in my experience, a correction never comes without a reason. It is the ability to distinguish worthy reasons from the rest which makes a great investor.

Worth remembering how WB bought Amex when everyone thought it was on the verge of default.

Disc: Invested at avg price of 430. Still holding.

A good theory and investment analogy but wrongly applied. First of all nobody knows what is the extent of management’s involvement in murky dealings. We are not even talking about biz loss like in case of Amex but loss of trust in the management which could be permanent. No investor will be standing to count and discount the earning whatever it might be. Long back someone cautioned me about agri businesses being popular conduits of money laundering due to tax free nature of earnings. This might not apply here but all nice looking return ratios will go up in smoke if there is any wrong doing.

Not a single question on the most important aspect of the issue - RAKGT. Was it a KRBL subsidiary? Did it receive any money? Was it’s ownership transferred out of KRBL to Potdar? And why?

I do agree. Few years back was the case of Jindal Steel & Power . Where CBI had filled the chargesheet and stock was trading about 300 and come down to 90. But today every thing is history , now again Jindal Steel & Power is rising. It will take near next 2-3 yrs to attain same level. Now its simple mathematics game how much u can loss or save.

Disc : Invested & confused whether to hold or Sell (Buying Price 449)

How can you compare the two companies… While Jindal was involved directly in the issue while krbl as a company has nothing to do with this issue… Please refrain from speculation of price movement

Thanks Sumitg, I accept my mistake and deleted the speculated price.Secondly, I’m not comparing two companies , Im comparing two Panic situations, Where investor has lost the money by some bad managements. You or I cannot deny that KRBL has hidden many things which they could have disc earlier or even today(now).