Frankly, I’m skeptical that increased oil prices would benefit KRBL. Just like reduced oil prices didn’t have any substantial change in the lives of common Indians I can’t imagine why elevated oil prices would change the consumption patterns of the populace of oil producing nations. The government probably benefits but common persons, I doubt it.

Agree with the previous comment. I don’t think high oil prices will make the Arabs eat more basmati. Also, I am not sure if the management would be looking to sell power assets. All they have said is they would not invest more. I was surprised at the buyback talk in the concall as there is very little cash on the balance sheet, with a thousand crore working capital debt.

On the positive side, rupee depreciation would help the company.

Agree that its staple food and the consumption amount may not vary much in economically bad and good years.

When it comes to consumption, an economically good year gives more assurance than and economically bad year. Also, India gate classic is most expensive and aspirational brand. When people have more money in pockets, they would tend to celebrate more and also their purchasing power of expensive things becomes more.

When oil price increases, Govt gets more money to spend on infra etc which would put more money in the pockets of people (indirectly). The gulf countries are well known for their generous bonuses when they are earning well.

The selling of power asset theory is my guestimate. It might or might not happen. I am guessing, it can happen. Management is finding the further power investments unattractive. So, I am thinking, they could get rid of the already present assets too, as it would help them have sufficient cash on books to buy rice NPA assets (they have disclosed this intention).

I checked with KRBL investor relations and have received the below reply after about 13 days (received the below reply on 25th May):

"Dear Sir,

This is with reference to your trail mail regarding shareholding details. In this connection we would like to bring to your kind notice that company get the beneficiary position from respective depositories through its Registrar and Share Transfer Agent (RT) Alankit Assignments Limited. Accordingly, the name of Pabrai Fund is not reflecting on beneficiary position received by us from depositories. However, name of Indian Clearing Corporation Limited with holding of 6494891 Equity Shares is reflecting on the beneficiary position. Company’s concern is limited upto the beneficiary position received from the depositories and not security market operations/media reports as mentioned in your mail.

Kind Regards,

"

- Does not clarify much to me, do you understand something new? Surprising thing is all media outlets reported this on 12th Feb, BSE bulk deal report for 12th Feb supports this (it lists Pabrai funds as the buyer of these 64 lac shares), so how can these shares still reflect under clearing corporation 6 weeks after the transaction (i.e in KRBL’s 31st March share holder report)?

4 Likes

This might help:

(Source: https://www.ccilindia.com/Membership/ByLawsDocs/CCIL%20Rules-%20270715.pdf)

So, looks like there could be some kind of regulatory or technical difficulty in transferring the shares to Pabrai Funds. We have no way of knowing the truth unless Pabrai himself answers this or someone from CCIL officially confirms what is happening here.

Does the company earnings profile change once big /known investors buy shares of the company? Finally long term return of retail investors depend on company earning growth and ROCE. We should identify companies and invest before known investors invest in it. They should follow us instead we follow them…this is the best rule for highest return but not easy to implement!

Second point- big investors has accumulated wealth and they have capabilities to lose and remain invested even price correct 50% but small retailers lose capital by exiting on correction aa they don’t have financial capabilities and patience

2 Likes

Conviction on limited funds is always the most difficult thing. Markets reward conviction and realization…There is always a gap which is where fear rules. Following success is the easiest path

What are the factors that Pabrai would have seen to commit almost 400 cr to KRBL. Would be interesting to think along these lines.

Here are a few things that could have been considered by Mohnish Pabrai.

- Front runner in the basmati rice industry and good localized market dominance (1 or 2 in most of the markets).

- Brand -> Can make it FMCG-like product.

- Operational efficiency in a capital intensive and challenging industry.

- Fully integrated rice company -> Better control over the product.

- Size of the organization (Market Value ~ 10K Cr) -> Allows MP to allocate good portion of his capital.

- Moderate to high barriers to entry.

- Growth prospects in other product segments. Strong distribution network and supply chain management should favor the company in these new areas.

- Able management.

Company does have a few risks like any other company in capital intensive industry. Also, being an agro company KRBL can face uncertainties and challenges related to weather and state policies.

To me, KRBL does not have a mutlibagger written all over it. But with very little downside and reasonable growth rate along with an FMCG element, KRBL does not have a reason not to sit in MP’s portfolio.

P.S. MP does look for multibaggers but more than that he looks for value. Now, we will have to just wait to know if that value makes it a 2X or 5X in next 3-5 years.

3 Likes

These factors were present since long and nothing change after Pabrai entry…only thing change is PE upward re-rating!. If we could find such factors in other companies where growth is high and no MF/known investor entered till date, I think that will be better investment (invest where PE upward re-rating is due instead where it already happened)

3 Likes

High growth + Under valued + Under followed is certainly a killer combination but only if one can identify such a company and hold it with conviction for a good amount of time.

No PE re-rating after MP’s entry. If anything, KRBL’s current market value is lower than what it was.

As you said many of the factors have existed in the past. But some of them gained momentum only recently:

- Gradual shift towards branded (90%+ branded) improved operating margins. In the last 5 years, though the revenue growth has been modest profit growth has remained healthy. Now we can argue that buying low and selling high of paddy and rice respectively might have contributed to profitability. But only the buying-selling game cannot promise the kind of margins the company has achieved in the recent years. So good chunk of the profit growth can be attributed to the “branded sales”. This shift has become evident only in the recent years 16-17 and 17-18. Market loves numbers that are consistent with the narration, hence the RE-RATING.

- KRBL entered healthy-food segment in 2016 (if I am not wrong) and has been trying to scale since then. So there is some visibility on the new source of revenues which did not exist before. Also these other segments are specialty segments which do not squeeze margins. Since the management is planning not to invest in power business anymore capital will be diverted to the new opportunities that the company has been betting on.

- KRBL is generating decent FCF in the recent years and I don’t see any reason for it to not to continue doing it in the near future. If KRBL can generate significant free cash flows (something like ~150 cr in year 1 and growing 10-15% annually) consistently for the next decade, which looks likely, there is a good chance of it being undervalued currently.

Note: Good FMCG companies grow steadily at modest rates but generate good free cash flows and usually have excellent ROIC. They trade at very high PEs contradicting their own growth rates. ROIC, FCF and consistency over the years make them favorites. I think KRBL would want to follow a similar path given where it stands today. How successful it is going to become? I don’t know.

Anil Kumar Goel’s entry has brought KRBL into lime light. KRBL didn’t look great (at least the numbers) when Mr Goel bought a stake in the company. 1000+ debt, cap intensive business, commodity etc etc had made it look unattractive at the best and terrible at the worst. But if one were cognizant of the facts that working capital is funded by debt and the company can scale its operations with little effort, stock would have looked interesting. My point is if one can understand fundamentals of a company and estimate future cash flows and growth with some certainty then it doesn’t matter who brings the stock into “public” domain; it will still make you money.

P.S. Too long a post. Sorry, I couldn’t do it shorter and I wanted to share my thoughts.

Best Regards,

VB

13 Likes

I was comparing LT Foods with KRBL. The EBITDA margin is significantly different…Wondering why…both of them have the same nature of business. Economies of scale can be one factor, but the difference is more than 500 bps…and hence there could be more reasons. Any thoughts on this will be really appreciated.

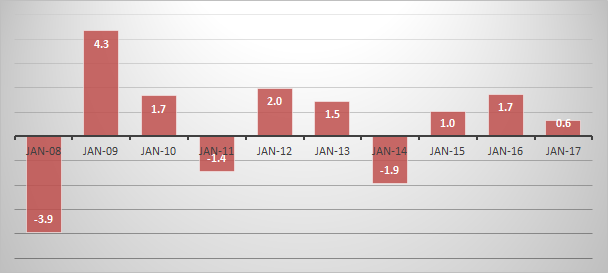

Thanks for the write-up. The chart below shows Cash Flow from Operations (CFO) as % of Net Profit (PAT). Would you be able to suggest why it is deteriorating in recent years. Thanks.

CFO/PAT

Pradip,

For KRBL, primary reason for the big swings in CFO is the way inventory is managed. Whenever the company adds significant amounts of inventories cash is converted to inventory (for future sale), thereby reducing the cash. So we expect to see CFOs lower than the profits for the years for which the company adds good amounts of inventories (compared to previous year).

As we can see from your picture the pattern is cyclical. For some years CFO is lower than the profit and for others it is higher. Over time the company does recover its cash. However, one should be worried if CFO/PAT <0.8 for consecutive 2-3 years ( which means company would not be able to convert the sales into cash).

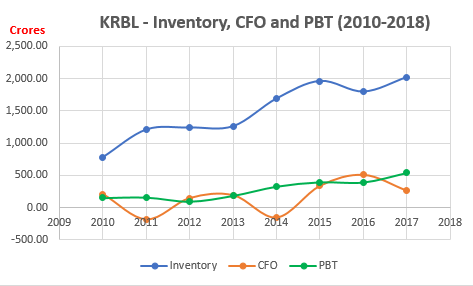

We can expect this cyclical pattern to continue in the future but given the good margins in the recent times the company would want to stabilize the CFO and avoid wild swings. The figure below shows CFO, Inventory and PBT for 2010-2018.

-VB

11 Likes

Got to see how the fate of non basmati rice exports to China will turn out to be. If it succeeds, it may help Basmati exports too (my personal non expert opinion). The chances are more that China unofficially restricts Rice imports like they are restricting Basmati imports (another non expert personal opinion).

A quote from the article:

“Chinese prefer Basmati rice. They also like Thai rice which is competing with Basmati,” the Chinese source said.

Discl: invested recently @450 levels

2 Likes

Some Points from the news:

- non-basmati rice export to Bangladesh and basmati rice shipment to the European Union is set to decline.

- A part of this decline, however, is likely to offset with the beginning of direct import from China, possibly in the second half of the current financial year.

- A study from India Rating (Ind-Ra) believes India’s export price is likely to remain competitive in the international market and the recent decline in India’s rice export prices could attract buying from African countries, as Indian rice has become more competitive while a decline in rupee is cushioning exporters’ margins.

- India’s exports could reduce by 0.5 million tonnes to 1 million tonnes.

Discl: invested recently @450 levels

http://www.careratings.com/upload/CompanyFiles/PR/Kohinoor%20Foods%20Limited-04-16-2018.pdf

So, Kohinoor downgraded to D. Expect more fire works from competition (the poor one’s like lakshmi energy and food etc) based on the kind of balance sheet they have been maintaining  . Also, if one attends concalls of chamanlal and KRBL, signs were visible. Hope, this will help industry to consolidate and string balance sheet players to emerge stronger

. Also, if one attends concalls of chamanlal and KRBL, signs were visible. Hope, this will help industry to consolidate and string balance sheet players to emerge stronger

4 Likes

I don’t know what to make out of this story? None of the names mentioned in the story are part of the promoters now… https://www.sundayguardianlive.com/news/ed-revives-agusta-westland-case-fresh-leads

8 Likes