You have to take the capacity of 4.2 MTPA which I think comes on stream in fy 19. Management has indicated that current debt may be peak debt, or very close to it. So we might assume EV to be close to 1900-2000 crores and do our calculations accordingly and try to figure out the valuations 1-2 years down the line.

Having said that, markets run more on sentiments and emotions of market participants rather than these kind of calculations.

This is my first comment on VP and I am glad that my first comment is about KCP. Here are some of my observations and few of these may answer some questions posed by others in this thread.

KCP may not have the brand value as Ultratech or ACC. But its popular in AP especially in the new capital region for decades.

Many people are worried about govt contracts if there is change in state govt in 2019. But the retail prices are much higher compared to the govt prices as govt negotiates for bulk deals at lower prices.

Capital construction does not mean just govt buildings. Amaravati is a green field capital coming up over 35,000 acres of pooled land from farmers. Of this, govt giving back 1/4th of land to farmers. Most people will build new houses, apartments in their lands over next few years. Govt also giving part of land to many private companies, educational institutions, hospitals, hotels, schools. All these will be retail customers which KCP can serve.

As the plant location is closer to Amaravati, there will be less transport costs for KCP.

Real estate in and around Amaravati will be the major driver for growth in the region. There are already hundreds of small apartments being built in the region. Also, large housing construction companies started their projects already in Mangalagiri region which is closer to Amaravati.

Disc: Not invested. I started investing just 3 months back and came across VP just few days back. I did not even know that KCP is a listed company even though I know about this company for more than 20 years. Strongly considering it now.

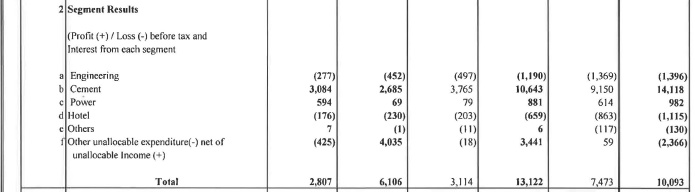

Results are good if one time revenue from subidiary is removed -

this q last q

Egineering 2,486 2,539

Cement 23,473 21,909

Power 2,504 1,883

Hotel 431 344

Others 131 3,927

Losses have narrowed down in engineering and hotel as management commented earlier.People initially might look only PnL and be worried but to me it looks healthy as expected.

Any idea why the pat for their core segment cement is less yoy ? even though the revenue are higher? Is there pricing pressure which impacted the margins in the cement sector ?

Difficult to say about pricing - I gather that pricing has picked up and is firm - but power and fuel expense if you look - that has shoot up from 45 cr to 75 cr. I believe that is mostly due to firm coal prices - that mgmt has already commented in previous quarter that this could put pressure on margin.

Thats great news for KCP. We need to be patient and watch for consolidated results. Also consider that the Vietnam sugar plant has gone through and expansion of sugar capacity and power capacity. May do an EPS of 12 for the year is my guess.

dispatches of sagar cements are very healthy for month of feb - this is one indication of demand in the AP/Telangana region.Eagerly waiting for KCP cement details…Below are the details as posted by @basumallick on sagar cement thread -

Could someone tell how is coal prices and freight faring now compared to last quarter.

This states that most fertilizers plant and cement plants in general are importing coal because of the quality and the price of coal is lower and is expected to fall due to china shutdown.

According to data available with CEA, renewable energy generation increased by nearly 49 per cent during April-December 2017 against the same period in the previous year.

even though I know about this company for more than 20 years. Strongly considering it now.

even though I know about this company for more than 20 years. Strongly considering it now.