CMP- 120 rs

Market Cap - 1500 crs

Debt - 500 crs

KCP is a conglomerate which has 4 business divisions:

-

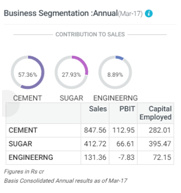

Cement - KCP operates 2 plants in Andhra Pradesh with a capacity of 2.6 MT. It has announced a brownfield expansion of 1.7 MT which will take the total capacity to 4.3 MT. Cost of the project is around 500cr and is expected to be completed by Q3 next year. KCP has captive limestone reserves and 30MW power. Cement produced this year was 1.7 MT and capacity utilization was 67%. Current EBITDA per ton is 700 and has declined a bit from last year due to pricing pressure, however there was volume growth of 15%. Cement constitutes 60% of the topline.

-

Sugar in Vietnam - Company has expanded capacity from 7000 TCD to 9000 TCD in March this year. It is expanding this to 11000 TCD by next year. It has also commissioned a 30MW co-gen plant in March. Sugar division last year reported lower profitability as it got impacted by unseasonal rains. Thus cane availability and recovery rates were lower. The expansion from 7000 to 9000 TCD was done in March and thus last years revenues did not capture increase in capacity. Further expansion to 11000 TCD would only contribute to revenues in FY19. Sugar is currently 30% of the total revenue.

3)Engineering - KCP has 2 engineering units in Chennai. This division has a turnover of 80crs and has a loss of 16crs. This division has been making losses for a few years but used to report operating profit of 50+ crs few years back.

4)Hotel - KCP built a 4 star hotel in Hyderabad for 100crs. It has given the management to Mercure hotels. Hotel reported a loss of 10crs.

KCP also has a JV with fives which makes turnkey sugar plants. This JV makes a small profit.

Outlook:

KCP’s cement division has reported healthy volume growth in Q1 and is expected to do well due to building of Andhra’s new capital, road and irrigation projects. Realizations should improve with increase in capacity utilization.

Sugar division should report good revenue growth for the next 2 years on the back of expansions.

Management has guided that engineering division should break even this year on the back of orders from defense and railways.

Hotel division should report operating profits with increased occupancy levels.

Risks:

- Further diversification into container freight station.

- Delay in infrastructure spending

3)Sugar division numbers are reported only once a year thus it is difficult to track.

4)Engineering and hotel could be a drag on KCP’s overall profit

5)Rise in input costs

At 70$/ ton KCP’s cement division itself could be worth 1900crs even though replacement cost would be 100$/ton.

Disclosure: invested

- In my humble opinion it is still undervalued at 120 - the mcap and sales are almost same even when Nifty has touched 10000.Very conservative management (read last 5 year annual reports - better cash management).Huge land bank in chennai - valued around a little less than the market cap.Small portion used for the hotel - rest might be used in future for container freight in future(though have not mentioned this in this year’s AR).Debt to Equity is healthy when most expansion is underway - so chances of less downside.Best part is cement business isnt valued the way other cement companies are - its not even half of where other companies are quoting - so sooner or later they will have to either de-merge it for value unlocking or shareholders will have to be rewarded by other means.Vietnam plant is icing on the cake.

- In my humble opinion it is still undervalued at 120 - the mcap and sales are almost same even when Nifty has touched 10000.Very conservative management (read last 5 year annual reports - better cash management).Huge land bank in chennai - valued around a little less than the market cap.Small portion used for the hotel - rest might be used in future for container freight in future(though have not mentioned this in this year’s AR).Debt to Equity is healthy when most expansion is underway - so chances of less downside.Best part is cement business isnt valued the way other cement companies are - its not even half of where other companies are quoting - so sooner or later they will have to either de-merge it for value unlocking or shareholders will have to be rewarded by other means.Vietnam plant is icing on the cake.