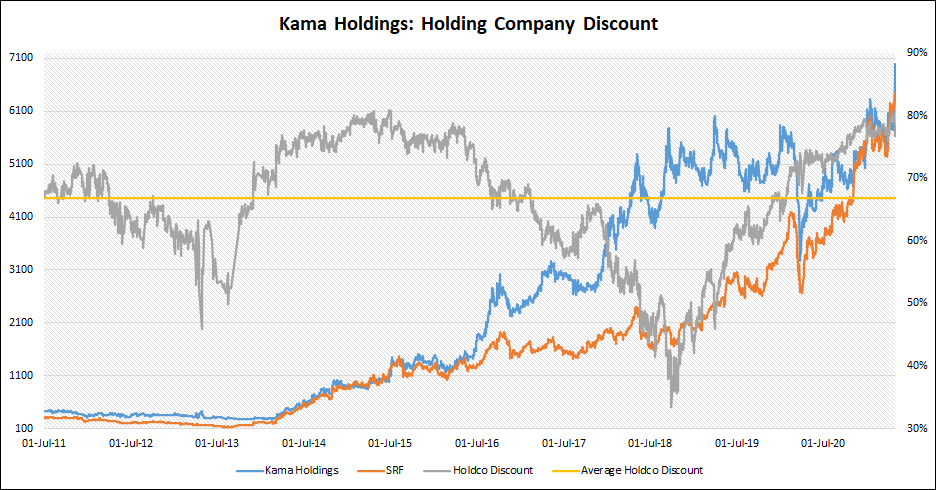

Kama Holdings is the holding company for SRF Limited. Market capitalization for Kama Holdings is '840 crore. Kama owns 52% of the share count of SRF, or 30 million shares. At current valuations, this holding amounts to '3,900 crore, indicating a discount of 80% to the value of just SRF held.

SRF paid a dividend of '10 per share in FY15, implying a net inflow of '30 crore for Kama Holdings as dividends for the year. Kama’s investment on books into SRF stands at '404 crore. Kama increased its holding in SRF by 1 million shares from 29 million as of end-FY13. This is a positive indicator of financial health through an open market buyback. It is instructive to note that this was done at an average price of approximately '162/share, a very good acquisitive price. Today, SRF is worth '7,400 crore or '1,275 per share.

As my friend and passionate value investor, Krishnaraj V (fondly known as Kimi) puts it: “A company should be known by the companies it keeps”. So, is SRF a good underlying investment? Let’s delve briefly into SRF.

SRF enjoys a global leadership position in its technical textiles business. It is a domestic leader in various other business lines such as refrigerants, engineering plastics, industrial yarns, polyester films and fluorospecialities, In FY15, SRF earned its revenues at an operating margin exceeding 25% on its consolidated business, after two years of sub-optimal margin performance. Note that this was despite strikes and inventory write-downs. Returns on average Net Worth stood at 13%, while pre-tax ROCE stood at 11%. Working capital requirements remain high for SRF thereby depressing capital returns during its growth phase. Debt to Equity (D/E) ratio stands at 1.0x. The promoters are known to be able and honest in their dealings, and have interests aligned with that of the company (through a cumulative 75% stake in the firm, inclusive of that held by Kama). While we should not expect more rapid growth in revenues, better operating margins through lower input costs, should enable profitability to increase faster than topline.

Per SRF’s FY14-15 Annual Report, Amansa Capital, a fund run by noted value investor Akash Prakash, started buying into SRF in May-2014 and now owns 5% (or 2.9 million shares) as of June-2015. Akash Prakash has the uncanny ability to buy undervalued businesses which blossom over a 3-5 year horizon, producing extraordinary long term gains. Examples include Eicher Motors, Ashok Leyland, Whirlpool, among others. The list of investors is long and noteworthy. A glance through the Annual Report or Company Shareholding Pattern would disclose further details.

There seem to be two possibilities:

- Kama’s holding discount narrows over time, compounding Kama’s returns faster than that of SRF’s.

OR - Kama Holdings mirrors the returns of SRF, implying the discount stays at a deep 80% to holding value.

In any case, the probability of the discount deepening further seems less likely than its narrowing, creating a substantial margin of safety.

A case of ‘Heads I win, Tails I don’t lose much’.

Disclosure: I do not own shares in SRF Limited or Kama Holdings Limited