Thank you for sharing takeaways but you might want to recheck the link sir.

1 Like

Im sorry…does the link not work? strange…

Ill try to attach the same once again: Q4FY19 conference call takeaways

Let me know if this works or not.

Hello Sudhir ji,

i have visited your site and retrieved the link

Thank you

Thanks @acido255 … for further reference and information of forum members, attached herewith are 2 general reports i managed to lay my hands on… trust this helps…

Stocksview Report on Jiya.pdf (411.9 KB)

Thomson Reuters report on Jiya.pdf (440.4 KB)

2 Likes

will we also get the bonus shares?

@acido255 … no, in my opinion… as the bonus shares is issued in the 100% subsidiary, in which only the parent company ie. Jiya Eco Products holds stake. So only JEPL is entitled to the bonus shares.

this is interesting

how this will impact us? will be any benefit us

Hey guys, I am fairly new to the forum but have been studying this company for a while now. I’d recently sent an email to the Company Secretary, Mr. Harshil Shah, and have received the following response to my questions.

Q1. I want to understand our supply chain and distribution network a bit. In the concalls, the management has pointed out that we have commission agents who are paid on per ton basis. What I wanted to understand is if these agents just get us orders or they do some warehousing and transportation for us as well? What is our exact nature of the arrangement with these agents? How are we marketing our product right now? I understand that we have our field team which approaches potential clients, but somehow the margins that we are losing because of the commission agents (2000-3000 per ton) is substantial because we sell our pellets at 12-14 rupees per kg.

A1. The Commission agents that we are talking about are traders. Generally they are coal and other similar fuel traders. Many a times Pollution control board seals the premises or manufacturing unit of highly polluted industries. For an alternative fuel such industries will contact the fuel supplier or such traders and many people are now a days are aware of Bio Fuel. So at times we are not required to go for marketing, such industries will contact such traders directly. Secondly, it is always not feasible for company to deliver small amount of pellets to all the retail customers every month, because of the transportation cost and other similar cost. Traders in their city, will have a good amount of stock every month, so the supply chain gets easy.

Q2. In our last concall, Mr. Kakadiya indicated that we are trying to raise around 6.5-7cr debt, mainly for capex in burners and stoves. And I completely agree with the management’s effort in trying to increase the retail business, but if I understand correctly then on an average the burners cost us 2.5 lacs and raising that amount and using it completely towards buying the burners will only add 300 burners approximately. How are we planning to fund the rest of the burners to reach our goal of 1200-1500 burners?

A2. Mr. Kakadiya rightly said that the Company is trying to raise around 6.5-7 cr mainly for burners and stoves to increase the retail business. We do have a target base to install 1200-1500 such stoves and burners in tranches. Firstly by raising 6.5-7 cr we can install about 300-400 stoves and/or burners of different sizes. By fixing such 300-400 stoves and/or burners, the production as well as the profits of the Company will increase and from such profits earned a part or portion can be utilized for installing the remaining stoves and burners.

Q3. Sir, as the management has rightly pointed out, there’s a very low barrier to entry in this industry, so, I just wanted to understand where our moat lies and what competitive advantage does JEPL have over its competitors. What are we doing right now that our competitors aren’t doing yet?

A3. We are trying to set up around 1200-1500 retail client base and few industrial clients. Our Company will have competitive advantage that we have strong client base. If any competitor tries to take few of our customers, we will take back our stoves and burners given to them as per the agreement and with the readily available stove and burner, we can install the same easily anywhere to the new customers. We have an experience in this field that no one have. And we are right now active in Gujarat and yet to cover all the other states.

Q4. If we look at one of our competitor in Gujarat, Abellon specifically, it has created a very well established brand, Pellexo, I was wondering if JEPL is working on building its brand name since that will be actually useful once we scale up our retail operations and expand into other territories, and a brand name could turn out to be a hidden moat.

A4. Good Suggestion of building a strong brand name, our Company is focused to give best quality products at an affordable price. Our Company is working on that as well. Our motto is for building brand name is not only to increase the production, because hundred’s and hundred’s of inquiries are flowing every now and then,but the motto is to create awarness of bio fuel and for environmental sustainability.

Q5. Thinking about the long-run, as we plan to enter Madhya Pradesh and Rajasthan next, how much do you think that the current business model is scalable in these state? Will we have the same level of working capital requirements? How are we doing on that front to ensure that we don’t face the similar capital crunch that we are facing right now?

A5. Right now the Company is focused to cater the needs in the region where it operates. Due diligence will be done, once we plan about any other region.

Q6. If I understand our arrangement with JEIL correctly then all our burners are installed through JEIL. JEIL recently filed a DRHP, and when I went through that, it said that JEIL has installed 60 burners so far, but JEPL claims that we have installed more than 350 burners already. Am I missing out on some information? (DIDN’T RESPOND TO THIS)

Q7. If we look at Enviva & Pinnacle, our largest competitors outside India, they generally have a weighted average remaining life of their off-take contracts around 9-10 years. I understand that these foreign companies cater to industries only and they enter into long-term contracts. Do you think JEPL will be able to negotiate such long-term contracts in the near future? Because to protect ourselves from the competition, we either have to enter into very long-term contracts or build a strong brand to have a sustainable moat around our business.

A7. In India we are one of a leading bio fuel manufacturer and we are operating with the terms & conditions and contracts accepted by the Indians customers.

Q8. I know the management has come across this question several times but our debtor days is around 170 levels. I know as soon as the Gandhidham plant starts and we start receiving retail orders, it will go down and our working capital requirements will be a lot more serviceable. However, for some reason or the other, the operations at the plant have been delayed. I just wanted an update, even though the management assured the investors that the plant will commence trial production soon and commercial production will also start very quickly. And what do you think will the sustainable debtor days going ahead be?

A8. Sir, there are many external factors affecting all the Industries operating in India. Government polices, liquidity crunch and many such other factors as well. Amongst all, liquidity crunch have been one of a major thing after IL&FS issue and increase in such other banking NPA’s. Our product is substitute of Coal, where the user gets credit period of 9-12 months. In this liquidity crunch senario, it is necessary to give the credit period so as to maintain the sales as well as customer. Once the policies of the government gets stable and liquidity crisis gets liberal you will definately see the improvement in that too.

Q9. Sir, investors feel that the company hasn’t clearly explained why our last two auditors resigned and also the purpose of bonus issue. While the latter is just an accounting entry, the former is a big concern. I hope you can throw some light on the resignation of auditors and bonus issues.

A9. One of a Auditor has to resign because they were not peer reviewed and the another was pre-occupied. And the Bonus issue part, most probably all the shareholders have welcomed such move made by the Company.

My views on his response-

– The fact that the company is planning to use the entire amount towards installing burners and stoves, and they install the burners for either free or very low deposit, makes them a capital intensive business. I doubt they will be a free cash flow company even in the next 5 years.

– The company is right in the sense that their distribution and supply chain network and their long-term contracts will turn out to be economic moats, eventually. However, they are not focusing so much on building a brand name. This will make them a commodity company and gives them little to no pricing power.

– The company is treading on thin ice when it acknowledges that they don’t have a plan under process as to how they will control their Working capital needs when they expand.

– It is deeply concerning to notice that the management didn’t respond to Q6. The numbers just don’t match and there is a huge disparity. I am definitely bringing this up in the next concall.

– The management is confident that they will survive these market conditions and will be able to bring their Receivables Days down. However, the promoters have constantly reduced their shareholding to raise capital through preferential share allotment. They are planning to bring out an IPO for Jiya Eco India Ltd (JEIL) if they face difficulty raising more capital.

– The management has not conducted a concall for the Q1FY2020 earnings, yet. I guess they don’t want to turn up and disappoint the participants by informing them that they still haven’t started commercial production at the Gandhidham plant.

Disc: Invested.

5 Likes

" If I understand our arrangement with JEIL correctly then all our burners are installed through JEIL. JEIL recently filed a DRHP, and when I went through that, it said that JEIL has installed 60 burners so far, but JEPL claims that we have installed more than 350 burners already. Am I missing out on some information?"

even I asked the same question and were never got an answer from the company

next

Also, I asked them

why? some part of the business that is the distribution of burners and plant at Gandhidham was transferred to the new Company (earlier it was to be operational under JEPL why the sudden change in the plan)? and we as shareholders have nothing to gain from this while promoters will be richer from new IPO.

They basicaly Dilluted JEPL fundamentally

after that, I have dumped all the shares it was around 8-9 July . Made 1x return though.

Kindly elaborate on the effect of IPO of JEIL?

As far as I know, Gandhidham plat was earlier to be in a Subsidiary called “Jiya Eco Gandhihdam ltd.” Which now transfered to JEIL. JEIL additionally holds busnness of burners!!

Kindly clarify on the effect of IPO. And what is the current holding of JEPL in JEIL (I guess 100%)

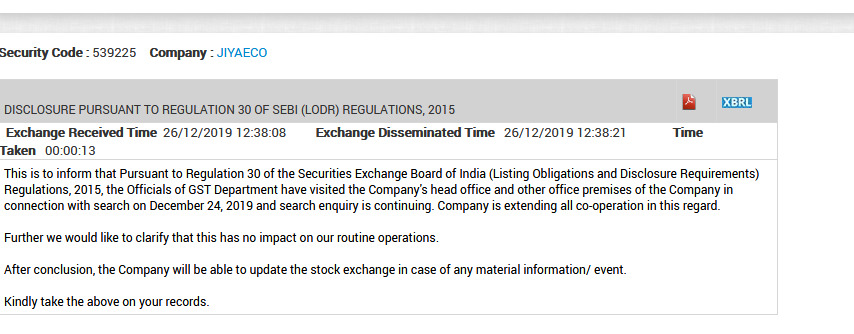

GST Dept search ops at company’s offices. Disc: Not invested.

Earlier red flags: Receivables led sales growth, delay in plant commissioning QoQ, selling by one of the earlier promoter at higher m.price

1 Like

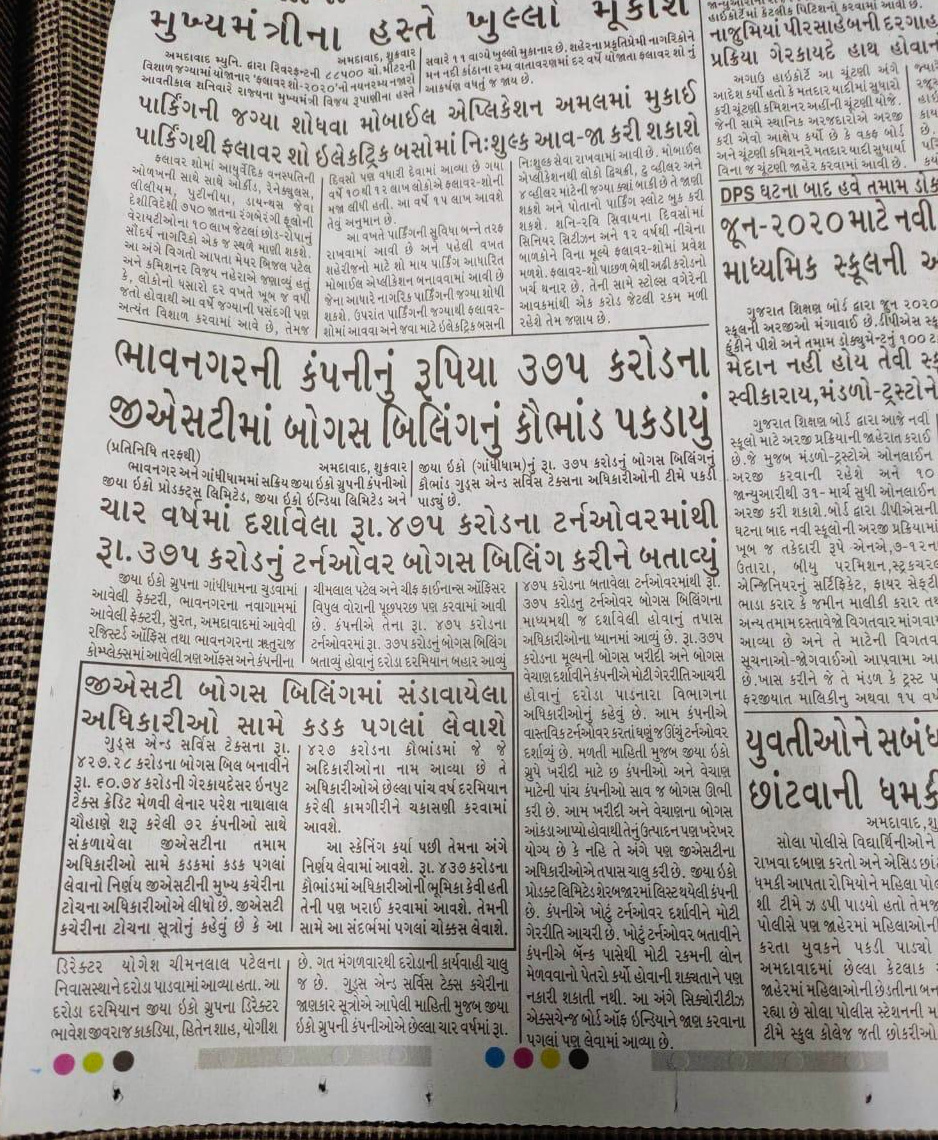

I got a copy of a news clipping, on Saturday, from a Gujarati publication. According to this article, GST officials have inspected the books of this company and reports some 375 crs of bogus invoicing that the company has done! As also there are chatters of banks staring at NPAs in this account etc etc.

While there’s no official communication, either from the company or relevant government bodies, to authenticate the claims, a couple of things that I ponder upon:

#1. The total consolidated turnover of this company, over the last 3 years, is ~Rs.340 crs! (Is the complete turnover bogus??)

#2. The company has paid taxes, to the time of ~Rs. 10 crs, over the last 2 yrs, as per published annual reports. (Tax paid is actual…on complete bogus turnover?)

#3. Total borrowing of the company is Rs.17 crs, of which term loan from banks is ~Rs. 2.60 crs, from nbfc and related parties is ~Rs.6.3 crs and working capital loans to the tune of ~Rs. 8 crs. (No such large debt exposure to worry banks)

#4. Total fixed assets of Rs. 14 crs (depreciated) and other non current assets of ~Rs. 5 crs

#5. With a combined turnover of Rs.340 crs (over the last 3 yrs), the total gst dues work out to ~Rs. 17crs (5% gst applicable as per Mgmt claims on concalls) (they haven’t paid any gst over the last 3 years?)

While I’m equally surprised (n terribly disappointed) with all this and await for further communication from relevant authorities, I thought it was prudent to update this development on the forum.

2 Likes

Company’s last intimation to the exchange:

https://www.bseindia.com/xml-data/corpfiling/AttachHis/1edd4948-9d8d-4f5d-9fa0-b6169d5d0657.pdf

I had posted the following on June 2019. God knows why the post was deleted by moderators, maybe someone flaged it

Update as on 28th June 2019 –

I have closed position in Jiya Eco Products with the full exit of holding quantity during May-June 2019. The investment that was initiated in May-June 2017 yields almost 3 times (200%) return in 2 years. The exit was due to the multiple red flags that came into my notice as follows-

- During May 2019 conference call, the management notified that they applied for the bank loan of around 7 crores for the working capital to support new capacity expansion. If they don’t get the bank loan then they would tap the capital market and bring IPO/FPO. After that, on 28th June 2019 they notified the exchange about filling draft prospectus with BSE SME platform for public issue of their subsidiary Jiya Eco India. It means the bank didn’t approve the required amount of loan which is a red flag on liquidity and cash flow situation of the company.

- The company did preferential allotment of around 50 Lacs shares during January-February 2018 that dilutes equity. Further on next year June 2019 again opting for fundraising. I don’t prefer companies that require such frequent fundraising. Interestingly, preferential allotment comes at one year lock-in period. After the lock-in removes in April 2019, since then the stock price is witnessing some unusual heavy volume and frequent bulk trades. Not only that since after April 2019, in the moneycontrol forum there are a huge amount of messages by a group of users prompting to buy the stock with some lucratively higher price target.

- One of the promoter group person Harsad Kumar Monpara continued selling his entire stake in the last 7-8 months. His entire 8.8% stake is currently almost zero. Although the management clarified that he is now not a part of the management thus selling stake, still a company which is growing at 70-80% every year such exit raises some doubt. Total promoter holding is only at 39.53% (as on March 2019) which was at 63.63% on a year ago period of March 2018 due to preferential allotment and huge dilution.

- Moreover, all the past concerns higher receivables days, negative cash flow and stretched balance sheet continues. Although management admitted all those and mentioned multiple times in the last one year that their focus would remain to improve working capital cycle still there is no visible improvement. As a result, the company is reporting 100%+ growth in profit in the past few years but still reporting negative cash flow and receivables stand at an alarmingly high level of 50%+ of the annual sales.

Due to the above mentioned red flags, I have completely closed the position in my personal portfolio. I might prove wrong and the stock price might continue its upward journey for the next few years.Kindly note that the above is not a buy/sell recommendation, rather my personal views on one of my portfolio stock.

The above was orginally published in my website. The same post is still there.

4 Likes

Hello there!

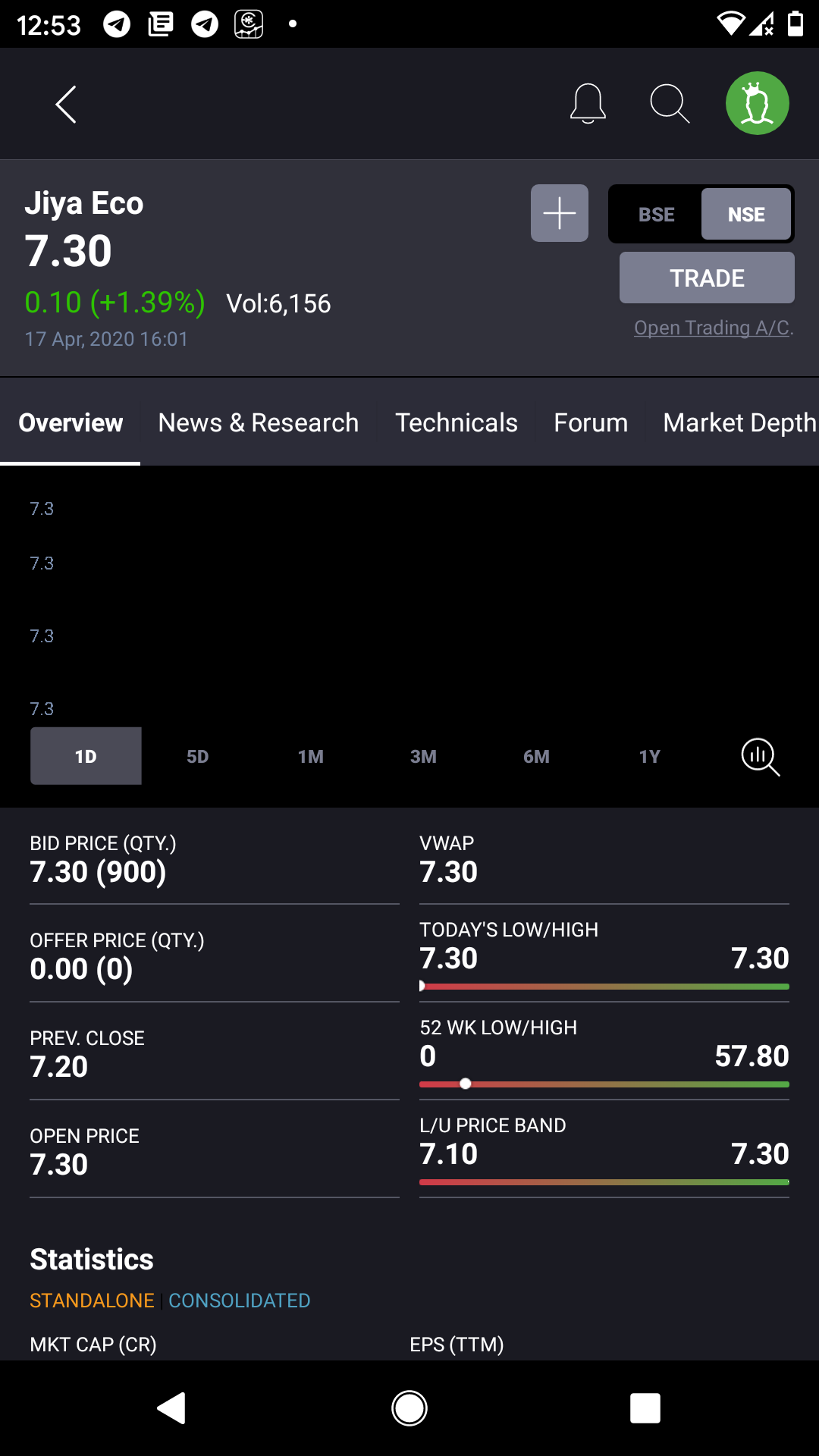

. . are you still tracking this scrip? . . . could you have an idea why has the stock price totally decimated??

tx

When share price falls to an extent that it becomes penny stock…you should only have one target going forward… How to take out maximum percentage of your principal out of that…

Some of the scrips give that chance and others don’t even give that chance…

Talwalkars was a recent example.

I would suggest avoid putting more money and thinking why it went down …

1 Like

Avoid any stock which appear too much on social media. Was watching this stock so many times on twitter. Nicely cooked up story to pump and dump.

2 Likes

Decimation of the stock is thanks to the over inflation of their numbers and the ensuing GST raids on the company, going by what was reported in the media. To make problems worse, there has been ZERO communication form the management since then. Since the day the news of the raids broke out, i’ve tried to reach out to the management, with no avail. The management is completely unreachable now!!! Now, in times like these (increasing risk aversion), why would anyone want to even attempt buying in such a stock where fingers are pointed out on the company’s corporate governance and the management has nothing to say??

2 Likes

Oh… they were active on twitter as well, is it?? i completely missed it out. Didnt miss the stupid bullish arguments put out on money control message board, which should have aroused my suspicion. But a lesson well learnt on how ‘ownership bias’ makes one ignore the hints and believe that alls well. ![]()

2 Likes