Initiating a thread on Jiya Eco-Products Ltd so that we can work together on this business for better understanding.

How I found it: Recently it filtered through screener as I was looking for businesses with Sales between 50 and 100cr and where Sales were growing at 10%+ for last 3 years.

About Jiya in few words: Company claims itself to be India’s First Company to produce Bio Fuel by agriculture and Forest Waste and any form of biodegradable waste. Bio Fuel can substitute solid fuels (Fuel or Wood) at cheaper cost and can easily be used in various kinds of thermal applications. Pellets and Briquettes (Jiya’s Bio Fuel Products) are considered to be prime renewable energy throughout the world. Company has tie-up with 52 villages in Gujarat for raw material procurement. It’s manufacturing unit is located in Bhavnagar, Gujarat and they are currently setting up 2 new plants in Gandhidham and Ankleshwar in Gujarat. Company claims that it’s Bio Fuel products are at least 30-45% cost effective compared to Diesel, LPG, and LDO.

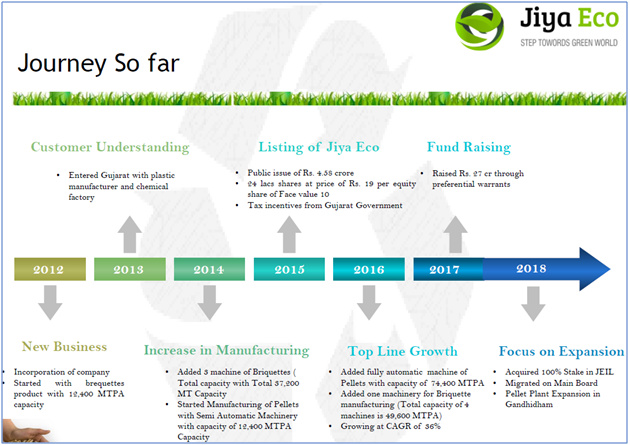

Jiya’s Journey So Far: Company has had very swift journey from being incepted in 2012, listing on BSE SME in 2015, and migrating to BSE Main Board with current market cap of ~130cr. Below is the snapshot of their journey so far.

Seems like transparent management: I have seen very few micro cap companies sharing the level of detailed information that Jiya shares with investors. Company regularly shares quarterly presentations and also provides detailed rationales of all announcements/corporate actions. Here is the link to their FY18Q4 quarter presentation shall help you to understand this business more: https://www.bseindia.com/xml-data/corpfiling/AttachHis/f842c0fa-599d-4874-9bce-166cc4835999.pdf

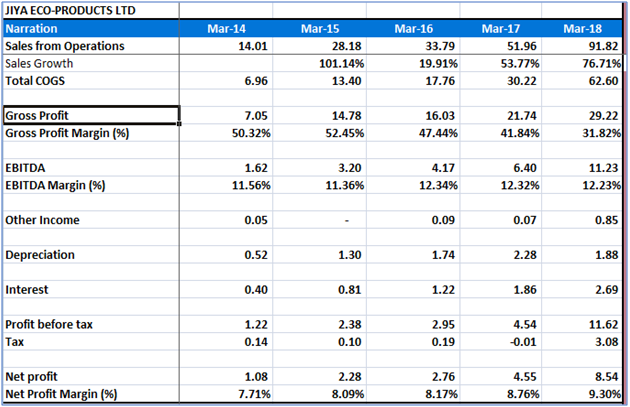

Numbers Snapshot:

Opportunity Shared by the Company:

Things I like about the company:

Company has grown topline from 28cr in FY15 to 92cr in FY18. FY17 to FY18 growth in topline has been 76.71%.

EBITDA margins and NPM have been decent and stable. ROCE is > 25% and ROE is close tp 20% for last 2 years.

Company has been expanding aggressively for its products at Bhavnagar and Gandhidham location which shall provide good economies of scale. Have rated capacity of each Briquettes & Pellets at Bhavnagar of 1.19 lakhs MTPA. And 2.6 lakhs MTPA in Gandhidham with 6 Pellet machines.

Management seems to very energetic, young, and transparent.

Seems like they have first mover’s advantage, however, I am still trying to figure out market potential for the company to address. Company is planning to enter in new geographies like Rajasthan and MP.

Shifting focus from Industrial customers to Retail SME. Going to focus on domestic/retail business of Pellets which shall lower working capital cycle and provide higher realization.

Very impressive performance by the company in last 3-4 years. Will be interesting to see if the company can continue or better current growth trajectory.

Possibility of bidding big NTPC tenders. CEA asks states to use 5-10% biomass pellets for power generation for which market size is $2.7bn.

Things I DON’T like about the company:

No patent protection and can possibly be easily copied by new entrants. Will have to keep an eye on how fast competitors are coming to snatch the opportunity pie.

Business not generating CFO or FCF. Most of the cash is being stuck in high receivables. Since business is growing most of the cash is going towards capacity expansion and working capital requirement.

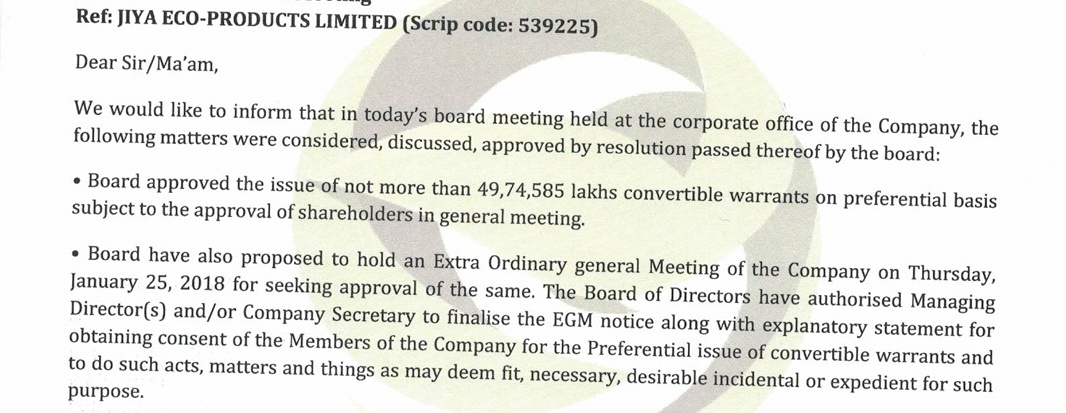

Issued 49,74,585 warrants at Rs. 54 each for total consideration of 26.86cr in Feb of 2018.

Low cost producers can be its only MOAT. Will be interesting to see if company can achieve it by scaling to a level where it gets excellent economies of scale.

Risks/Negatives:

Auditor (M/s Hitesh Agrawal & Co.) resigned on 16/04/2016 due to preoccupation in other assignments.

Auditor M/s Pary & Co resigned on 16th Oct, 2017 without giving any reason.

No patent protection and seems to be low barriers for new entrants.

Company has not proven outside of its home state Gujarat where it can face many challenges.

Possible commodity product business.

Views invited. Disc: Invested. Currently 1% position. Its part of my tail portfolio and may acquire more at lower levels, if conviction increases.

Yes, company issued 49,74,585 convertible warrants for total consideration of Rs. 26.86cr in Feb 2018 which were immediately converted to equity shares. My understanding is that these funds were utilized for Capex and WC requirements.

I am not sure if the drop in promoter shareholding from last 2 quarters has been considered in your analysis. As per the March shareholding pattern…it was around 63.6 and after the allotment it became 57%. It doesnt sound right? Is it that promoter selling in open market and then buying cheap through warrants?

Promoter has not been selling in the open market nor they have allotted warrants to themselves. Their stake has been reduced because of dilution by raising funds and issuing convertible warrants converted to equity shares to the public group. Part of warrants have been converted to equity shares on 19th April 2018. Below is the time-line of events that have happened so far in 2018:

Jan 25th – management decided to raise Rs. 26.86cr by issuing 49,74,585 convertible warrants to 70 allottees (all 70 of them part of general public group)

Feb 8th – company allotted 49,74,585 convertible warrants and received part payment of Rs. 6,71,57,041 being 25% of the total warrant subscription of Rs. 26.86cr.

April 19th – company allotted 11,59,065 equity shares upon partial conversion of the convertible warrants. Promoter holding went dow

There is possibility that promoters holding can go down to 43.46% when all convertible warrants are converted to equity shares. Below table hopefully gives complete picture.

They don’t have cash and cash equivalents enough that they can expand.

They are not taking enough debt as it can make company sink.

Left is diluting shares to finance there expansion.But,to the extent that will live them to 43.46%

Agreed. Seems like promoters desperately wanted funds to expand capacity at Gandhidham and Bhavnagar even at the cost of reducing their own stake.

Company has Accounts Receivables of Rs. 49.76cr (FY17 AR was 15.6cr). So any recoveries from here should ease cash constraints. Company has mentioned it will focus more on Retail SME market where realizations are higher than current Industrial customers and also lower receivable days.

Total Debt seems to be roughly ~17cr which comes out to D/E of 0.41

Considering these big negatives , how can you claim promoter s transparency. I am from Gujarat but I never heard about someone using bio fuels instead of LPG.

Do you know any place where we can actually go and check the product specifically - pallets

I am also from Gujarat (Ahmedabad), but live in the US. I wish I was in Ahmedabad right now to do scuttle-but work myself. However, I am reaching out to my various contacts in Gujarat and eliciting more information about Bio Fuel industry and Jiya Eco-Products. I encourage everyone interested in Jiya to do scuttle-but work and share here with everyone.

Re: two auditor’s resigning in short period of time - this is definitely BIG NEGATIVE and BIG RED FLAG. I have sent email to both the auditors asking for specifics and reasons for their resignation. Not expecting them to share any specifics (actually not even expecting their reply), but have given a shot at it.

There are not many sub 130cr market cap companies sharing the level of information and business insights that Jiya has shared so far, hence I said management “seems” to be transparent.

According to the management - Pellets are usually used in Farsan, Candy, Hotels, Bakeries and Cafeterias where mass production is involved. I am trying to elicit information from some of my contacts in catering business.

I have learnt to take all micro, small, mid, large caps with pinch of salt. One is never going to get all the clear information that is required to pull the “buy” trigger. I usually take a tracking position and try to learn more about the business. I sense something brewing with recent surprising numbers. At least 20+ institutional investors have met with Jiya management in last 1 year which shows something is brewing. I see enough decent probability catalysts and if wind blows in right direction, this biomass opportunity can ignite a lot of lights. NTPC orders and CEA asking states to use 5-10% biomass pellets for power generations can be huge for the company (viewing it as low probability of occurence) since it has early entrant advantage. Above all - what I like about the business is its “go green” initiative. All the stakeholders win in this business. And I have a strong feeling that if you have a product that would substitute your current fuel and save you 30-40% cost, customers will definitely give it a try. Jiya as an opportunity is definitely worth digging deeper.

My expectations from Jiya is very low. It’s part of my tail portfolio with less than 1% of allocation. Although I don’t wish for it go to zero, but even if it does then it will not impact my current life style.

Done some scuttlebutt about this business from small factory owner at Gandhidham. Here is my view:

Positives:

Sector is in nascent phase and there is vast opportunity for new entrants.

Some coal base power plants and big furnace operator companies use this product to improve flue gas emissions but there is no mandatory low to use it. But they are showing good interest to use this pellets so not that difficult to find new customers but margins are lower side in this area.

Kandla port is very good location for this business as waste wood is easily available and transport cost gets reduced.

Negatives:

Raw material availability is seasonal say it is very difficult to get it in monsoon months which seems a major constraint. Also output depends on raw material quality which is not fixed so pellets quality control is not fully on operator hand. Raw material cost also not fixed and no organised sector for this. High dependency in local small suppliers.

Abellon Eco is a biggest company at gandhidham which also manufacturers pellet based cookstoves,

Water heat generator & Pellet burners. Generally this product users like hotels and other players prefer to use Abellon’s pellets as it makes easy business to take pellet from equipment manufacturers and for easy warranty contact.so it will be very difficult for jiya to acquire such customers.

3.As govt has made mandatory to use FGD to control emissions in coal based thermal power plants, they may notvtake interest in this product in future.

Disc: I haven’t personally visited any plant and all the talks were on phone calls with friend which is in same business. so it should be taken with pinch of salts.

Pardon me for my lack of knowledge on SME stocks and this might be a different skill altogether which is beyond my abilities as of now but would like to highlight one key thing.

What I inferred is none of the promoters seem to have any kind of education or professional background. I understand that education and profession is not a mandatory criteria to lead successful businesses (Oyo rooms and microsoft) but then such cases are outliers. So, I am not sure how investment rationale is judged in SME cases but I consider lack of clarity on promoter education and professional background as something serious to factor in as risk and area to explore further to have better conviction. A company is a reflection of promoters and promoters are reflection of their past and if past is totally unknown, should not it be considered as a potential risk?

Few things worth highlighting from 1st level screener financials:

Super PAT growth without any positive cash from operation. High capex in initial phases is understandable but profit without cash is just an accounting entry

Receivables are not super high but still on higher side around 28-30%

Ideally with rise in sales, gross margins should improve with better bargaining power unless business is raw material cyclic and company has no bargaining power which is understandable for a SME. Here, gross margin has gone down from 52% to 42% and need to be understood in detail why so

Company is paying very minimal tax. Why?

Working capital intensity has deteriorated from 25% in 2015 to 44% in 2017 and this is very high. This could be the reason why profits are not being converted into cash.This gets reflected in increase in debt from 10 cr to 14 cr (40% increase in debt) despite of the fact that this debt has not been spent on any capex which means it is being utilized to meet working capital needs. So, can business grow it cash profit without debt in future? If company claims to be 1st in the country to have this product and the product adds value to customer why it is so working capital heavy?

Year over year company has been diluting equity and also raising debt (FY 13 to FY 17 , equity raised from 1 cr to 11 cr, debt raised from 3.5 cr to 14 cr = 20cr ). Despite of so much equity dilution and debt, there are no signs of cash profit. Why?

If we look at EBITA per rupee (debt+equity+reserves), it has come down to 13 lakhs per cr to 12 lakhs per Cr in 3 years despite of revenue going up from 14 Cr to 52 Cr which means no improvement in profitability despite of size of balance sheet increasing. Why so (why COGS has spoiled everything basically)? So, what is future plan in terms of debt and equity dilution and when 1st signs of cash profit would be visible?

Company is doing investor interactions but FY17 annual report link on website is not working? Am I checking at wrong place? where can I get FY17 Annual report?

My sense is there is nothing special or unique about the product or business apart from the name resembling feel good green energy factor. So, everything lies on hunger and ability of promoter and which I have heard drives a SME stock. If it boils down to this, then, I have question over promoter ability and history highlighted in previous post.So, again, promoter history and background becomes super important considering the above

I am not a micro-cap expert. Trying to learn and evolve my stock picking skills by swimming in new waters. In such micro cap world - I try to catch promising businesses early (small position) and then average up as management delivers/executes.

This is definitely a commodity product business. It has low entry barriers and it will have mushrooming effect on new entrants(as we can already see with so many players in the market). But my key question is - will there be mushrooming effect on acceptance of bio fuel as substitute for fossil fuel? Pellets and briquettes can substitute fossil fuels. Let’s see if we see any value migration happening to bio fuels. Players with good capacity, economies of scale and lowest cost producer(s) should be big winners. It’s not a typical compounder or buy-and-hold kind of play.

Re: lack of professionalism in management - yes, not a typical professional looking management. The key is if managers are ethical, energetic, and smart businessmen - which only time will tell. Personally, I am OK with them not fluent in english or less education or less professional background. Investors will have to keep an hawk eye on their capital allocation skills and future corporate actions.

Thank you @Akash_Padhiyar for sharing the information with everyone! Very helpful.

I was able to download Abellon’s product catalogue from this link. They seem to have good Biomass Pellet based cooking solution products for Hotels, Restaurants, Caterers, and Canteens. They also have Pellet production capacity of 1lakh tons per annum. Whereas, Jiya seems to have 3.8lakhs TPA Pellet capacity. Jiya Eco India Limited (100% owned subsidiary) also provides similar bio-fuel pellet fired burners and stoves. Would love to see Jiya’s such product catalog with product details. Jiya installs burners and stoves at user’s site and have contract with them to procure pellets for 3 years at fixed rate. This seems to be interesting model where prices are locked providing topline visibility. Downside is that things may turn bad if raw material prices spike up. Such model seems to be industry standard.

I was able to speak with a friend who is into catering business. He said he knows other catering, restaurant, and dairy users who use such bio-fuel pellet fired stoves. Awareness is lacking but slowly and gradually people are moving to these options as it saves their input cost.

can you please elaborate more on this? sorry not able to understand why would power plants not take interest in this product in future.

See though pellets are cheaper than oil, it is very costly than coal.

Thermal power plants uses the pellets for emissions control.

Govt of india has given deadline to all coal based power plants to reduce flue has emissions (to control SOx,NOx) by installing FGDs(Flue gas desulfuriser) as no other technology is available to reduce the same. Once FGD gets installed z they have no need to use costly pellets.