What is the last day for booking STCG ( short term tax gain) Losses in year 2017-18 ?

Hi Sanjay

it will take one to two weks to get aditional share in your credit .The 50% cost reduction is happen because of adjustment of share price beuase total noumber of share just became double in order to keep the same maket capitallization of the company The price is halfed e.g orginal price 100 after bonus you will get two shares of Rs 50 and to total value remain the same i.e 2x50=100 Rs. the same koind of price adjustment is done in case of splits

regards

Thank you sir. Got the additional share yesterday.

How to calculate cost of capital manually?

The actual procedure is:

- Get NIFTY50/SENSEX Data for 3-5 years and calculate daily or weekly returns in Excel.

- Get the stock’s price history for the same period and calculate daily or weekly returns in Excel.

- Use =SLOPE(Stock Returns,NIFTY/SENSEX Returns)

You can by-pass these three steps and get the Beta published online on many sites, but that’s a decision left up to you. Else, by doing the process above, you will end up with a ‘Beta’ figure.

- Find out the Risk-free Rate in India. As of this moment, it’s 7.37% (India - 10-Year Government Bond Yield 2024 | countryeconomy.com)

- Find out NIFTY or SENSEX’s returns over the same period for which Beta was calculated (If you did it yourself, this would become very easy)

- Use the formula Risk-free Rate + Beta * (NIFTY/SENSEX Return - Risk-free Rate)

You will have now calculated the Cost of Equity.

- Find out the Cost of Debt of the company. This could be mentioned in the Annual Report. Or you could make a rough guess from their Credit Rating (AAA Bonds in India are trading at close to 7.5% if I’m not wrong)

- Use the formula Cost of Equity * ((Equity+Reserves)/(Equity+Reserves+Debt)) + Cost of Debt * (Debt/(Equity+Reserves+Debt))

This would give you the CAPM-based Cost of Capital of your company.

If you are interested, you can visit my thread. The model there contains automatic formulas for calculating both CAPM Cost of Capital and Bottom-up Cost of Capital (Often quoted to be a better measure of risk than the CAPM Cost of Capital):

You will have to input: Equity, Debt, Risk-free Rate, Company Beta, Industry Beta and Industry D/E Ratio in order to successfully calculate both of them. Once that is done, under ‘Assumptions’, select ‘Company Beta’ to find out the CAPM Cost of Capital or select ‘Industry Beta’ to find out the Bottom-up Cost of Capital.

2 Likes

Wow. Thank you. Will take some time to understand. Will reply if I have doubts. Thanks a lot.

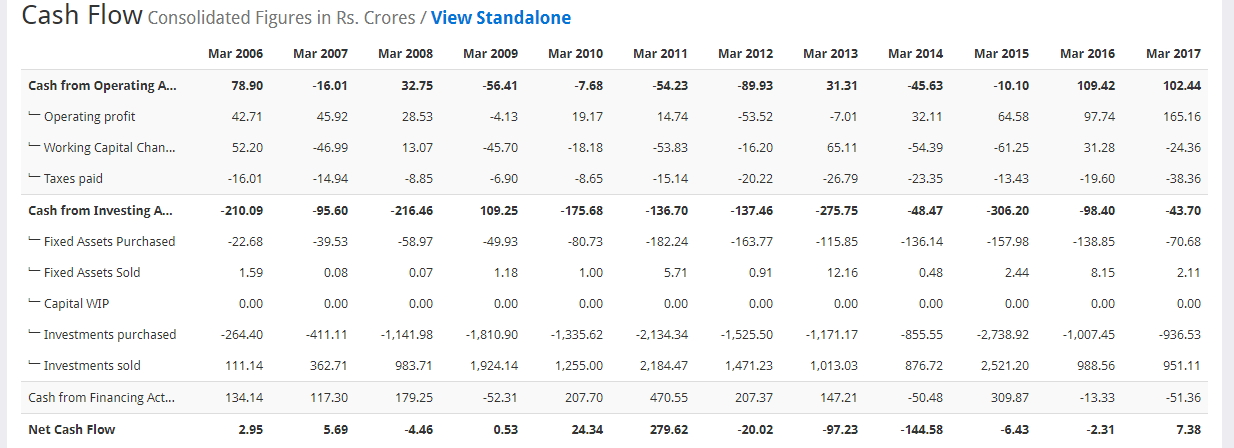

Seniors please help,

I was going through Cash flow statement of 'Trent Ltd, to see the free cash flow of at least of five years,but it was not impressive as there were number of years , where the company has posted negative cash ,Still the share the price of company is in uptrend since 2009. What I am missing here

Kindly enlighten.

Thanks

Arvind

Dear All,

I have just joined and had few of the queries. Anyone can help on that:

- Which time-tested ratios are used to find the mutibagger and value stocks in screener.in?

- If I build ratios in screener.in. Can I tested them if they really could have produce multibagger in the past.

- Is there a valuation template that can be uploaded in screener.in

- Can we have the basics of stock investing that start from basic to advance at one place…Probable by our seniors. There are pieces of advice but scattered across blogs and replies. This will surely encourage new bee like us…

- Which portfolio tool is widely used. I want to get the price and news alert on stocks. Moneycontrol charges for it after few alerts. Any advice on that?

Thanks much!

Ekta

@decoder12345

Stock investing is probabilistic guess based on various factors. Few factors which aid this are more tail winds than head winds (pvt sector financials), sector leaders creating their own niche and breaking away from the clutter (Eicher Motors, Page, Titan, Indigo) and emerging opportunities (Avanti, Symphony). Some companies without even having sound fundamentals can still generate mulitbagger returns and then fade away (Pantaloon).

So none of them can be captured using a single parameter, but a combination would do. But staying invested in a well run company for a long long time may a far better bet than looking for mulitbagger. From VP if you come to know one and latch on to it that would be great.

I would recommend you to read Basant Maheswari’s “The Thoughtful Investor” book to get a broad view about mulitbaggers.

1 Like

Thanks for the reply @sgjaclyn sgjaclyn. I got little encouragement that I received your reply for my first post. I straightway went and order the book you suggested because I am in a bit of dilemma that if leaders creating own niche and breaking away from clutter then their financial today or tomorrow will fall in place, and if we screen based on those fundamental when they fall in place presently they are already overvalued. So let’s assume we are confident of a company will create niche and break away from clutter, then is there a minimum set of screens which we can use to filter them to validate our hypothesis. For example, correct me- (Debt + Cash end of the preceding year ) /Number of equity shares < Current price, can this be the starting point?

Or the other way to bet on what are the ratio related to a well-run company? If we get that then we can filter the company that will create a niche and break away from clutter based on the future trend/prospects of the economy.

There is no doubt about that whichever way we adopt VP can be the good source to validate our findings but in both the scenario we would need the basic ration that can filter the wannabe company to maybe 10-15.

What your view on this?

Sorry asking a question not related to investing - but some technical issues on valuepickr … many times we get “cannot connect to database” error (do not remember the exact words, but something similar) and in those times it is not possible to login. I have also noticed that when this happens, it does not get fine within a few minutes, but rather can continue for even a day or 2.

Hope it is not just me and the technical team on this wonderful forum is looking into it and trying to resolve it? …

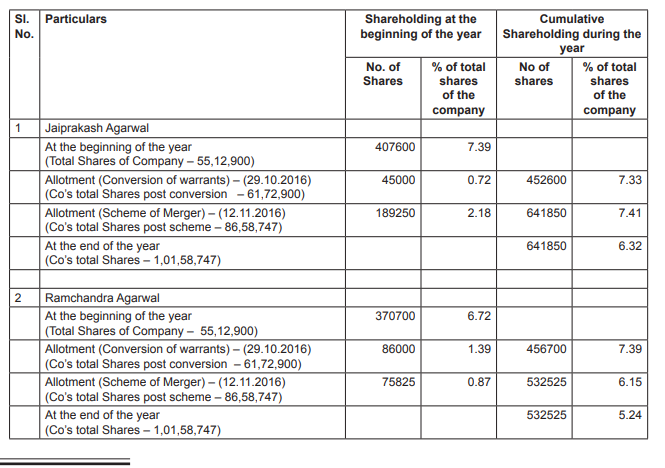

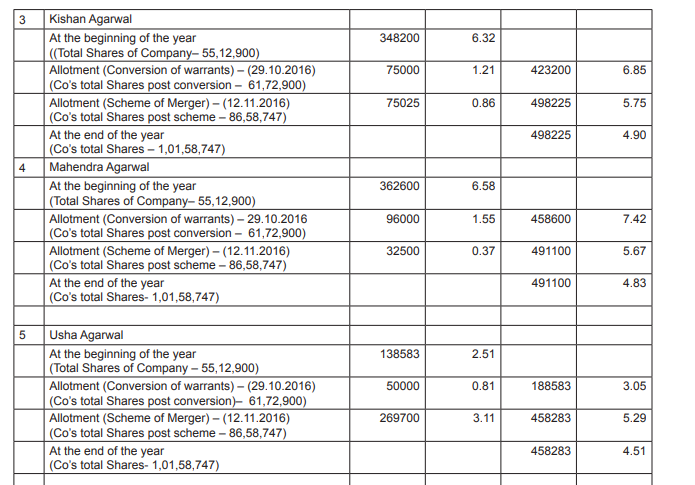

Hi All,

I have recently joined this forum and had a doubt.

I was going through the annual report of Agarwal Industrial Corporation Limited. In the annual report I came across the information that promoters had issued lot of warrants to there relativees who were legally not in the promoter group and than this warrants were converted to equity share. Further this warrants were issuedd at throawway price when compared to the price of share in the market. Does this mean that promoters are trying to jack up there holding unethical means? I have uploaded the annul report for your reference. Page No - 12,13,22,23,24

Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return - even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result.- Charles Munger

I keep reminding me of this mantra because different quotes can lead us into different direction. For e.g. if people are fixated on buy low and sell high, no one could have bought HDFC Bank as it always quotes at a premium and people would be tempted to sell it most of the time as the bank trades at a premium to all other banks.

So if management has certain attributes like growth without compromising long term future, long runway clearly identified and repeatedly highlighted irrespective of short term vagaries, not afraid to take risks and fail etc are some of business qualities I look at. And if the results are already seen, then it gives double confidence to stay invested.

So I would judge a company not purely based on specific ratios but what vision they are focussed on.

Another thing which I follow is not to run after small caps, but rather look at well run cap agnostic companies. But it depends on each individuals taste and comfort factor.

To your question about what could be the one or two ratios to be focussed on, they would be RoE (RoIC to factor the influence of debt) and growth. The first one shows the strength and the second one the stamina to run the race. There are companies like Castrol, Gulf Oil, VST Inds and several others which have high RoE, but have poor growth. These companies may preserve the capital and provide safe returns without much surprises.

BM’s book should provide you lots of clarity. The one I liked most from his book is the aspect about the behaviour of bull run its peak and subsequent crash.

1 Like

Yes thanks @sgjaclyn for giving inputs to start. I will read through the book. Would also appreciate if you can suggest some videos for basic understanding of b/s cash flow and pnl.Thanks

I made this post some time back, I hope it answers your query as well:

You could look at companies your screen returns and find out their historical performance. In fact, this is one of the criteria for a good screen that I mention above (Tweak around your screen to ensure it throws a bunch of great companies).

I would seriously advice against this, even if you do find one. Screener has very generalized data and you can’t find out the value of a company from generalized data. You can, of course, use it to calculate some basic Ratios or find growth trends etc., But that should be it.

The way I suggest Valuation should be done is take half a day, settle down with the company’s AR on one hand and tea on another. Use the internet extensively to do research whenever required. If you need a Valuation model which works like that, here is mine:

I personally use Screener to identify companies, MoneyControl to do basic Ratio Analysis, Stock Mojo to find out miscellaneous details about the company, ResearchBytes to access the concalls and of course, ValuePickr for getting perspectives on the stock.

2 Likes

https://www.youtube.com/channel/UCw4SlTWA7bpiUK-b6FssPlg/videos

I think this will help …this is free accounting course nptel… enjoy

My Mom is a housewife. She has some investments since last 2 years. The short term capital gain is less than 1lakh. She do not have any other income. Do she liable to pay any income tax ? Is income tax filing is required ? I hope today is last date for last two financial years. CA friends plz help.

Hello all my friends.if am am purchasing a stock of networth 50 cr at 250 cr market cap i.e p/book of 5. Presently netprofit is 10 cr i.e Roe of 20%.suppose after three years netprofit becomes 30cr what would be price to book after three years?can u give us method to calculate book vale for company making 30cr netprofit which was making 10 crs 3 years ago

Issuing warrants at much discount to the current share price certainly raises doubt on the motive of promoters. The simple logic being the profit admissible on conversion of these warrants to the equity shares and profit earned by selling them immediately. It will be much better to see the issue of warrants at the current market price of the share.

That is my view as a novice…ill request senior members to throw in some light.

Regards

Could anyone please help me with formula for CROIC ?

what i get from my search is : CROIC = FCF (CFO - Capex) / (Longterm debt + Shareholders equity - cash)

I the above is correct, i would want to know from where can i get the inputs for the formula ?

- Capex - Can i use Expense for Purchase of Plant, property machinery under CFI ?

- Long term debt - Can i use Long term borrowings from Balance sheet ?

- Cash - Where can i get this from ?